Listen to the audio version of this article (generated by AI).

Is a 70% crash coming?… Grantham’s track record problem… what a 1992 magazine cover got right… the FOMO that isn’t there… the earnings pushback against bears

Last week, Jeremy Grantham, British investor, billionaire, and GMO co-founder, went full bear:

This is the most expensive market in American history…

My guess is sometime between two weeks ago, two weeks from now, two months, two quarters and conceivably two years – the timing is always terribly uncertain – the market’s going to peak out and drop back to trend.

And getting back to trend from here is closer to a 70% decline than a 50% decline

Do you find this helpful?

At some point… between two weeks ago and two years from now… we’ll have a huge crash.

No disrespect to Grantham – he’s a legendary investor – but, to me, this comment is useless. Worse, it can be financially damaging.

On January 24, 2023, Grantham released his official 2023 outlook letter titled “After a Timeout, Back to the Meat Grinder!” where he warned of a potential 50% crash.

Then in April of 2023, he told the We Study Billionaires podcast that the modern “superbubble” was on the verge of popping.

And in July of 2023, he put a 70% probability on a crash matching the patterns of 1929, 2000, and 2021.

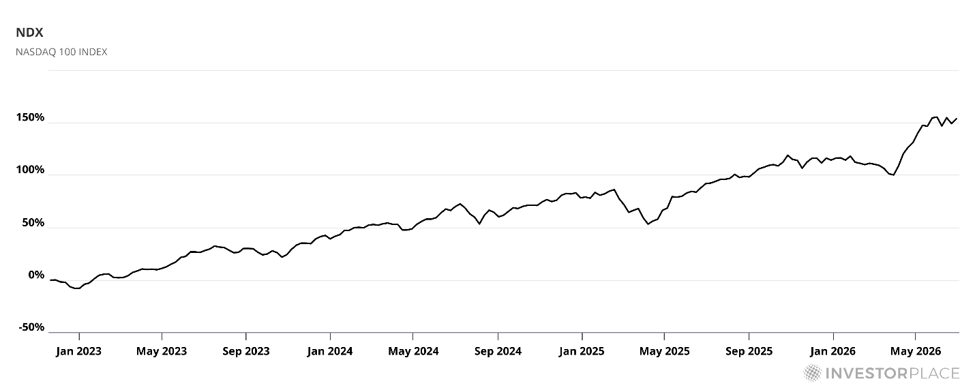

Not only has no such crash occurred since Grantham’s first January 2023 call, but stocks have surged since then. The Nasdaq 100 is up more than 150%.

If you’d sat out of stocks based on Grantham’s call, you’d have missed your account more than doubling. That’s not a rounding error – that’s a potential multi-year retirement delay.

The reality is that we will eventually have a market crash. But I don’t think it’ll be tomorrow, next month, or even this year. And today, I want to highlight one major reason why.

To be clear, I’m not saying the next 6-12 months will be smooth, or even that we won’t suffer a 10%-15% haircut somewhere along the way. But I believe “the crash” remains farther out on the horizon, which means one thing…

It’s still time to be invested and make money before the eventual pain arrives.

A magazine cover, a stock chart, and a lesson about tops

Older investors like me will recall 1991 when the U.S. economy was clawing its way out of a recession.

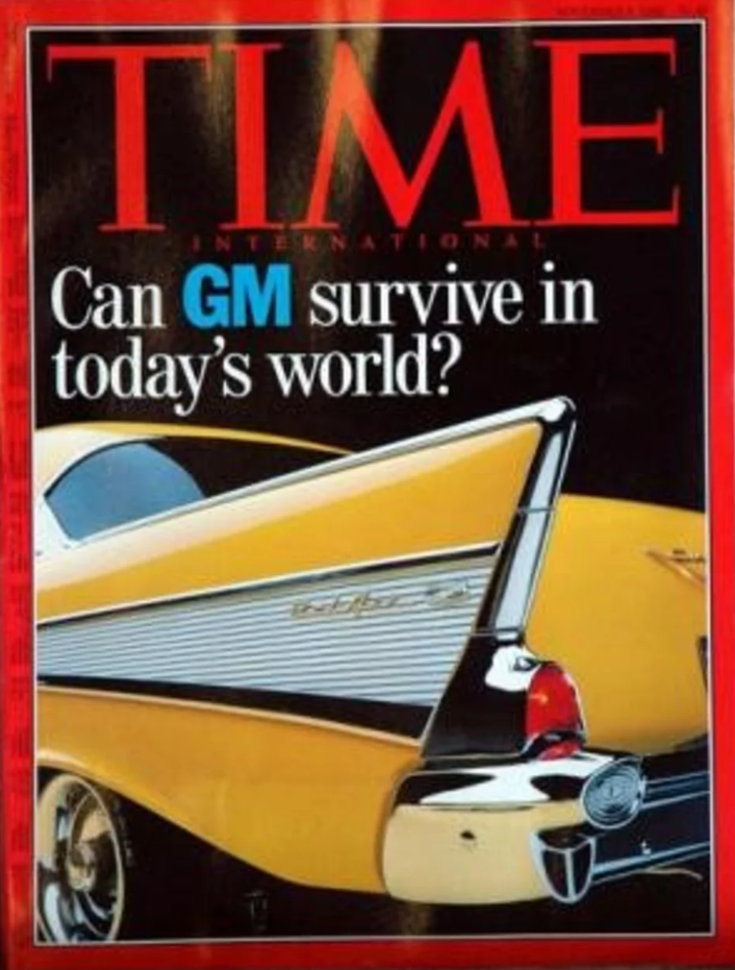

Auto sales had collapsed to a level that would mark the low point for the next 16 years. Investors were bearish on Detroit, and they had reason to be – TIME even ran a cover story that November asking a blunt question: “Can GM survive in today’s world?”

Thirteen months later, the mood had entirely flipped…

The economy was strengthening, auto sales had bounced back, and TIME ran a new cover featuring the CEOs of the Big Three automakers. But this one wasn’t despairing. It was triumphant: “The Big Three – How Detroit is shifting into high gear.”

Same company, same industry, 13 months apart.

So, which would have been the better time to buy GM stock? At the point of despair or the point of hope?

In November 1992, during the “despair” cover, GM shares traded around $28.

By December 1993, during the “hope” cover, they’d climbed to just above $55, nearly doubling.

And then, just 12 months after that triumphant cover ran, GM shares had fallen by about a third, back to $35.

Despair preceded the gains. Hope preceded the losses.

This teaches us a critical lesson about investment peaks and valleys that we’d be wise to remember today…

Whether on a stock-specific basis or across broad markets, “tops” tend to form when investors are wildly confident, bullish, and greedy, while bottoms are typically carved out when investors are despairing and hopeless.

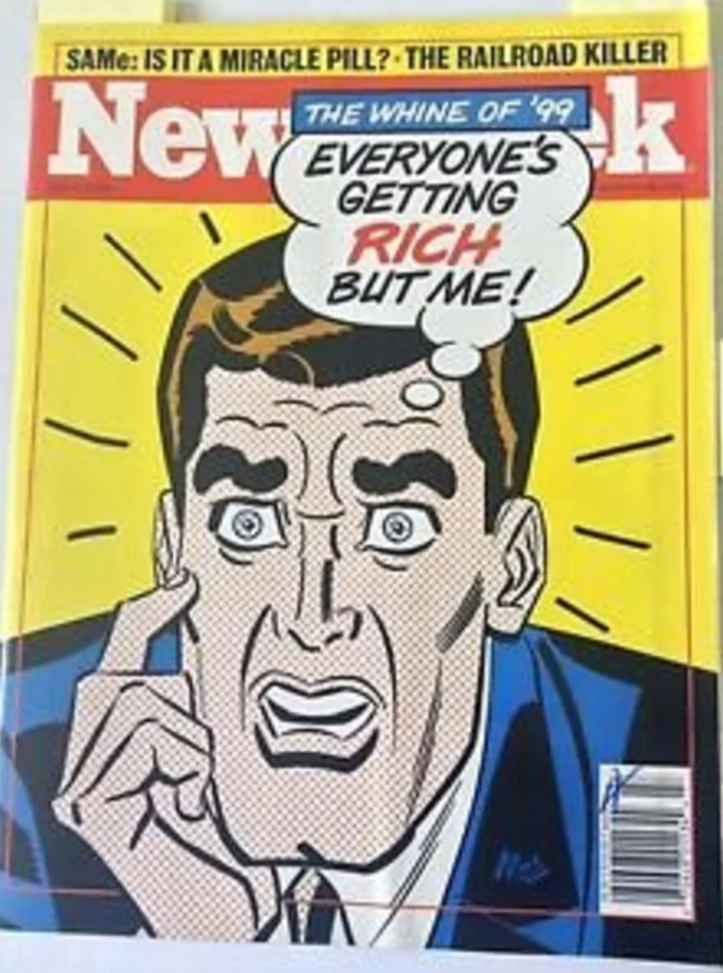

Alan Greenspan coined the phrase “irrational exuberance” to describe exactly this dynamic during the dot-com run-up. And Newsweek‘s famous 1999 cover capturing that era’s FOMO ran just months before the Nasdaq collapsed.

So, here’s the question…

Does this market feel irrationally exuberant?

The sentiment data tells a different story than the headlines

If euphoria and rabid FOMO are the preconditions for a top, today’s numbers don’t support the “we’re there” thesis nearly as cleanly as Grantham’s bubble framing suggests.

Yes, some pockets of the market are experiencing FOMO, but as we’ll get to, it’s somewhat justified by earnings. More on that shortly…

First, zeroing in on sentiment, let’s start with retail investors…

The latest American Association of Individual Investors Sentiment Survey from last week shows bullish sentiment at 44.9%. That’s above the historical average of 37.5%, so it’s not nothing. But it’s well below the 60% to 70%-plus readings that marked the actual dot-com peak.

Retail investors look more like accumulators than blind speculators right now – surveys on AI-focused investors show the overwhelming majority plan to hold or add to positions, with only a small minority looking to reduce exposure.

Now look at wealthier investors…

A recent Janus Henderson survey of affluent and high-net-worth investors found that 67% are actively worried about an AI bubble bursting within the next 12 months.

That’s not complacency or “YOLO” risk-taking. That’s a market grinding higher while two-thirds of its most sophisticated participants are looking over their shoulder.

Finally, on the institutional side, Bank of America’s Global Fund Manager Survey shows funds remain structurally long tech, but positioning has eased meaningfully. Managers are taking profits on the most extended hardware names and rotating into broader equities rather than doubling down.

Put it together, and you get a market climbing the proverbial “wall of worry” – high conviction paired with persistent, widespread caution.

That combination has historically been a feature of ongoing bull markets, not a signature of imminent tops.

A true top tends to require something close to universal agreement that prices can only go up – recall Barstool Sports founder Dave Portnoy during the 2020 day-trading craze saying, “Stocks only go up” and “only losers take profits.”

Are you seeing that sentiment today?

I see the opposite: widespread, well-documented anxiety sitting underneath continued buying.

Still, caution remains critical

The lack of rabid FOMO is not an invitation to go all-in.

Grantham’s framing deserves real respect, and there’s at least one place where the data is flashing something worth watching closely.

Here’s our hypergrowth expert Luke Lango, editor of Innovation Investor, on what he’s calling an IPO Spike Warning:

The Bloomberg data showing Q2 2026 IPO value tracking toward $400 billion — roughly double the recent quarterly average — is a pattern worth monitoring precisely because it has occurred near inflection points in prior cycles.

We are not making a market crash call. The specific circumstances of each prior spike were different, and the AI infrastructure fundamentals today are categorically stronger than the earnings realities of the Dot Com era, the leverage realities of the GFC era, or the inflation shock of 2021.

But historical patterns that have repeated across multiple distinct market cycles deserve respect, and the intellectually honest posture is to acknowledge this one while maintaining our constructive stance on AI infrastructure.

Luke recommends investors be thoughtful about position sizing, maintain dry powder for potential outsized pullbacks, and stay focused on the highest-quality, most defensible names in the AI infrastructure trade rather than speculating.

But with those defensive measures in place, he concludes:

The Summer of AI is intact. We are watching the IPO spike carefully. Both things can be true.

That posture feels right to me.

IPO mania does reflect some exaggerated FOMO, and it has shown up near inflection points before – not as a guaranteed crash signal, but as a pattern that deserves respect. However, this FOMO centers on just a handful of stocks going public.

“But Jeff, you’re missing the FOMO and greed in corners of AI like the memory trade.”

Great point! The memory/semiconductor trade is very crowded today. And I’d be surprised if we don’t see some double-digit profit-taking over the coming weeks. In fact, we’re seeing some today as I write. It could result in a longer stretch of underperformance.

But profit-taking is not the same as crashing. And there’s a big reason there will likely be loads of buyers after a bout of profit-taking…

Earnings.

Does today’s earnings backdrop support the bubble-bursting narrative?

Memory is a hot trade today – but it’s for a reason.

A week ago today, memory giant Micron (MU) told investors to expect roughly $50 billion in revenue next quarter. Analysts had penciled in $43.6 billion. That’s not a beat – that’s a different zip code.

Micron’s blowout outlook is a microcosm of a broader AI supercycle that has the entire chip sector firing on all cylinders. According to research from International Data Corporation (IDC), total global semiconductor revenues are projected to surge 52.8% to hit a historic $1.29 trillion in 2026.

Here’s more from IDC:

The memory segment is at the epicenter of this shift: DRAM revenues alone are projected to nearly triple in 2026 to $418.6 billion, driven by demand for high-bandwidth memory (HBM) and DDR from hyperscalers and AI infrastructure providers.

But this earnings strength isn’t limited to just memory chips. It’s wider…

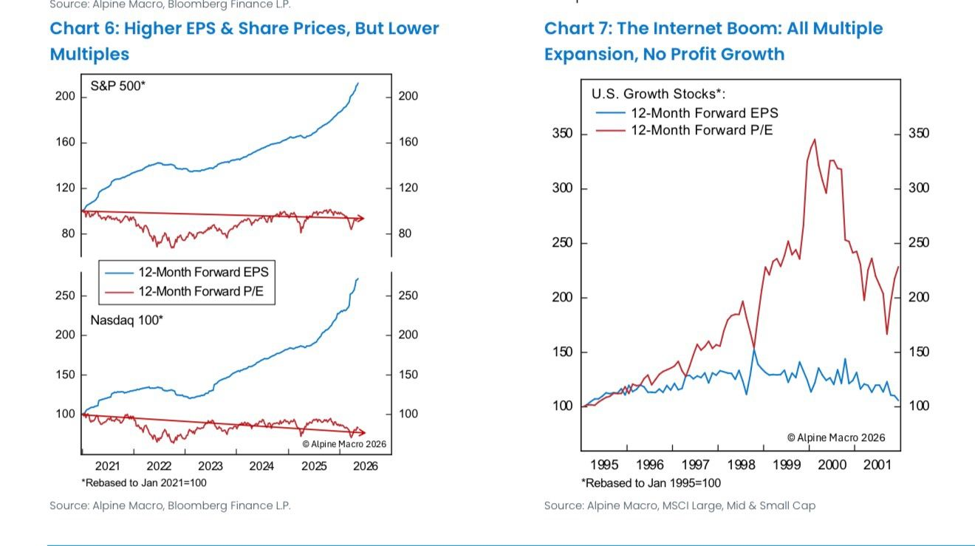

In last Thursday’s Digest, I highlighted a chart from Alpine Macro showing how today’s tech boom has something the dot-com era didn’t have…

Real earnings growth, not just multiple expansion.

From last Thursday’s Digest:

In the dot-com boom, P/E ratios went to the moon while profits barely budged. Today, earnings per share are compounding while multiples have stayed relatively flat.

That’s a structurally different – and arguably more durable – setup.

Better still, we can also look one layer up from tech to the wider S&P…

Wells Fargo expects headline S&P 500 earnings growth to surge to 22% growth year-over-year during Q2.

Meanwhile, FactSet’s forward-earnings data shows similarly robust expectations baked into current estimates – meaning today’s elevated valuations are, at least partly, being met by real, growing profits rather than pure multiple expansion.

Don’t misunderstand me – this market is not cheap. But these robust earnings take pressure off the “nosebleed valuation” argument, which – along with the lack of frothing-at-the-mouth FOMO – suggests disaster isn’t directly at our door.

Closing the loop on the memory trade and FOMO, yes, there’s some FOMO in memory today – but it’s chasing a massive number that just printed, not a fantasy number that people hope will print.

Coming full circle

If you had to put a magazine cover on today’s market, would it be the jubilant “shifting into high gear” version? Or the despondent “can it survive?” version?

For me, it’s neither. It’s something far less marketable – perhaps:

“Investors Aren’t Sure, and the Data Backs Them Up.”

Of course, magazines with that cover don’t sell well. But that’s usually a good sign for investors like you and me.

Most likely, we’re somewhere in the messy middle, though skewing toward the top. The evidence still supports parts of both the bullish and bearish cases. And that’s important because true market peaks usually leave very little room for debate.

Bottom line: Watch the IPO data… track the earnings… respect Grantham’s warnings…

But analyze whether you’re really seeing rabid FOMO today – and if you’re not, consider what that means for whether we’ve truly arrived at the peak.

We’ll keep tracking this as the data develops.

Have a good evening,