Before we dive into today’s Smart Money, first off, thanks all of you who joined me on Thursday for The Road to AGI Summit. Thousands of you all joined me, making it a huge success.

At the event, we discussed…

- How Wall Street is currently asleep at the wheel on the cusp of Artificial General Intelligence’s revolutionary advance…

- An exclusive peek into Big Tech’s secretive frontier AI labs…

- And my “futureproof” blueprint for a world of rapidly accelerating AI.

If you missed this informative event, you can click here to access the replay.

Now, on the heels of all that, let’s focus on a well-known tech company that will use AGI to create some potential new avenues for success.

This may come as a surprise, as this company has been making headlines recently… albeit the wrong kind. A recent disappointing quarterly earnings announcement triggered a massive 30% selloff.

However, I expect the unpopular shares of this tech company to outperform the wildly popular shares of Nvidia Corp. (NVDA).

So, I’m not abandoning this company just yet. Here’s why…

Betting on the Little League

The company I’m referring to is Intel Corp. (INTC).

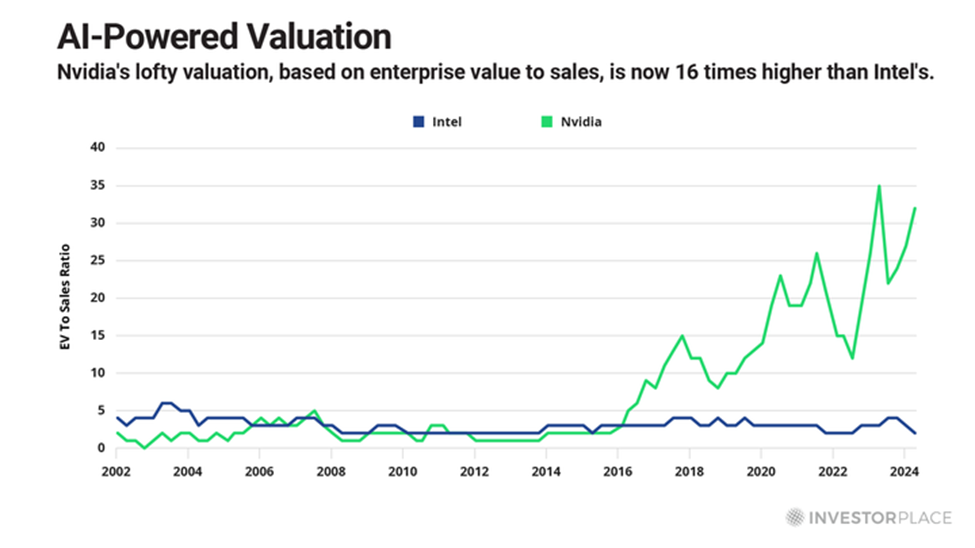

Admittedly, based on financial results from the last few years, Nvidia and Intel are not even in the same league. Nvidia is a Major League Hall of Famer, while Intel is a Little League benchwarmer. The stock market valuations of both companies amply reflect the disparities between them.

For most of the last two decades, both stocks traded for a similar valuation, based on enterprise values (EV) to sales. But today, Nvidia trades for a whopping 32 times, while Intel trades for less than 2 times EV to sales.

Nvidia’s high-flying stock anticipates ongoing Hall of Fame results, while Intel’s depressed stock anticipates endless disappointment. It reflects a company that will continue riding the bench at the Little League level for a long while.

But therein lies today’s opportunity.

Even modest signs of improvement could propel Intel to much higher levels. And I believe the company’s long-term strategy will succeed… and generate substantial profit growth over the long term.

The Worthy Cost of AI Investments

Intel’s core strategy is to become the dominant domestic manufacturer of semiconductors, while also boosting the competitive strengths of the chips it designs.

These goals are still within reach, but they are expensive and difficult to achieve. Intel is spending tens of billions of dollars to advance its goals, which is crippling its near-term profitability and straining its balance sheet.

The higher the price tag increases, the fewer the investors who applaud Intel’s strategy. They believe it is simply too costly and too risky. Maybe so, but Intel does not have the luxury of resting on its laurels.

No tech company ever does.

The business of technology is always and forever a business of rapid obsolescence. That’s why it is a business that requires massive, ongoing capital expenditures and research and development… especially in the wild, wild world of artificial intelligence.

AI is the most creative – and destructive – technological force that humanity has ever encountered, which is why all the major technology giants are ramping up their capital spending to prepare for it.

Back in January, for example, Meta Platforms Inc. (META) announced that it would spend about $30 billion this year on new tech infrastructure. In April, the company raised that figure to $35 billion. Then, Meta CEO Mark Zuckerberg bumped the number again to $37 billion.

Intel is making a similarly massive commitment to the AI-centric world it anticipates. And as AGI advances, Intel could find some success from the technology, especially in robotic developments. As Thomas Yeung mentioned in a recent Fry’s Investment Report weekly update (subscription required)…

Figure 2.0 and other humanoid robots, for instance, require the type of onboard processing where Intel has traditionally excelled. Though Nvidia will continue to dominate data center-level compute, standalone robots will require the type of integrated AI chips that Intel is now developing. Autonomous vehicles and other smart devices will see similar requirements.

So, while critics may say that Intel cannot afford to make these AI investments, I say that it cannot afford not to make them.

To discover other ambitious companies that will prosper as we head toward super-advanced AI, be sure to check out my The Road to AGI Summit. Once again, you can access the replay by clicking here.

Regards,

Eric Fry