This company must be a fraud.

This is a bold claim to make on national television in front of millions of people.

But this is how Andrew Left, CEO of Citron Research (a notorious short seller), described a technology company on CNBC in September 2017.

Fraud is a serious offense, and usually this sort of accusation does not get thrown around lightly. So, when folks hear that kind of serious claim on TV, they often believe it.

This is what Ubiquiti Inc. (UI) was up against when Andrew Left pointed his guns in its direction.

The high-growth networking technology company designs and sells wireless communications and enterprise networking solutions for service providers and businesses worldwide.

Left called Ubiquiti a fraud because he believed there were several “red flags,” including exaggerating the size of its user community, accounting irregularities and high executive leadership turnover. In the immediate aftermath of the news, Ubiquiti fell 8%.

And then, as the rumors spread, the stock tumbled.

This is exactly what Left wanted. You see, short-selling is a trading strategy where you borrow shares of a stock and sell them at the current market price. The idea is to buy them back later at a lower price to return to the lender, profiting from the decline in the stock’s value.

Simply put, short sellers want the stock to go down.

Firms like Citron, Hindenburg, Muddy Waters and others take short positions in companies and issue research reports that are critical of them. Now, sometimes there are merits to the claims, but a lot of times they simply exaggerate or throw around wild accusations, hoping to drive down the price.

Here’s how Ubiquiti’s CEO, Robert Para, initially responded:

Now, the question is: Did those claims have any merit?

Despite the short-seller attack, Ubiquiti continued to post strong earnings. In the first quarter following the Citron report, the company reported revenues of $245.9 million, a 20.1% year-over-year increase. It achieved a gross profit of $111.7 million, representing 45.4% of revenues net income of $74.9 million. Earnings per share came in at $0.92.

And in the quarters following the Citron report, the company beat analyst expectations multiple times, demonstrating resilience in both revenue growth and profitability. Ubiquiti’s robust fundamentals, including expanding margins and strong cash flow, ultimately proved that the accusations lacked substance.

I’ll put it this way. I felt comfortable enough to add the stock to my Growth Investor service back in May 2021. We ended up walking away with a 90% gain in December 2021.

More importantly, Ubiquiti is still around today.

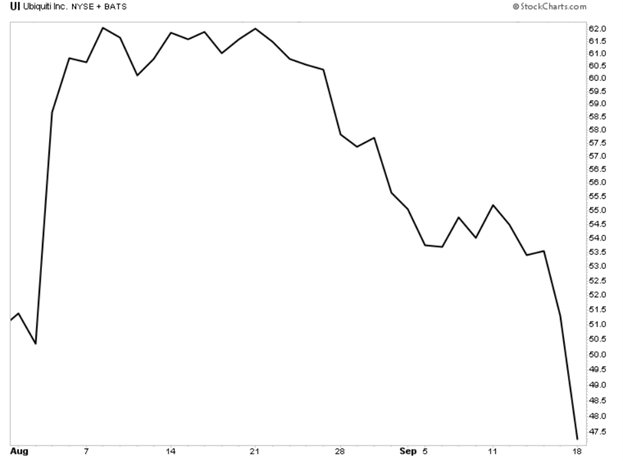

If we look back, the Citron report in 2017 was simply a blip in the grand scheme of things.

In the chart below, the red arrow indicates the sharp drop it took when the report was released. But the stock has since recovered the losses and posted some impressive gains…

The point is the claims ultimately subsided, and the company’s fundamentals ultimately spoke for themselves.

In the end, Para had the last laugh.

But here’s the thing…

The sharp drop caused by Citron damaged the portfolios of a lot of hardworking people. I’m willing to bet that many people were scared away from this stock completely, causing them to miss out on the long-term 500%-plus gain that followed.

I have a problem with that.

These are people who were planning to retire someday. Maybe take a nice vacation with their spouse. Or pay for their daughter’s wedding.

And Left? He is currently facing both civil charges from the Securities and Exchange Commission (SEC) as well as criminal charges from the Department of Justice (DOJ).

In short, I think short sellers are scum, folks.

And I bring this up because the case with Ubiquiti shares some striking similarities to what happened to Super Micro Computer, Inc. (SMCI) last August. If you haven’t followed along, let me break it down for you in today’s Market 360. Then, I’ll review the latest developments and why I continue to believe it’s worth holding today. Plus, I’ll share where you can find strong stocks with superior fundamentals that are great buys right now.

What Happened with Super Micro

Now, Super Micro is a leading high-performance server provider, specializing in energy-efficient, liquid-cooled hardware that’s ideal for data centers working on artificial intelligence. This made it a key player in the AI Boom since its products were best-in-class. In fact, demand for Super Micro’s products was insatiable – making it one of the hottest stocks on the market.

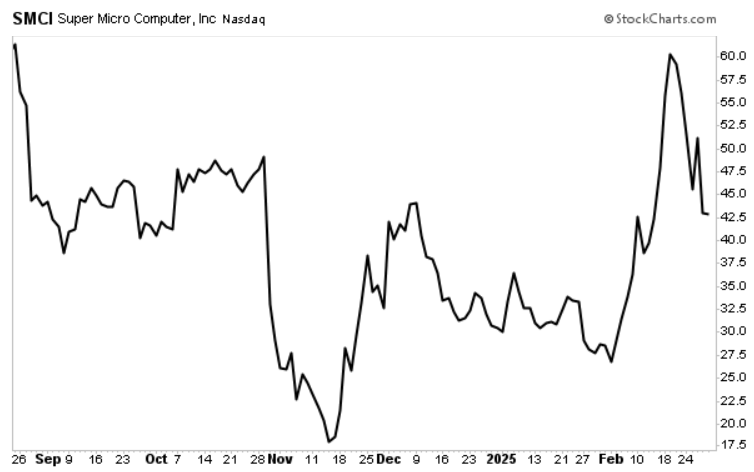

On August 26 last year, Super Micro fell victim to a report from another notorious short-seller, Hindenburg Research. A former employee also claimed that Super Micro was committing accounting violations and filed a whistleblower report.

The DOJ took Hindenburg Research’s allegations seriously and issued a probe to investigate. Super Micro had to delay the filing of its annual 10-K report to the SEC as a result.

Then on October 30, Super Micro dropped more than 30% after its auditor, Ernst & Young, resigned, citing concerns over the company’s controls. The stock fell another 12% the following day after CNBC’s Jim Cramer said that Super Micro might get delisted from the NASDAQ. The company did get a deficiency letter, and it had until November 16 to comply.

After hiring a new auditor, Super Micro was ultimately granted another extension to file its 10-K and 10-Q reports to the SEC. There was a three-month investigation conducted by an independent Special Committee. They found no evidence of fraud or misconduct from management or the board of directors.

Now, the new deadline was Tuesday, February 25. Now, the new deadline was Tuesday, February 25. Shares of SMCI surged by roughly 49% in anticipation of meeting the filing requirements – which it did meet this week.

But the damage was done. You can see the carnage investors experienced in the chart below.

That’s quite the wild ride, folks.

Why Fundamentals Matter

When the news of this fiasco first broke and the stock began to fall, Super Micro was downgraded to a D-rating in Stock Grader (subscription required). Normally, that means it’s an automatic sell. But I advised my Growth Investor subscribers to hold it. Many of them thought I was crazy for doing that, and I don’t blame them. Super Micro was becoming volatile, and no one likes too much volatility when their hard-earned money is on the line.

But the only thing I hate worse than volatility is a scummy short seller jerking people around, manipulating them to make a buck.

The fact is Super Micro has superior fundamentals. The numbers speak for themselves.

Its most recent update showed second-quarter fiscal 2025 sales between $5.6 billion and $5.7 billion, translating to 54% year-over-year growth. Analysts were expecting sales between $5.0 billion and $6.0 billion.

Looking to the third quarter, it expects total sales between $5.0 billion and $6.0 billion. That’s just a hair below analyst expectations for $6.09 billion. I should also add that Super Micro revised its full-year fiscal 2025 revenue forecast to a range of $23.5 billion to $25 billion, down from the previous estimate of $26 billion to $30 billion. But that still translates to nearly 60% growth on the low end.

It’s important to keep in mind that Super Micro has an extensive order backlog – as much as four to five years. I used to work in accounting, so I know that falsifying an order backlog is nearly impossible to do.

The bottom line is that fundamentals matter. Short sellers are scum and they’re just looking for ways to ruin the party.

You do not want to get me in a room with these people. In fact, I said in a CNBC International interview in February 2024 that I would fight them after they alleged that NVIDIA Corporation (NVDA) was round-tipping. Its phenomenal fourth-quarter 2024 earnings results showed that its growth was quite real, and the stock rallied about 16% in the wake of its strong numbers. There was absolutely no truth to the rumors.

I should also mention that Hindenburg Research is now out of business. On January 15, 2025, founder Nate Anderson announced that Hindenburg would be closing its doors in a personal note to his employees.

I find this very interesting.

With all of that being said, Super Micro is still not out of the woods. They have a lot of ground to make up. The stock surged as much as 23.4% on Wednesday after the company filed 10-K and 10-Q reports, but then gave up those gains after NVIDIA’s earnings triggered a tech selloff.

In the end, I think this is simply a blip in Super Micro’s history. Just like it was with Ubiquiti.

What to Invest in Next

So now, you’re probably wondering where else you can find stocks with superior fundamentals like Super Micro.

Well, look no further than my Growth Investor service. My recommendations are characterized by 26% average sales growth and 556.1% annual earnings growth. Plus, the average earnings surprise during this earnings season is 43.3%.

And you couldn’t join at a better time. I just released my March Monthly Issue to my Growth Investor subscribers this afternoon with four brand-new recommendations. All four of them have positive analyst revisions, which typically precede future earnings surprises and earnings surprises mean that they’ll jump up higher, putting more money in your pocket.

Click here to join now and gain immediate access to my March Monthly Issue. You’ll also receive full access to all my Special Market Podcasts, Weekly Updates and more!

(Already a Growth Investor subscriber? Click here to log in to the members-only website.)

Sincerely,

Louis Navellier

Editor, Market 360

The Editor hereby discloses that as of the date of this email, the Editor, directly or indirectly, owns the following securities that are the subject of the commentary, analysis, opinions, advice, or recommendations in, or which are otherwise mentioned in, the essay set forth below:

NVIDIA Corporation (NVDA) and Super Micro Computer, Inc. (SMCI)