There’s less than one week until Christmas.

Airports are jammed. Shopping carts are full. And most investors are already halfway out the door – mentally checked out, ready to stop watching every tick and go be with their families.

That’s when markets tend to get dangerous, folks.

Because the headlines don’t stop just because the calendar says “holiday.” And the biggest surprises often land when nobody’s paying attention.

Case in point – the Federal Reserve.

Even after last week’s rate cut, several Fed members are still sounding uneasy. They’re pointing to missing inflation data from the government shutdown… and they’re warning inflation may stay above their 2% target for years.

Meanwhile, you have unscrupulous short sellers and members of the media who are trying to throw water on the AI boom, which is very real – and in fact, accelerating.

In other words, there are a few Grinches lurking around the market – and within the Fed – and they’re threatening to spoil a potential Santa Claus rally for the rest of us.

That’s why this week’s economic reports were so important: employment, U.S. retail sales and the Consumer Price Index (CPI).

Because after delays caused by the government shutdown, these reports should finally shed some light on what’s really going on.

So, in today’s Market 360, I’ll dig into the latest numbers and break down what they’re really telling us. I’ll explain what the Fed now has to confront heading into 2026, why the labor market matters more than inflation at this point and how that shift changes where the best opportunities are likely to emerge next year. Then, I’ll walk you through a profit opportunity built specifically for this transition.

Let’s dive in.

What’s Really Happening in the Labor Market

The U.S. economy has been resilient this year, and GDP growth is heating up. The Atlanta Fed currently anticipates 3.6% GDP growth in the third quarter, for example.

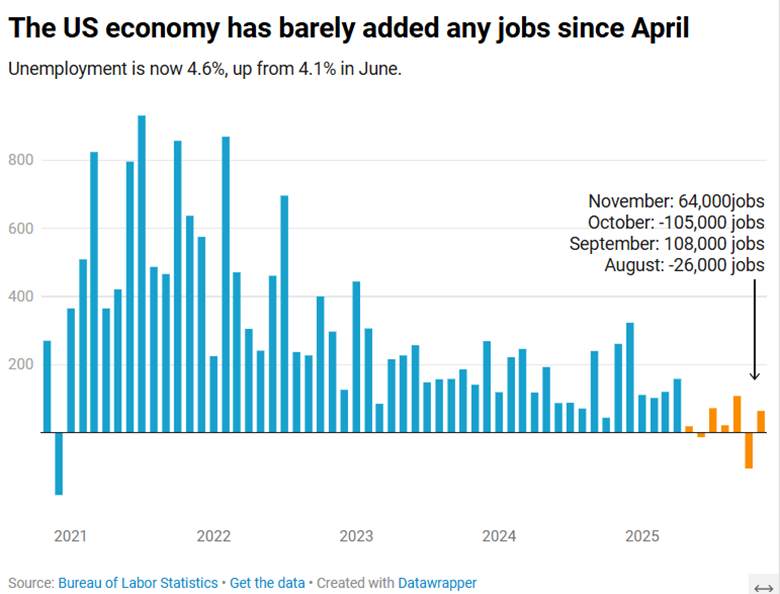

But despite the robust economic growth, the U.S. economy is not firing on all cylinders. The jobs market, in particular, has struggled of late. ADP recently reported that 32,000 private payroll jobs were eliminated in November, compared with estimates of 10,000 jobs added.

So, this is why folks were eager to get their hands on the employment numbers released on Tuesday.

The Labor Department revealed that 64,000 jobs were added in November, compared to estimates of 45,000 jobs. The delayed October data, though, showed that 105,000 jobs were lost that month.

In turn, the unemployment rate rose to 4.6% in November, up from 4.4% in September. The consensus estimate only expected an unemployment rate of 4.5%.

This is the highest unemployment rate reported in four years.

As you know, the jobs data was delayed due to the shutdown, and many didn’t trust the recent numbers, including Fed Chair Jerome Powell, who suggested there may be an overstatement in the Labor Department’s numbers.

But the bottom line is that there hasn’t been any substantial job growth since April.

The government shutdown may have distorted the data. But it’s not the whole story. More companies are slowing hiring and trimming headcount as they focus on efficiency – producing more with fewer workers. That helps explain why GDP growth can remain strong even as job creation cools.

Federal Reserve Chair Jerome Powell has acknowledged this possibility, noting that it’s still too early to measure the full impact of new technologies on employment. At the same time, he warned of “significant downside risks” if these trends accelerate faster than expected.

For workers, especially younger Americans entering the job market, this has made conditions feel tougher. But with a couple more key interest rate cuts to help, this will look less like a collapsing labor market and more like one in transition – and I’ll explain why in a moment.

But first, the next question becomes obvious: Are consumers actually pulling back?

Cutting Back or Splurging?

This brings us to our next report, U.S. retail sales, released Wednesday morning.

For October, retail sales were unchanged from the previous month. Economists expected a 0.1% increase.

A 1.6% decline in sales at motor vehicle and auto parts dealerships weighed on the headline number, reflecting in part the expiration of federal incentives for electric vehicles.

But when vehicles and auto parts are excluded, retail sales rose 0.4% month over month – double economists’ expectations.

Digging further under the hood, spending remained firm in several key categories. Furniture store sales climbed 2.3%, food and beverage stores rose 0.3% and clothing and accessories sales increased 0.9%.

On the flip side, there was a 0.4% decline in food services & drinking places, suggesting consumers are becoming more selective with discretionary spending.

Taken together, this doesn’t look like a consumer in retreat. It looks like households are adjusting how – and where – they spend, even as job growth cools.

Why Inflation Is Cooling Off

Finally, we turn to the CPI report. It was a bit tricky to interpret because it covered two months of data due to the government shutdown. Even so, the results came in notably better than expected.

Headline CPI rose 2.7% on a yearly basis in November, well below economists’ expectations for a 3.1% increase. Core CPI, which strips out food and energy prices, rose 2.6% over the previous year, also below forecasts.

One component I always pay close attention to is owners’ equivalent rent, or OER. This measures the imputed rent homeowners would pay if they rented their own homes.

Now, shelter costs overall make up about a third of the CPI. And they’ve been responsible for a significant chunk of inflation readings for much of this year.

But I have pounded the table, saying that these numbers would fall and that the Fed needs to get ahead of this.

Well, folks, OER reading has now fallen for four straight months.

What Needs to Happen Next

Some investors continue to question the CPI data. But the bigger issue isn’t whether inflation is easing – it clearly is. The real question is what comes next.

The Fed has a dual mandate of taming inflation and maximizing employment. At this point, inflation pressures are cooling, while the labor market is showing clear signs of strain.

So, I think the Fed needs to cut rates two more times in 2026, bringing it down to a “neutral” rate, which should help stabilize the economy.

But the main thing I want you to do is to cheer up and enjoy the ride.

I am unbelievably bullish for the New Year.

Yes, unemployment is the highest it’s been in four years. Why? Because we’re getting more efficient, and those productivity gains will further add to GDP growth.

As I mentioned before, companies are now relying more on AI. Is this disruptive? Of course it is, but it’s a massive investment opportunity that you shouldn’t overlook.

It’s what I’m calling the Economic Singularity.

It’s a full-scale reset of how work gets done – where software increasingly outperforms humans at speed, scale and cost. Tasks that once took hours are now completed in minutes. Sometimes seconds. And this shift is already reshaping which companies will thrive – and which ones will fall behind – in 2026 and beyond.

That’s why I’ve put together a special presentation to walk you through exactly how to position yourself for this transition. In it, I explain which stocks are most vulnerable as this shift accelerates – and which companies are best positioned to benefit as efficiency becomes the dominant competitive advantage.

If you want to be on the right side of this change heading into the New Year, I encourage you to watch the presentation now.

Sincerely,

Louis Navellier

Editor, Market 360