Editor’s Note: Eric Fry here. Today, I have a special guest column from Charles Sizemore, Chief Investment Analyst at InvestorPlace‘s publishing partner, The Freeport Society. Charles has released a brand-new special report to help launch his free e-letter, The Freeport Navigator — and it’s pretty exciting stuff. It’s called 5 Unapologetically Profitable Stocks for 2024. Click here to get your FREE copy and to sign up for Charles’ FREE letter.

Take it away, Charles…

A trillion dollars is such a big number that it’s meaningless.

It’s inconceivable, really, until you think about what you could do with that much money. The author Rowan Hooper reckons you could end global poverty… settle on the moon and explore the solar system… build quantum computers… and increase the human life span.

But what you can’t do with a trillion dollars – as our federal government is finding out the hard way – is pay it back.

In 1987, the totality of the federal budget – every nickel that Uncle Sam spent that year – crossed $1 trillion for the first time.

It’s never been less since then.

In 2009, the federal budget deficit – or the amount our government borrowed to spend – crossed $1 trillion for the first time. That was a pearl-clutching moment. Now, it’s expected.

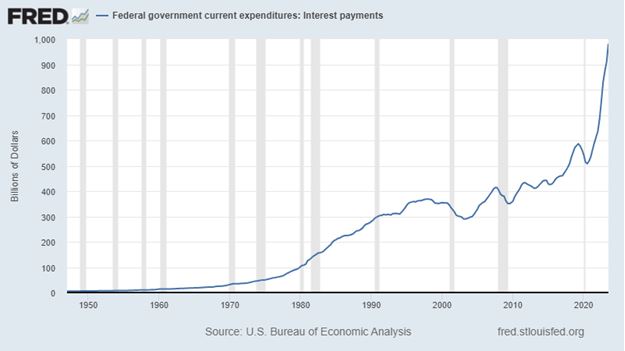

This year marks yet another tragic trillion-dollar milestone. Just last month, the annual interest paid on our national debt is estimated to have crossed the $1 trillion mark for the first time. I say “estimated” because government accounting being what it is, we won’t know the official numbers for a while.

It gets worse. Those trillions of dollars of debt are coming up for refinancing… at much higher rates. That means interest costs won’t be dipping below $1 trillion any time soon.

Even if we balanced the budget tomorrow, the interest expense would still continue to rise as older lower-interest bonds are rolled into newer higher-interest ones.

Unfortunately, there’s about as little chance of me being drafted to play point guard for the Lakers at the ripe old age of 46 with two creaky knees and a blown-out rotator cuff on my shooting arm than there is of our government balancing its books tomorrow.

In reality, the Congressional Budget Office sees the budget deficit widening from $1.4 trillion in 2023 to $2.7 trillion by 2033. Most of that expansion – 53% – will be due to interest paid on debts already racked up.

Our “primary” budget deficit, or current spending over and above current revenues, will be “only” $1.3 trillion.

It’s all, quite literally, mind-boggling.

Unfortunately, I have more bad news…

Waiting on Something to Break

Our budget deficit won’t be $2.7 trillion in 10 years. Not because Congress is going to sober up and rein in spending. Instead, because something will break long before that happens.

The so-called “Bond King,” Jeff Gundlach, manager of the DoubleLine family of bond funds, says that a “crack of doom” moment is needed to make both Democrats and Republicans take the deficit seriously. A bona fide crisis.

What will that crisis be?

Your guess is as good as mine.

A rational person might have assumed that Fitch lowering Uncle Sam’s credit rating might have been it.

It wasn’t.

It didn’t make one iota of difference to government spending plans.

Will another downgrade matter?

Maybe. Maybe not. But we’ll find out soon enough because there is no way – in any reality, parallel or otherwise – in which regular $2.7 trillion deficits can be the norm by 2033.

Something will break before then.

Will Social Security Be the Straw That Breaks the Camel’s Back?

The current national debt is just over $33 trillion, of which $6.8 trillion is “intragovernmental,” or debt the government owes itself.

Why does our government owe itself so much money?

Because it’s borrowed from the Social Security trust funds.

Here’s the dirty little secret on the Social Security trust funds: There actually is no trust fund. There never was.

In the years when Social Security ran surpluses, bringing in more in tax revenues than it paid out in benefits, that extra money wasn’t left sitting in a bank account somewhere. It was invested in government bonds.

What that means is that the money ostensibly set aside for Social Security got spent elsewhere by Congress and was replaced with an IOU.

Social Security “surpluses” masked deficits elsewhere. But it at least made the accounting look “good.”

Now, even this accounting fantasy is untenable because the retirement of the baby boomers has put Social Security into deficit. The imaginary trust fund is estimated to be fully depleted by 2034.

Now, what seems more likely to you?

That 80 million baby boomers accept a Social Security check that’s 20% lower each month in order to match current system inflows…

Or that they demand that their congressperson make up the shortfall by pulling spending from elsewhere and divert it to Social Security?

We know how this ends.

Congress will play with tax rates, lifting the cap on earnings subject to Social Security FICA taxes. They’ll make benefits fully taxable. They may even reduce the benefits paid to higher-income retirees who “don’t need it,” and Social Security effectively becomes welfare.

In fact, that’s exactly what former New Jersey governor Chris Christie said in the November 8 Republican debates: “The fact is, on Social Security, it was established to make sure that no one would grow old in this country in poverty, and that is what we have to get back to. Rich people should not be collecting Social Security.”

Call me cynical, but I imagine Congress will end up considering anyone with two nickels to rub together to be “rich.” But I also know that they can’t cast that net too widely because they don’t want to deal with legions of angry voters wanting their checks back.

The easiest way to make the Social Security problem go away is to play with the inflation adjustments. Sure, your guaranteed payout won’t change, but it will buy a little less with each passing year.

Inflation is also a great way to make the national debt problem go away too. Paying debts in devalued money is a trick as old as debt… and as money itself.

You’d be crazy not to have at least a little inflation protection in your portfolio.

You can find some of the best investments for that in my free special report called 5 Unapologetically Profitable Stocks for 2024 (you can get that report by clicking here).

2024 is shaping up to be a chaotic year. We’re on the brink of war, high interest rates are wiping out the middle class, and recession seems all but certain. But this is an opportunity for smart traders. And so, in my new free report, I outline the five stocks best-positioned for 2024’s volatility.

To life, liberty, and the pursuit of wealth.

Sincerely,

Charles Sizemore

Chief Investment Strategist, The Freeport Society