Hello, Reader.

Tom Yeung here with today’s Smart Money.

When most people start cooking, it’s easy to assume fancy cookbooks will be a guiding light in making tasty, picture-perfect dishes.

But as any seasoned chef – whether at home or an upscale restaurant – will tell you, the real magic happens when you watch a family member whip up a cherished recipe from memory.

Well, this similar principle applies to the simple yet specialized job of analyzing companies.

When I started working on Wall Street as a buy-side equity analyst, I was usually given two sets of reports for each company we covered…

Equity sell-side reports. From investment banks like UBS and Goldman Sachs, focusing on the value of the company’s stock. These reports addressed areas like stock price targets, earnings forecasts, and company outlook. (Here’s a sample of one.)

Credit reports. These reports focused on the debt of a company and were produced by firms like Moody’s and Fitch Ratings. They were more interested in the solvency of a company and rated a firm’s bonds on a AAA to C/D scale.

Now, you might think that equity reports would be more useful.

That’s because years of study demonstrate that equity is the top layer of a company’s value. If a $100 million company is split 50-50 between equity and debt, every additional $1 million in value goes directly to the stock.

For instance, if the company’s value increases by $1 million, the equity would rise to $51 million while debt remains at $50 million. Conversely,if the company’s value goes down by $1 million, then it’s the equity value that suffers, dropping to $49 million while the debt maintains its $50 million value.

Our theoretical firm would have to lose $50 million in enterprise value before debt is affected! So, we might imagine that equity analysts would be more sensitive to changes in a company’s value and give a fellow young equity analyst the necessary information.

However, I quickly learned that the opposite is true…

Debt Markets Say “Buy”

In my experience, sell-side companies like UBS and Goldman were always too bullish. They would paint the rosiest picture, claiming unlimited upside and zero risk, and saying “buy, buy, buy!” With many of these investment banks as bookrunners for the companies they covered, it was their unspoken jobs to be bullish to sell more stock.

“Chinese Walls” between equity research and investment banking were rarely enforced.

Meanwhile, debt ratings agencies like Moody’s and Fitch would consistently publish accurate reports about the status of a company.

This accuracy stems from credit rating agencies’ greater financial liability for egregious errors that deceive investors, and so they have less incentive to promote troubled firms. The business is more interested in return of investment, not return on investment.

Detachments from stocks allow debt analysts to have a clearer view about markets. Troubles at Enron in the early 2000s, for instance, were flagged by S&P and Fitch long before equity analysts soured on the high-priced firm.

This predictive ability extends to debt markets as well. Since 1960, every recession has been predicted by a particular occurrence in debt markets, and this unusual event has only yielded one false positive in that period. 2022 to 2024 would mark the second false positive.

Meanwhile, stock markets are far too skittish to predict much at all. Over the same period, the S&P 500 saw 18 years where a bear market occurred (prices drop >20%) and another 20 years where a correction happened (prices drop 10%-20%).

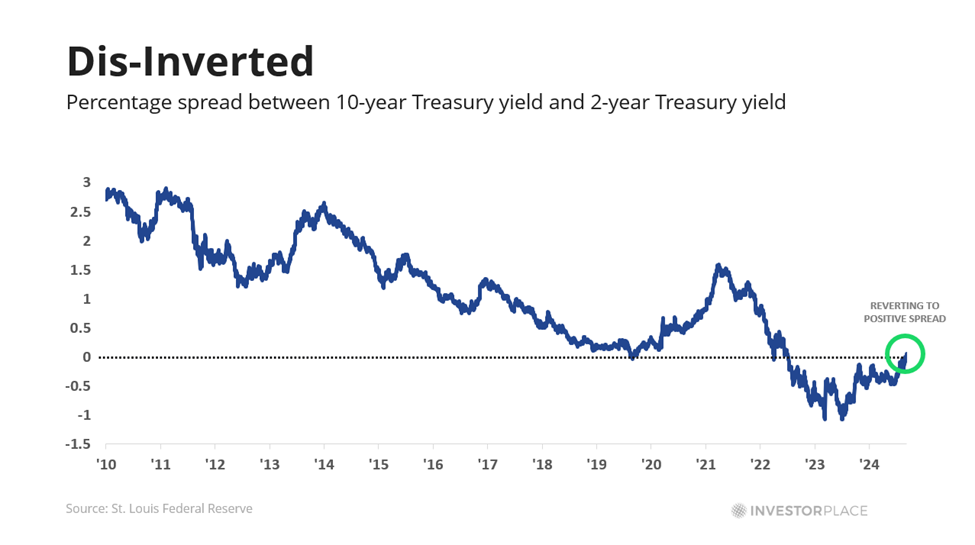

That’s why a special event in debt markets last week is so notable.

Last Friday, the 10-Year Treasury yield rose above the 2-Year yield for the first time in over two years. This “dis-inversion” (or reversion) of the spread is an extremely bullish sign because it undoes the yield inversion we’ve seen since June 2022 – a typical warning of an upcoming recession. Friday’s “dis-inversion” means the recession alarm has now been lifted.

This also happens to be the same “particular occurrence” I wrote about earlier. As recessions approach, the yield of 2-year bonds tend to rise above those of 10-year ones; debt investors anticipate near-term interest rate cuts and make their bets accordingly. As the risk disappears, the same traders then unwind these bets, pushing yields of long-dated bonds back to where they started.

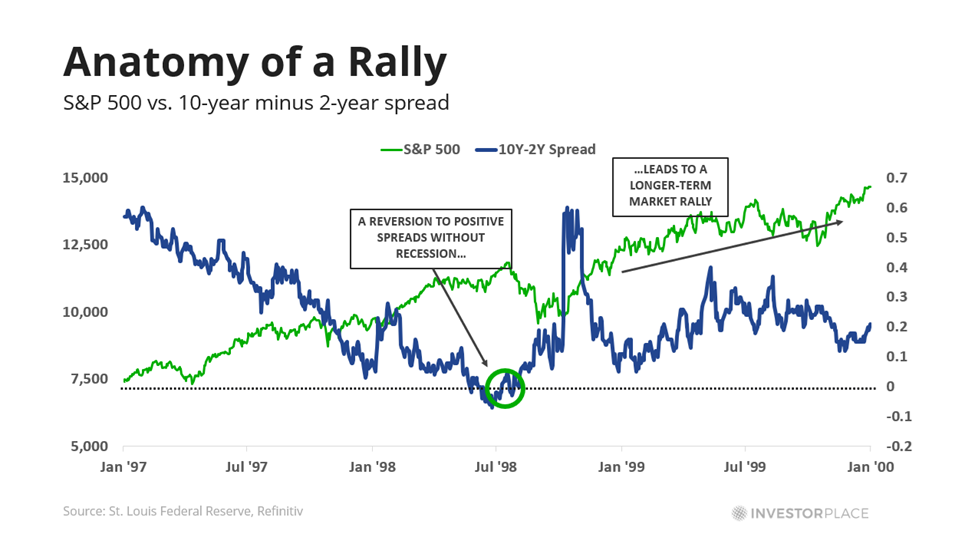

That’s excellent news for stocks, especially ones exposed to the business cycle. Robust economies signal strong employment, mild inflation, and rising stock markets. Last week’s dis-inversion is an echo of the late 1990s, which saw a stock market boom (and a bubble in tech stocks) through 2001.

And so, we remain highly bullish on our commodity-based bets in Fry’s Investment Report, and even more so on mean-reverting ones in tech and healthcare. These low price-to-earnings companies benefit as P/E ratios rise and earnings catch up – a pair of lucky breaks. They also avoid the sort of bubble-like stocks that turned the dot-com boom into a bust.

It’s also why we’re consciously downplaying the recent downward moves by equity markets.

This does not change our macro outlook. We believe that shares of AI firms were simply too highly priced to start, which is why Eric recommended his paid members take profits in some notable tech firms over the past several months in the Investment Report (go here to find out how to join them).

Lower equity values now provide a more attractive entry point into companies whose outlooks have frankly not changed by the magnitude their share prices suggest. Sometimes the most valuable insights come from unassuming sources, much like the outperforming nature of your grandmother’s reliable chicken noodle soup.

Regards,

Thomas Yeung

Markets Analyst, InvestorPlace