- Inflation is at a 40-year high, but it’s impacting everyone differently.

- Inflation hurts poor people and those on fixed incomes the most.

- Inflation helps borrowers and investors in stocks, real estate, and commodities.

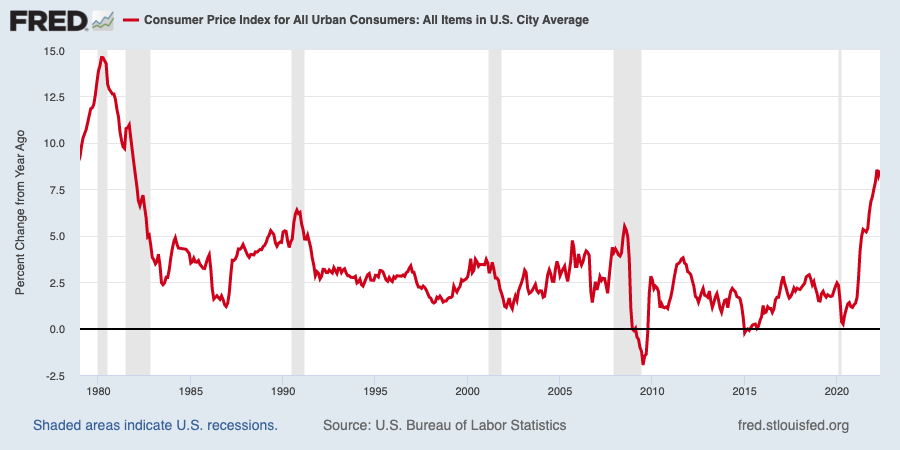

A new generation of investors is grappling with the dangers of inflation. Last week, we learned the Consumer Price Index (CPI) rose 8.6% from a year ago, marking the most significant annual jump since 1981. And the price hikes are hardly hidden — they’re flashing in your face in gas stations and supermarkets across the nation. Considering the new and seemingly sticky regime of rising prices, it’s worth asking: who does inflation hurt and help most?

The answers are less complicated than you might think. Let’s take a closer look at each part of the question, starting with the victims of inflation.

Inflation Hurts Poor People and Savers

Click to Enlarge

The pains of inflation aren’t doled out equally. Consumers who lack assets and live paycheck to paycheck on meager incomes are undoubtedly hurt the most. Lower-income earners spend a larger percentage of their take-home pay on essentials like food, shelter, and gas. Thus, a sharp rise in prices takes a bigger bite out of their income. For example, let’s say Wealthy William only spends 20% of his income on the essentials mentioned above. Meanwhile, Poor Paul must spend 60% of his income on them. Consider what would happen if inflation causes prices to rise 10%.

The cost for William would rise from 20% to 22% of his income. The cost for Paul would rise from 60% to 66% of his income. While inflation’s toll only required 2% more of Wealthy William’s pay, it took 6% more from Poor Paul.

But even those who own assets aren’t immune to the ravages of inflation. The long-term average inflation rate in America has been 3%. If you’ve owned assets like cash, savings accounts, certificates of deposit (CDs), fixed annuities, and bonds that have not grown by at least 3% per year, then your real returns have been negative. Since risk-averse savers tend to favor these vehicles, they are another cohort particularly vulnerable to inflation.

Here’s another way to think about it. Inflation translates into rising costs. Assets like those mentioned above generate fixed income. Having a fixed income in a rising cost world is a surefire way to lower your standard of living over time.

Inflation Helps Investors and Borrowers

If inflation is the foe of savers, then it’s the friend of borrowers. Indeed, indebted consumers are uniquely positioned to benefit from inflation. It lightens the burden of debt by making money worth less. Take a 30-year fixed mortgage, for instance. Three decades ago, taking out a $100,000 mortgage to purchase a house may have been a big deal. Now, it’s nothing. $100,000 isn’t what it used to be.

With a long-term mortgage, the last payment you make won’t hurt near as bad as the first because your income will rise over time. Though incomes don’t necessarily move in lockstep with inflation, the rising cost of living eventually drags wages higher. For instance, the median U.S. household income when I was born in 1984 was $26,430. In 2020, it was $67,521. The cost of a mortgage as a percentage of your pay falls over time.

The second cohort of people aided by inflation is investors. We’re specifically referring to those who have invested in the right types of assets. Namely, the ones that have grown beyond the pace of inflation, which is more than 3% annually. That’s how true wealth is created. Stocks, real estate, and commodities are standard vehicles used by intelligent investors to combat inflation.

Of these three, stocks have been the best way for regular investors to create long-term wealth effortlessly.

The Best Way to Protect Yourself From Inflation: Stocks

Since 1926, the S&P 500 has been up approximately 10% yearly. That’s the nominal return. If you strip out the 3% inflation, the real return is 7%. Equity investors have grown their purchasing power by more than double the inflation rate. Not bad.

Here’s one of the most beautiful things about using equities as your vehicle for beating inflation — it doesn’t require any effort. All you must do is stay the course and allow the best companies on the planet to do the heavy lifting through their pricing power. Here’s how the logic goes.

First, inflation increases the cost of labor and materials. Second, companies pass on these elevated costs to consumers by raising the price of their goods and services. Third, even if they sell the same number of widgets, revenue and earnings still rise in nominal dollars. Fourth, because of rising earnings, stock prices can increase without valuations going into orbit. Therefore, dividend payouts can also increase.

While equities can suffer in the short-term when inflation fears come to a head, like now, history has taught us they never stay down. This time will prove no different.

On the date of publication, Tyler Craig did not have (either directly or indirectly) any positions in the securities mentioned in this article.