Its value as a barometer for an entire earnings season had diminished considerably over the years, but to the extent Alcoa (AA) is still the trend-setter for corporate America’s quarterly results, Q2’s marketwide earnings may be a little lackluster.

Although the company turned a profit, earnings per share of Alcoa stock fell short of estimates.

On the flipside, although the Alcoa earnings figure came up short of expectations, revenue topped estimates, offering a little hope that the turnaround efforts from AA are taking hold even though aluminum prices are still suppressed.

Indeed, the fact that Alcoa managed to turn a profit at all in its second quarter is impressive in light of Aluminum prices that have been beaten down by a surge in China’s exports of the commodity. Earnings impressed investors enough to send the stock up 3% as of this writing.

But today’s buyers are making a mistake.

Alcoa Earnings, By the Numbers

Last quarter, the company earned operating income of $250 million, or 19 cents per share of Alcoa stock, on revenue of $5.9 billion. The bottom line rolled in better than the 18 cents per share of AA the company posted in the same quarter a year earlier, when it generated $5.8 billion worth of sales.

The bad news? Analysts were expecting earnings of 22 cents per share of Alcoa stock. On the other hand, the revenue figure for Q2 was better than the $5.8 billion the pros were collectively expecting.

The weak points of the Alcoa earnings report were, largely as expected, alumina and primary metals.

Operating income for its primary metals division fell from $97 million a year earlier to only $67 million this time around, and was well below the $187 million earned in Q1. Its flagship alumina division’s after-tax operating income of $215 million was down slightly on a sequential basis, from $221 million, though it was well up from the $177 million earned in the second quarter of 2014.

As for its global rolled products it made forward progress on a year-over-year basis as well as compared to its first quarter. Ditto for its engineered products arm.

Broadly speaking, the company’s ongoing reduction in aluminum smelting and refining capacity along with its development of high-end aerospace solutions continues to pay off.

That being said…

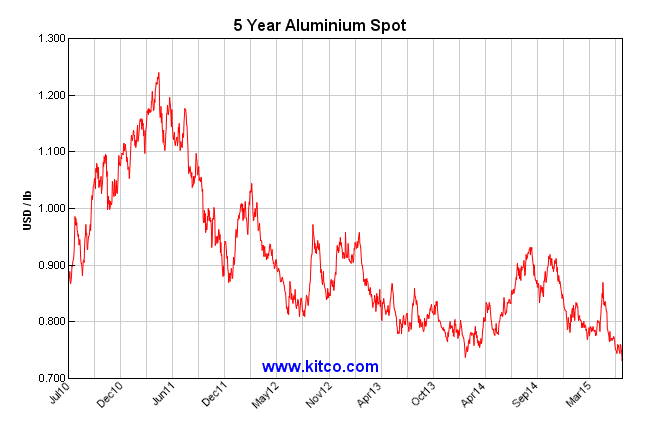

Aluminum Price Trends

As diversified as Alcoa is aiming to become, it’s still quite subject to aluminum prices. And prices have been anything but fantastic.

As of yesterday, aluminum spot prices are at new 52-week lows near 73 cents per pound. That also happens to be a new multi-year low, and a far cry from the price of $1.24 per pound that Alcoa and its peers like Century Aluminum (CENX) and Kaiser Aluminum (KALU) were enjoying for a bit back in early 2011. That strength was clearly not meant to last.

Click to Enlarge

The cause for the price implosion wasn’t, and still isn’t, a lack of demand. In fact, along with the Alcoa earnings report the company maintained its expectation that the global aluminum market would grow to the tune of 6.5% this year after growing a hefty 9% last year.

The weak prices are being spurred by massive Chinese exports.

For perspective, China’s aluminum exports grew 20% on a year-over-year basis in May. And that wasn’t anything new or unusual. Year-to-date, aluminum exports averaged 35% higher than the year-to-date total at this time in 2014.

The good news is that the steep decline in aluminum prices may have finally inspired even China — where the material is sourced quite cheaply — to stop supplying so much of the stuff. Alcoa CEO Klaus Kleinfeld added to Wednesday’s earnings report that he expects the swell of China’s aluminum exports to finally taper off this year.

The bad news? It could still take a while to fully absorb the supply already in storage in addition to the still-hefty output from the country. Alcoa COO William Oplinger predicted China’s oversupply level will hit 2.2 million tonnes in 2015, versus a previous estimate of 1.8 million tonnes.

Bottom Line for Alcoa Stock

While the Alcoa earnings report offers a glimmer of hope, it forces investors to recognize the difference between “better” and “good”.

There are some things that truly are “good” working in favor of Alcoa stock. On most fronts, the numbers and the outlooks are simply not as bad as they used to be. But they still don’t make AA investment-worthy.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities.