On the surface, Apple (AAPL) beat the Street’s estimates. revenue grew to $49.3 billion and gross operating margins held well at 39%. Even growth in China, which many agree is the key to Apple’s future growth, beat estimates, growing by 112% year-over-year.

But let’s pretend you didn’t know the actual results. Say instead you were gauging the Apple earnings based solely on AAPL’s stock performance. Then considering APPL’s nose-dive of 7% you’d no doubt assume Apple earnings were pretty awful.

They really weren’t, though. So what exactly hit Apple stock right where it hurts? Short answer: the Apple iPhone. Surprised? Sure you are; after all, total iPhone revenue grew by an impressive 59% year-over-year. But what was disappointing was that the total number of iPhone units sold fell 22% from last quarter.

That drop touched a very sensitive nerve with investors, because it means iPhone mania may be waning. And that means the bullish story for AAPL stock is over.

iPhone: Too Much of a Good Thing?

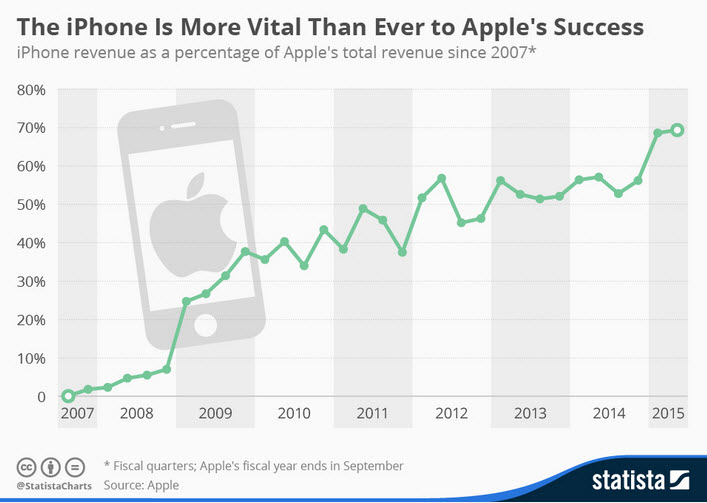

You might remember Blackberry (BBRY) smartphones — formerly the “it” gadget. One of the key reasons that BBRY stock has cratered since August 2007 is that the company’s sole focus was on that one product, relying entirely on the Blackberry for growth.

Click to Enlarge

Once a new wild card emerged in the market — i.e. the iPhone — BBRY found itself very quickly pushed to the margins. Naturally, investors want Apple’s revenue base to be more and more diversified, so as to avoid a fate like BlackBerry’s.

But as time passed, the exact opposite happened. Instead, the iPhone has become a bigger and bigger share of Apple’s revenue base, and that worries investors. It worries investors quite a lot.

What Apple Management Thinks

With the risk being so evident, rest assured that Apple’s management is very much aware of the problem. So what is management’s strategy on this? They want to produce an entire “ecosystem” around the iPhone.

Apple management believes users will still want to buy the iPhone, not simply because it is such a great phone, but because consumers will be able to gain access to Apple’s ecosystem, which is synchronized for a singular experience.

For example, you might want the iPhone because then you have access to the abundance of iTunes, or to link to your iPad or iPod. Or, if you own an iWatch, that would give your iPhone even more value.

The problem is that those other products are lagging iPhone growth by a thick margin. Investors’ main concerns, then, is that if the iPhone hype fades and the iPhone loses its cachet, they will be left with only the mediocre growth of the other segments. Other devices, plus iTunes and its streaming music business, must start catching up to the growth and size of the iPhone segment.

Until then, Apple earnings depend too entirely on iPhone sales.

The Bottom Line

So what is the take away?

First, a no brainer; iPhone sales must return to growth next quarter for investors’ enthusiasm to return — regardless of what Apple earnings actually look like.

And the second? Apple management must starting focusing more and more on enhancing iTunes and other Apple devices. The introduction of a new streaming service launched through the iTunes app is a good start. If iTunes growth begins to catch up with the iPhone, that would validate Apple’s Ecosystem theory.

We need to see if Apple’s plan to build an ecosystem does bear fruit. Then, the worries which pushed investors to sell after Apple earnings could compel them to buy once those worries are dispelled.

As of this writing, Lior Alkalay did not hold a position in any of the aforementioned securities.