Just one quick glance at the price of Alcoa (AA) and you get the sense you’re beholding a bargain. But the truth is not every stock, even one trading at a multi-year low, is a bargain.

With Alcoa stock, it’s not even close.

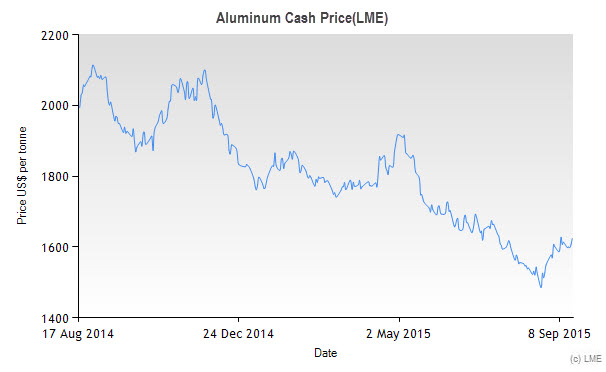

The world’s largest aluminum consumer, China, is in slow-go mode. There has been a significant decline in China’s construction sector, typically a major driver of Aluminum.

Now, with China midway into what may be a hard landing, Aluminum demand has fallen off sharply. All the while, however, Aluminum production levels are still high. This, of course, has created a massive oversupply that keeps pressuring Aluminum prices south.

Pricing pressures on Aluminum show no signs slowing and may even intensify. Given that, it’s hard to see how Alcoa’s core business, Aluminum mining and smelting, could recover.

Too Late for Alcoa Stock

Alcoa bulls had pinned their hopes on Alcoa’s major shift into more downstream production, where margins are significantly higher.

By downstream, we mean sophisticated aluminum parts for autos — e.g. Alcoa’s joint venture with Ford (F) in its Micromill factory. That venture, alongside others, is part of Alcoa’s “grand strategy” to diversify into less price-sensitive, more lucrative undertakings.

Click to Enlarge

The problem is that Alcoa moved a bit too late for the current cycle. While the shift may help Alcoa stock in the next bearish cycle, that’s little comfort now.

The pain is not likely to abate anytime soon, as the majority of profits will still come from smelting and mining. That means that the upside from those ventures will take a bit of time. The good news is it should be enough to balance the weakness in Alcoa’s core business.

Alcoa Stock Trades at a Premium

With a bleak outlook for Aluminum and macro pressures weighing, only a very low valuation could make Alcoa stock appealing. But Alcoa stock is trading at a 20x price-to-earnings multiple, which is higher than most commodity producers. The downside in the company’s business is not priced in.

On top of that, add a rather modest dividend yield of 1.2%. All things considered, you can arrive at only one conclusion: Alcoa still isn’t cheap enough, and the dividend does little to protect the downside.

Rest assured, there will come a time when the tides will turn for Alcoa stock. If AA stock continues to trade significantly lower, it become cheap enough to buy. Otherwise, the Aluminum sector should begin to recover. The way things look now, the former looks to be a more likely scenario.

Given the way things looks now, Alcoa stock needs to be much cheaper to be worth the risk and headwinds.

As of this writing, Lior Alkalay did not hold a position in any of the aforementioned securities.