If there’s a four-letter word on Wall Street — besides the obvious — it’s Valeant Pharmaceuticals Intl Inc (NYSE:VRX). VRX stock has taken down more people and off-roaded more careers than accusations of Russian collusion. Valeant may go down as a name in market infamy, joining the ranks of WorldCom and Enron.

Recently, however, VRX stock made a big splash. Since the close of May 8, Valeant shares are up 43%.

Admittedly, that hasn’t done much in terms of its year-to-date performance, which is underwater by 0.2%. Still, the embattled company has shown serious moxy. Will Valeant Pharmaceutical become great again?

A broken clock is right twice a day, so I wouldn’t put much faith in Valeant stock. But a few analysts are willing to give it a twirl — under very limited conditions. InvestorPlace contributor Nicolas Chahine is one of them. He offers carefully hedged options trades based on the general assumption that the VRX downside is mostly priced in.

With all due respect, I think Mr. Chahine’s cautionary tones before he gave the options ideas offer more value. He wrote, “The bull and bear arguments on this pharma stock are so bifurcated that I can’t tell who is making sense and who is making things up.”

When the waters are as choppy as they are for Valeant Pharmaceutical, you’re better off waiting for a better deal.

No Solid News for VRX Stock

Chahine is absolutely right in asserting that Valeant stock is bifurcated. But at a certain point, you cannot deny the fundamentals. InvestorPlace’s Vince Martin made this loud and clear when he declared that Valeant is still “hot garbage.”

The hot part refers mostly to the company’s Q1 earnings report. Although VRX missed its earnings per share target by a fairly wide margin, management earlier announced that it “paid down debt early after an asset sale to

L’Oreal SA (ADR) (OTCMKTS:LRLCY) closed ahead of schedule. The launch of psoriasis drug Siliq and the approval of surgical platforms in the Bausch + Lomb optical unit offered incremental contributions to sales and earnings.”

The garbage refers to the growing concern that none of these positive developments matter. As Mr. Martin notes, Bausch + Lomb is growing tepidly, and getting absolutely smoked by rival Cooper Companies Inc (NYSE:COO). Worse yet, the contact lens division badly underperforms in the pivotal U.S. market.

The Q1 figures were also a bit of a joke. As Martin points out, the markets apparently celebrated avoiding a catastrophe, as opposed to rejoicing in an actual victory. Both the top and bottom lines missed their respective analyst expectations. The hoopla centered on Valeant Pharmaceutical turning a profit, mostly the result of a non-recurring tax benefit.

It’s fine to be lucky every once in a while. The Valeant story, though, is drastically different. Essentially, it’s a stock that will only do well on the capriciousness of chance.

Valeant Has Too Much to Prove

Admittedly, that statement could describe a lot of things, not just VRX stock. However, understanding the odds is a big part of risk analysis. And like playing slots in a Las Vegas casino, the odds simply don’t favor the gambler.

For Valeant stock, I’m worried about its declining earning power. We all know that based on the Altman Z-score, Valeant Pharmaceutical has struggled in varying degrees of distress. What is most problematic is that of the five categories that determine the Z-score, earnings continue to disproportionately lag.

Unfortunately, this is the most critical factor for any company. If an organization cannot generate income, investors are more likely to jump ship towards a firm that can.

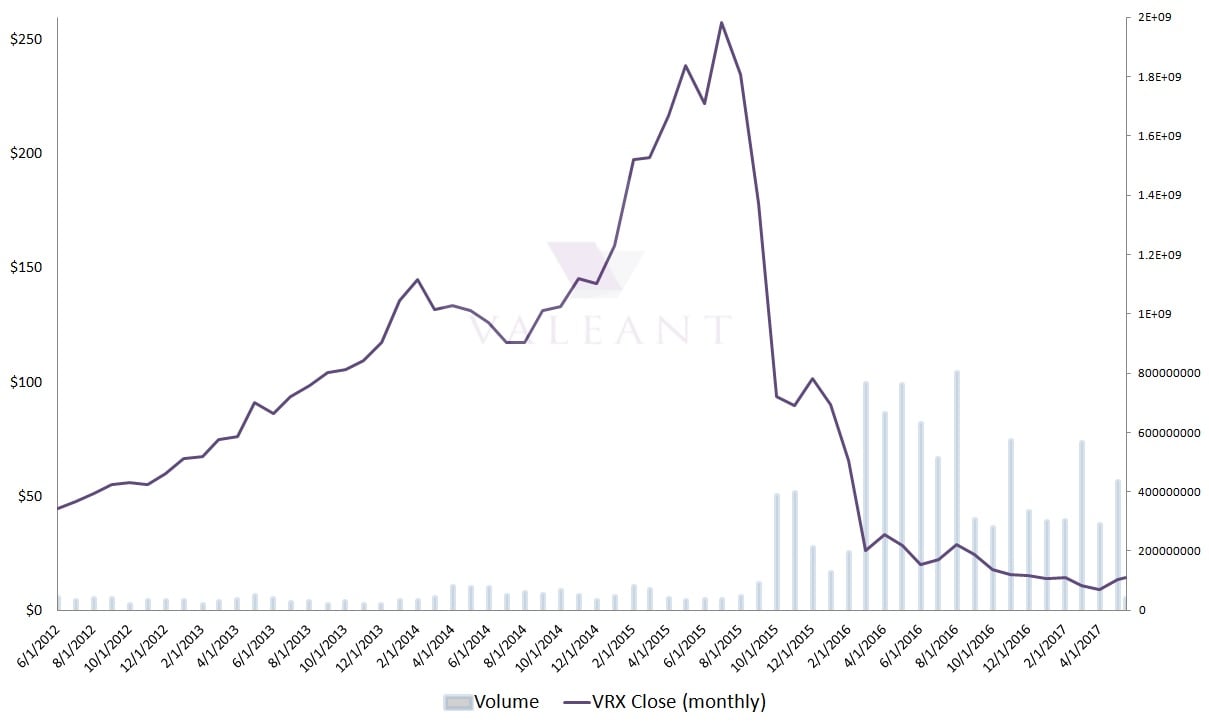

Click to Enlarge

After all, Valeant shares were trading hands at above $200 two years ago. That’s nearly a 1,500% move higher from the present market price.

But a bottom could have happened in June of 2016. Back then, VRX shares also jumped significantly higher from the half-year mark. Of course, the markets had different plans, and here we are. This could be the bottom, or it could be a respite before another shipwreck.

I just don’t know what to make of VRX stock. One thing that I do know is that their numbers are ugly. In the bigger picture, Valeant is constantly racing from behind the pack. Their resilience is noble, but nobility is not the same as profitability.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.