Schizophrenia is as much a problem in human societies as it is in the markets. Just take a look at Groupon Inc (NASDAQ:GRPN). One of the biggest problems facing Groupon, and by logical extension, GRPN stock, is user integration. Quite simply, the company and its brand name has lost popular-culture awareness.

Despite this issue, GRPN performed brilliantly in the markets for the year-to-date.

Up 14%, Groupon is so far proving the doubters wrong. The majority of these gains were sparked in June, in which GRPN stock rallied to almost 27%. Otherwise, we would be having a completely different conversation. Without the surge, shares faced the prospects of being down double-digits. Consider the June swing as a much-needed reprieve.

More importantly, the sudden rise in GRPN may have fundamental support. According to InvestorPlace writer William White, “B. Riley analysts upgraded GRPN stock from a ‘Neutral’ rating to a ‘Buy’ rating. The reason for the upgrade was Groupon Inc’s increasing profitability and customer growth. The firm is also expecting the company to increase marketing due to these factors.”

One of the biggest contributors towards trending optimism in GRPN stock is the company’s international business. In the event of a sale, B. Riley analysts believe it could be worth a $1 per share premium.

This is certainly a tremendous boost for shareholders. However, with Groupon earnings just around the corner, will the sentiment be enough to attract other buyers?

Can GRPN Keep Momentum Alive?

For the second quarter of fiscal 2017, analysts expect the Groupon earnings per share target to break even

at $0. The estimate is smack in the middle of the spectrum, which ranges from two pennies down to two pennies up. The coin-toss nature of the earnings target isn’t at all surprising. Over the past several months, a majority of covering analysts ranked GRPN stock as a hold.

Although the $0 earnings estimate seems rather uninspiring, it is a significant step up from the year-ago Q2 estimate. Back then, analysts expected Groupon earnings to fall in the red by 2 cents. However, the company surprised the markets by paring losses at 1 cent down.

This year represents an important turning point for GRPN. Analyst estimates progressively move higher from Q1. In sharp contrast, consensus forecasts called for negative Groupon earnings in the first three quarters of 2016. Thus, the markets are eagerly anticipating a solid beat for Q2. Anything less would be disappointing, given recent momentum.

On the revenue front, Wall Street is looking for $688.8 million. This forecast is towards the lower end of the sales spectrum, which ranges from $650.7 million to $695.7 million. Softness in revenue expectations is again not surprising. Groupon is demonstrating cyclical patterns. Outside of the fourth quarter, GRPN hits a challenging retail environment.

The company’s in-sector performance is another problem. Compared to internet-related businesses, Groupon’s three-year sales growth is middling. Furthermore, over the last six quarters, year-over-year revenue growth averages a decline of 0.21%.

For Groupon earnings to be successful, the company must rely on all cylinders firing and continuance of their cost-cutting measures.

Groupon Needs More Than Great Earnings

Based on its momentum, and improving financial outlook, GRPN stock has a solid chance of delivering the goods. Unfortunately, I don’t think it’s enough.

A good clue can be found in the markets. After securing a robust month in June, GRPN stock failed to add more to its gains. That failure is all the more notable considering that the B. Riley boost came at the end of June. More critically, shares have charted a bearish head-and-shoulders pattern, largely underneath its 200-day moving average.

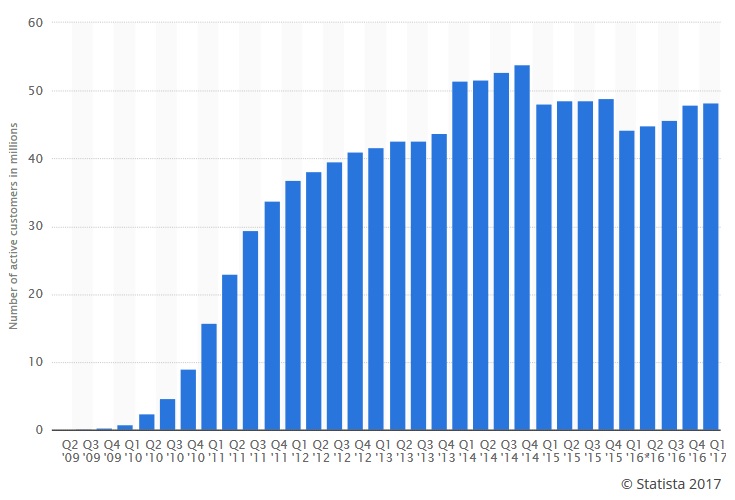

Active customer statistics brings us the second warning.

Click to Enlarge

As of this year’s Q1, Groupon had 48.3 million unique customers. That number has virtually not grown since Q1 2015. It’s also down more than 10% from the firm’s all-time peak of 53.9 million customers, set in Q4 2014.

The biggest concern? The number of customers in Q4 has been declining over the past two-and-a-half years. Since GRPN experiences the most activity during the holidays, the Q4 trend is a major red flag.

Finally, you have to recognize GRPN stock for what it is. Shares spent all of 2016 attempting to regain its prior glory, but to no avail. Without a significant catalyst, I don’t see it doing anything other than wildly swinging north and south. Even a great Groupon earnings report isn’t enough to change this dynamic.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.