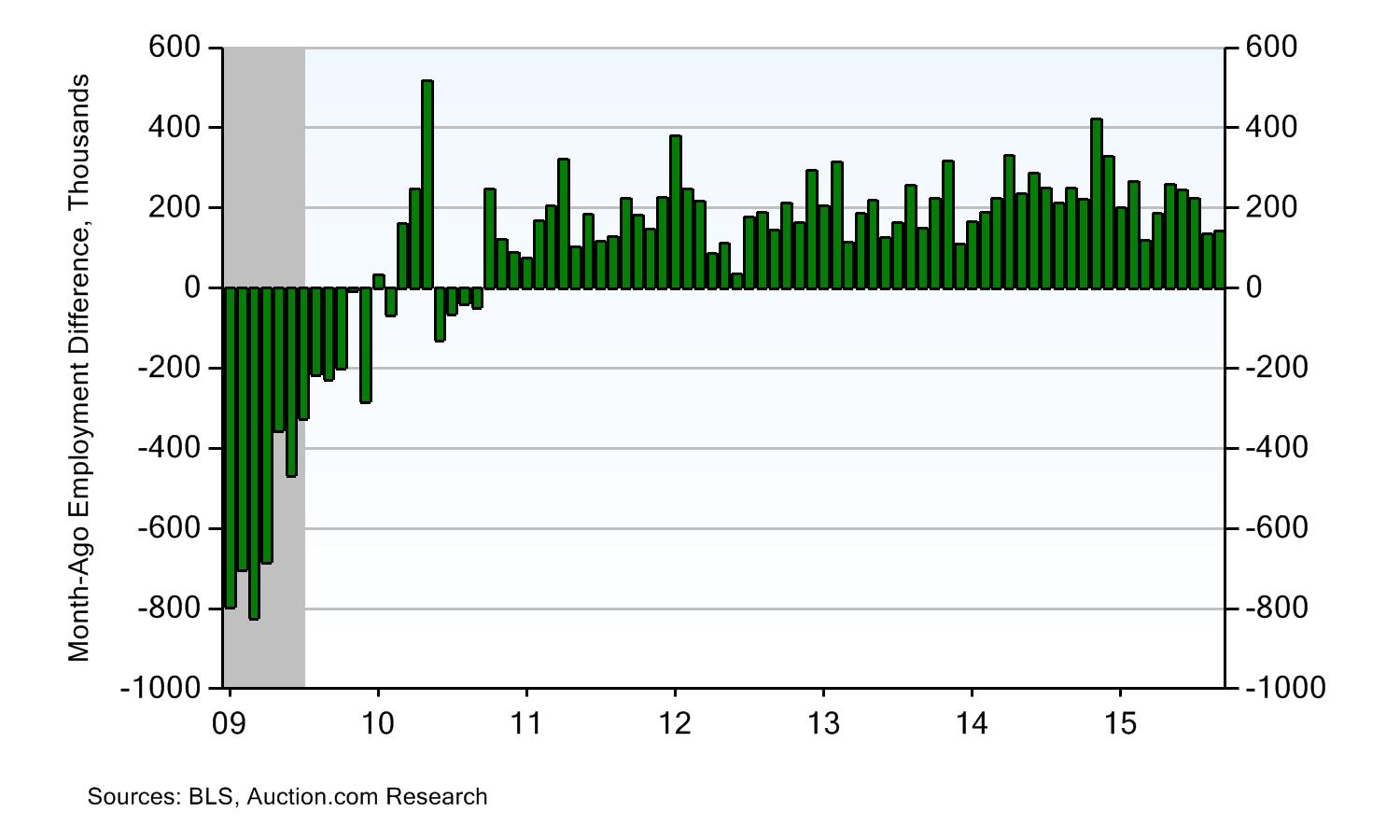

The BLS released September employment data last week, and the result was discouraging with respect to expectations. September saw 142,000 jobs added in the month compared to expectations for 203,000. Unemployment remained flat at 5.1% as expected, while the labor force participation rate eroded 20 bps to 62.4%.

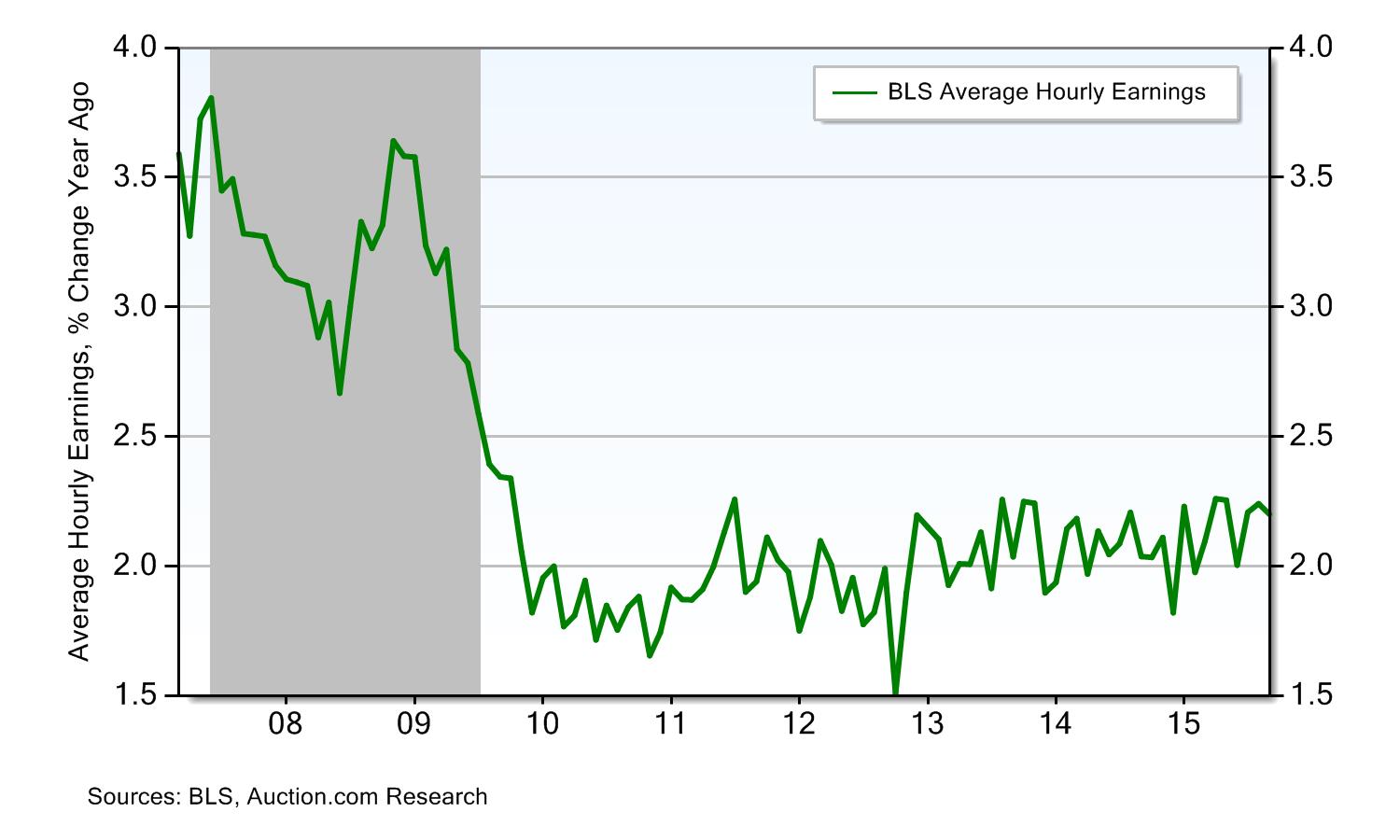

The average hourly earnings series were also disappointing in this report, still lagging the ECI and Atlanta Fed Wage Gauge, though these indicators have started to slow as well.

After recent market volatility gave the Fed pause on a September rate hike, we now believe the past two months’ employment weakness will dissuade the Fed from raising rates this year, barring an incredible jump next month.

September Job Growth Disappointed, While Prior Two Months Suffered Downward Revisions

September saw just 142,000 jobs added in the month compared to expectations for 203,000. August’s gain was revised downward from 173,000 to 136,000, while July’s gain was also revised down from 245,000 new jobs to 223,000. That leaves the average monthly gain this year at 198,000, not cause for panic but well shy of the 260,000 average monthly gain in 2014.

The poor headline figure was reflected in the Auction.com Research Acceleration Index, which fell from -19.7 last month to -34.9 this month (scale -100 to 100) as it continues to deteriorate.

The BLS’ Wage Growth Figure Rises Marginally, Less Encouraging Than Other Wage Growth Measures

Average hourly earnings were flat from the month prior, missing expectations for 0.2% growth. Year-over-year earnings growth remained stable at 2.2%, and have disappointingly failed to show any sort of acceleration in recent months. The continued tightening of the labor market still has us favoring the stronger ECI and Atlanta Fed measures, but even the Atlanta Fed wage tracker has cooled in recent months. Wage growth will be key to the next stage of economic expansion, so we continue to await more growth in these indicators.

Energy Sector Contraction Is Intensifying, with No End in Sight

Losses in the energy patch continue to intensify, as job cuts are mounting. Support activities for mining, mining, and oil and gas extraction were all among the worst-performing sectors, declining 5.4%, 2.1%, and 1.1% respectively over the last three months.

The Texas metros, in particular Houston, are reflecting this slowdown, as office vacancies rise amid slowing absorption and a robust supply pipeline. Fort Worth’s economy is also sputtering, though its recent stagnancy has yet to materialize in real estate fundamentals.

Oil prices meanwhile have shown no meaningful recovery, large oil companies continue to announce layoffs, and credit markets show high risks of default on smaller names. The October reserve recalculations by banks could contribute to more dire financial situations in the sector.

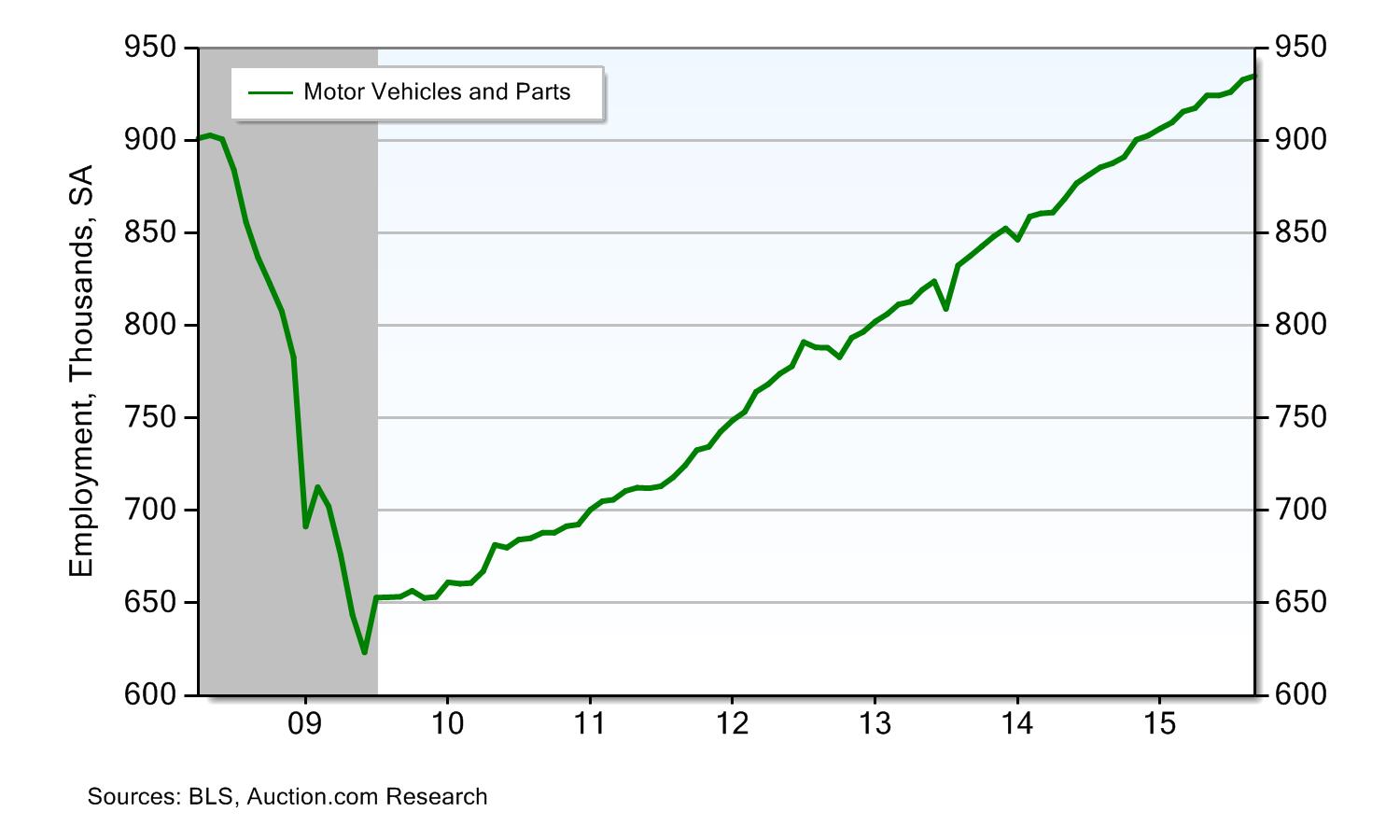

The Auto Sector Is Revved Up, but Subprime Auto Lending Is a Growing Concern

The auto sector is still strong, as automobile dealers and motor vehicles and parts each saw strong gains of 1.1% over the past three months, while motor vehicle & parts dealers saw a solid 0.7% gain. This is expected as auto sales remain hot, but there are still concerns about the growth of subprime auto-lending contributing to these sales.

For now, however, the sector continues to be a tailwind for metros with exposure such as Detroit, parts of the Midwest, South Carolina and other pockets in the South.

Residential Construction Employment Is Heating Up, Other Facets of Construction Diverging

The construction sector is showing bifurcation, as residential construction grew 1% over the past three months, while non-residential construction and civil engineering saw losses of 0.5% and 0.2% respectively. Multifamily construction activity continues to see pocketed growth across the country in select metros such as Austin, New York City, Boston and Nashville, and this will provide a tailwind for these metros as household formations continue to rise.

The continued recovery of housing market will be reliant on further wage growth, though millennials burdened by student loans will be a drag on the first-time buyer segment.

This post originally appeared on Auction.com.