For all the criticisms of President Trump, you can’t deny that the commander-in-chief isn’t trying. In his first 12 days in office, Trump signed 18 executive actions — one less than the preceding Obama administration. In particular, he is making good on his campaign promises of lower regulations, a gesture well-appreciated by business leaders. And it’s no surprise that “brick-and-mortar” retail stocks are in great need of a helping hand.

The most obvious culprit is the broader decline in consumer foot-traffic. With e-commerce grabbing an increasingly larger share of total retail sales, many physical stores are steadily becoming irrelevant.

That substantially pressures retail stocks, even big-box retail companies who were once kings of the sector. Unless something drastic occurs, they too face the real possibility of a painful phase out.

This is where President Trump comes in. Despite the litany of controversies emanating from the White House, this administration is unabashedly pro-business. To back up the rhetoric, the last February jobs report exceeded economists’ expectations by a comfortable margin of 17.5%. As a result, the unemployment rate remains at multi-year lows at 4.7%. It’s far too early to call President Trump a success on the economy, but it’s an encouraging start.

That’s the good news. The bad news is that not all retail stocks are going to enjoy the benefits of a Trump administration. Foot traffic is still down, as evidenced by some abysmal performances in the sector. Shoppers are, therefore, incredibly picky in where they buy stuff.

Unfortunately, big-box retail stocks are truly in a make-it-or-break-it scenario. With their vast square footage of real estate, big-box retail companies must drive foot traffic. Not doing so is tantamount to a death sentence.

As with any other sector, big-box retail stocks are divided between the “haves” and “have-nots.” Here are two names to buy, and two to avoid.

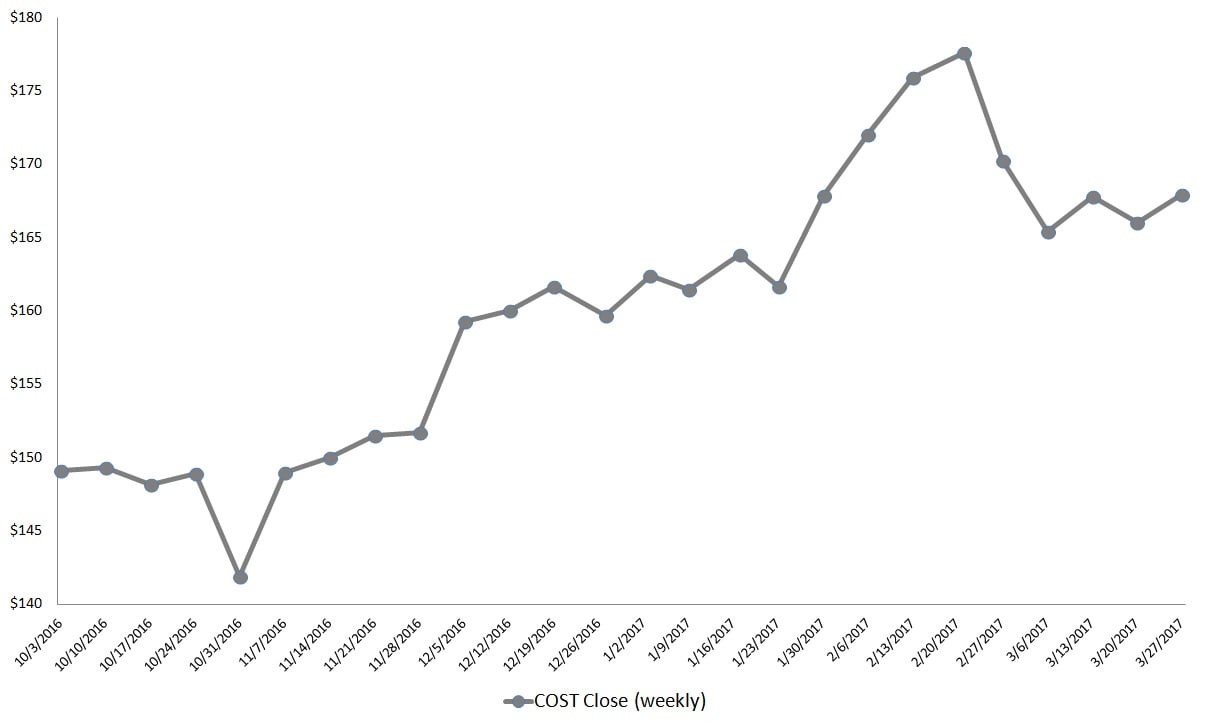

Big-Box Retail Stocks to Buy: Costco Wholesale Corporation (COST)

Click to Enlarge

Despite broader challenges in retail stocks, people still want discounts on common household goods. And against the competition, no one has yet to offer a serious alternative to COST stock.

Costco is essentially an American icon. It is parodied numerous times, perhaps most notably in the films Employee of the Month and Fun with Dick and Jane. Since opening its first store in 1983, the company has amassed 81 million members. That’s a quarter of the total U.S. population. That sheer leverage alone is enough to make a bullish case for COST stock.

More importantly, the fundamental tailwinds for COST stock is reflected in the markets. Year-to-date, Costco shares are up nearly 5%. While that may not sound like much, COST stock was once up 11% not too long ago. Furthermore, the big-box retail giant is handily beating out most retail stocks.

To be frank, this is not the most stable of sectors. Still, a winner is a winner, and that’s exactly what COST stock is.

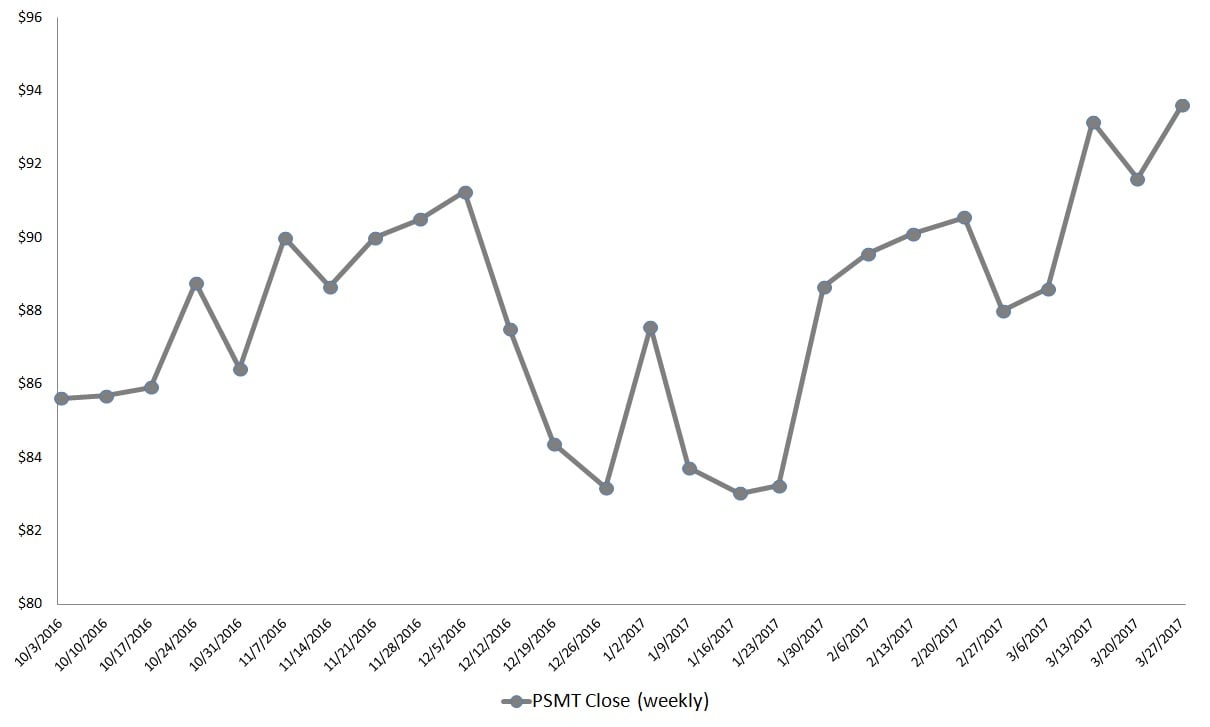

Big-Box Retail Stocks to Buy: PriceSmart, Inc. (PSMT)

Click to Enlarge

Headquartered in San Diego, California, PriceSmart, Inc.’s (NASDAQ:PSMT) practical connection to the U.S. virtually ends there. With 39 warehouse clubs across 12 countries, only one of the warehouses is located on a U.S. territory.

Most PSMT stores operate in Central America and the Caribbean, although they are currently making inroads into South America. This exclusively international focus makes PSMT unique among American big-box retail stocks.

When you think about it, it’s an ingenious move on the part of PriceSmart’s management team. Rather than fighting a losing battle against Costco, PSMT sought greener pastures south of the border. After all, despite differences in nationality and politics, everyone wants a discount! And PSMT continues to grow year after year by delivering the Costco experience to a hungry and appreciative market.

However, PSMT is not just a clone of its bigger brother. Management understands their target demographic, and have adjusted their business model accordingly. Because of their attention to detail, PSMT is successful in the markets despite a tough environment for big-box retail stocks. On a YTD basis, shares are up 12%, and seem poised to move higher.

If you can’t beat them, move somewhere else. That’s what PSMT did, and they’re reaping the rewards!

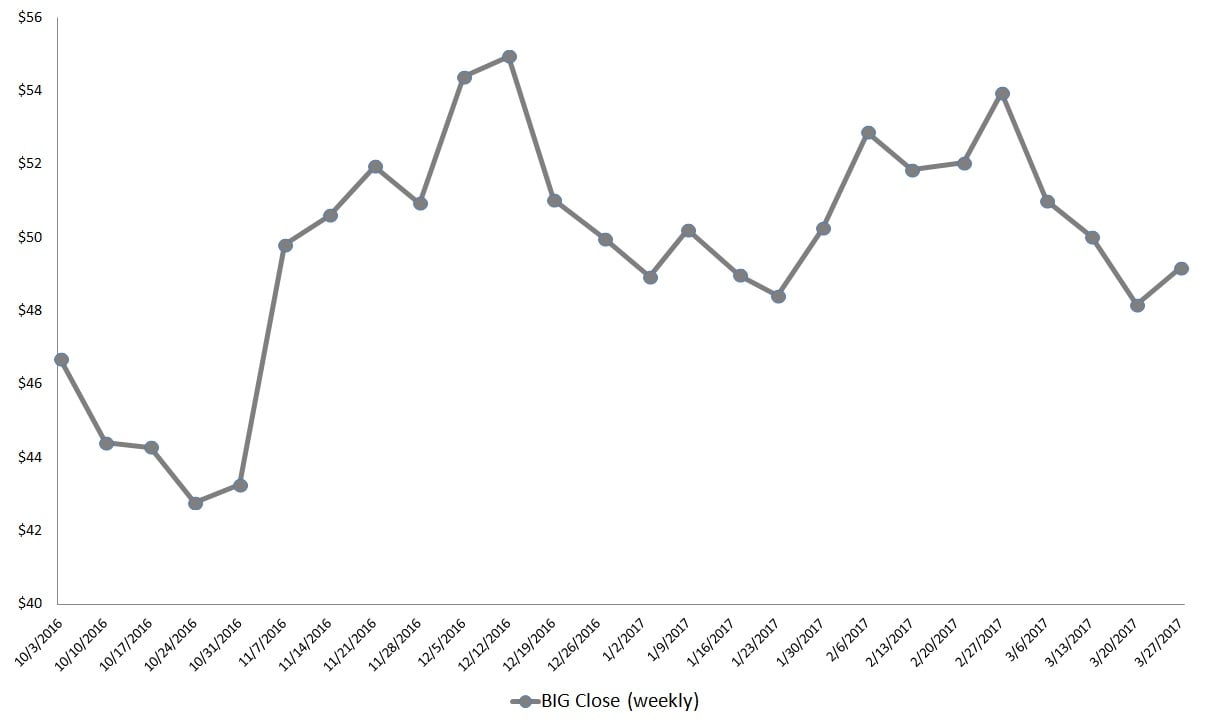

Big-Box Retail Stocks to Sell: Big Lots, Inc. (BIG)

Click to Enlarge

Running through the aisles with oversized shopping carts, it’s easy to get carried away — I know from personal experience! But a variant of this question is particularly suitable for retail stocks like Big Lots, Inc. (NYSE:BIG).

We Americans love big everything, and BIG stock plays into that emotion in more than one way. However, even Americans have a limit on their over-sizing craze. For Big Lots, how many big-box retail stores do we need? Apparently, the answer is not any more. If we look at revenue growth for BIG stock over the past ten years, it averages a pedestrian 1.3%. In contrast, Costco averages 7.2%.

You hate to say it, but BIG is getting outplayed by the competition. On a YTD basis, shares are down 2%. That’s not a horrifically bad performance when compared to other retail stocks. However, BIG stock shows a negatively tilted trend channel. Unless it somehow improves its financials, I don’t see why investors want to stick around.

The bottom line for BIG stock is that there are plenty of other opportunities that have a better risk-reward picture.

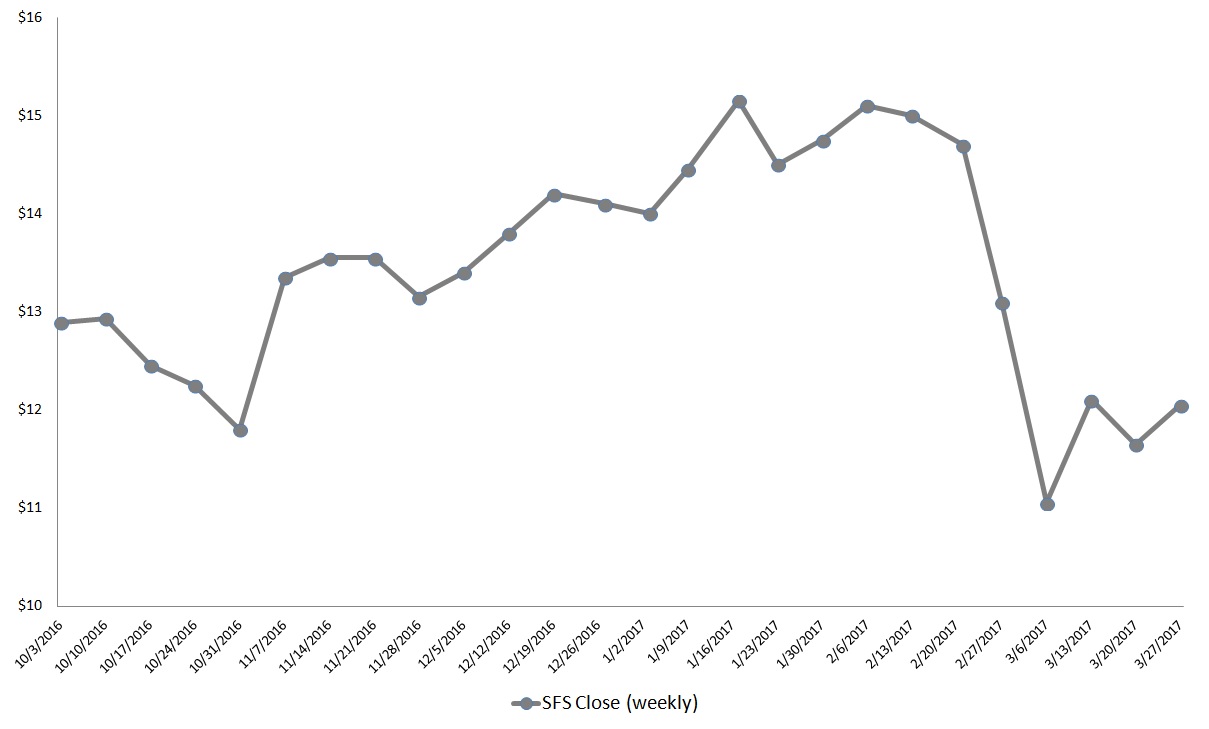

Big-Box Retail Stocks to Sell: Smart & Final Stores Inc (SFS)

Click to Enlarge

Currently, SFS stock has a market capitalization of only $903 million, or only 40% of Big Lots’ figure. With so much competition in the big-box retail sector, SFS faces a war of attrition.

Sadly, it’s the least capable of waging such a war.

The problem for SFS is finding ways to compensate for its lack of size. However, Smart & Final’s financials are middling at best. Nothing strikes you as being particularly confidence-inspiring, and as you dig deeper, the more anxious you become.

For instance, the debt burden for SFS will come back to bite it if it can’t claw back some market share. Also, SFS stock is considered overvalued on earnings against other big-box retail stocks.

It’s no wonder Smart & Final is such a laggard in the markets! SFS has lost 14.5% of capital value this year, and 2017 is still very much young. Speculative bulls are attempting to stage a recovery, but the corresponding volume is weak. You don’t have to be a renowned technical analyst to understand that that spells trouble.

I give credit for SFS sticking it out, but for investors, it’s just not a smart play.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.