I’ll be the first to say that I really love the products from Tesla Inc (NASDAQ:TSLA). The new semi truck? Awesome. The Roadster? Jaw-dropping. Even the company’s foray into electric power and energy storage is amazing. Yet, despite all the company has going for it, the TSLA stock price is teetering on the brink of trouble.

From a fundamental perspective, there are surely concerns. Tesla CEO Elon Musk, as great of an inventor as he is, continually has trouble hitting his lofty targets. Even though TSLA stock is showing some cracks, Wall Street has largely been willing to look past these shortcomings — be it Model X production in the past or Model 3 production now.

If Tesla had a lower valuation, the risk of these shortcomings would be smaller. But because TSLA stock trades at ridiculous levels, it has to execute. To some extent, though, I get it. If Musk says they’re going to produce 50,000 units, the excitement isn’t there, even if they beat it. If he says they’re going to produce 500,000 units, Wall Street gets all giddy.

Enough About Expectations, We Want Results

While the $200,000 Roadster and semi truck are all great, what about the now? Essentially, Tesla used the Model S and Model X to drive sales, awareness and build the blueprint for the Model 3. That’s supposed to be the money-maker — and it’s why so much hinges on its success. The mass-market sedan starts at $35,000, a reasonable price for a high performance electric car, particularly when compared to the other electric vehicles on the market from General Motors Company (NYSE:GM), Nissan Motor Co Ltd (ADR) (OTCMKTS:NSANY) or

BMW (OTCMKTS:BMWYY).

On the surface, this is an excellent strategy, but the cash burn is a big concern. It’s expensive to ramp production of a mass-market vehicle and capital expenditures were sure to climb. But the margins and sales of the Model 3 need to gain some traction to alleviate investor concerns.

Free cash flow came in at negative $1.55 billion last quarter — gulp — and stands at a about negative $5 billion over the trailing twelve months. Concerns over the financial situation only worsen alongside negative headlines about high vehicle defect rates, employee dissatisfaction and product capabilities. This is in addition to the production concerns around the Model 3.

What Does It Mean for Tesla?

I wouldn’t necessarily believe all the negatively, nor would I blindly follow all the hype. I believe that Tesla will ultimately hit its production targets (although not on time) and will (eventually) successfully roll out its Model 3 en masse. It will remain a player in the auto market and I wouldn’t worry that it will go bankrupt. The product and brand are too strong.

I’ve always been a believer in buying Tesla on large corrections. Should the current concerns creep on investors’ minds and the overall market go through just a touch of volatility, the TSLA stock price could really take a hit.

Not surprisingly, Tesla bonds are in junk territory. While the automaker does have $3.53 billion in cash on hand, total debt stands at $10 billion — roughly one-fifth its $51 billion market cap. The problem with production hiccups (which were bound to happen in any mass-production ramp) is that the cash isn’t coming in. So while Tesla is spending, spending, spending, it’s not able to replenish the cupboards. That could lead to a capital raise sometime in the next six months.

The short-term will have issues. That’s why one must believe in Tesla’s products and Musk’s long-term outlook to be a buyer of the stock.

So, when do we do that?

Trading TSLA Stock Price

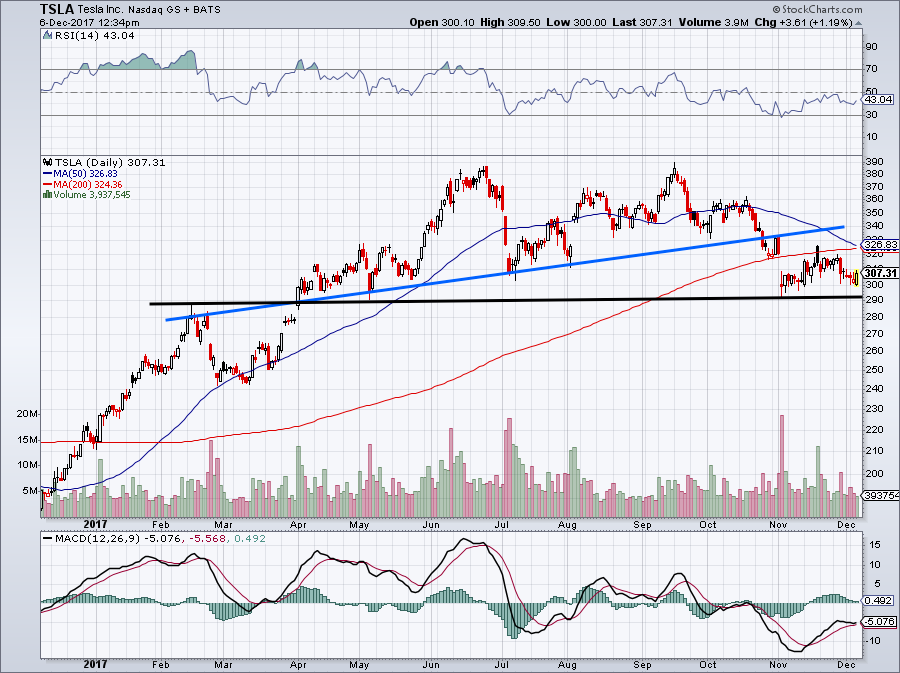

Click to Enlarge

The charts aren’t looking too good, unfortunately. Heading into the semi truck event, we said if TSLA stock price can reclaim $330, it’s a buy, with a close below that level serving as a stop-loss. It wasn’t able to get there and, thus, has floundering back near $300.

Uptrend support (blue line on the chart) couldn’t hold and now looks to be acting as resistance. Horizontal support (black line) is still holding up near $290, but the more times it’s tested, the more likely it is to fail. The 50-day moving average crossing the 200-day to the downside creates what’s known as a “death cross” and doesn’t bode well for TSLA stock price.

Should TSLA stock fail to hold support, I would target between $240 and $270, based on prior consolidation levels in the stock. If TSLA stock climbs above $325-$330, I’ll consider it a breakout buy. Until then, it’s a no-touch, unless investors want to gamble on $290 holding as support.

I personally, do not.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.