By all accounts, the shares of Micron Technology (NASDAQ:MU) should be trading somewhere around $84. That’s the consensus price target which analysts have come up with. Given that MU stock is only trading at a forward price-earnings ratio of 4.4, the argument that the shares could be worth three times their current value of $51.37 holds water.

What gives? In other words, why has MU stock been so cheap for so long? Why are the shares, which have failed to reach the consensus target, starting to move further away from it?

You may not like the answer, but it’s the answer all the same. This is one of those cases where it’s crystal clear that presumptions and perceptions are in the driver’s seat. Whether they are right or wrong, you have to decide if you want to jump in the car and go along for the ride.

Don’t Fight the Tape

Just for the record: Micron has vexed the pros, too.

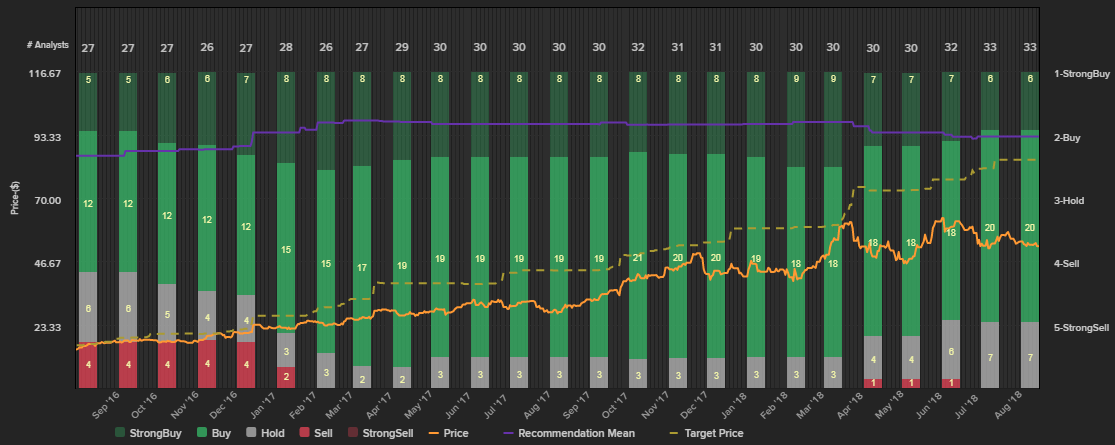

The graphic below tells the tale. Take note of the fact that the price of MU stock (the solid yellow line) has never really met the ever-changing consensus target (the yellow dashed line). However, that’s not terribly unusual; analysts usually raise the average price target before a stock reaches it. What’s unusual here is that the gap between the consensus price target and the actual price of Micron stock is decidedly widening.

Click to Enlarge

Another curiosity is clearly evident on the chart. If you look closely, as of April, even though the consensus target continued to rise, a couple of analysts lowered their ratings on MU stock from strong buy to just buy, and a couple more downgraded their ratings from buy to hold.

That’s odd, simply because the company’s outlook didn’t change much between the beginning of the year and April.

Some observers will say that the so-called supercycle for computer memory and storage now lies directly ahead but was only on the horizon a few months ago.

That argument is at least slightly flawed. A few months ago, SSD and conventional hard disk drive prices were already falling or had already stabilized at low, commodity-like prices. RAM prices more or less peaked in March

, in line with MU stock. But that still doesn’t explain how and why Micron shares have been priced at a single-digit price-earnings multiple for a year.

The Reality of MU Stock

There is an explanation though. That is, investors have been expecting — and even counting on — the supercycle to end for the better part of the past year. That doubt prevented Micron stock from ever reaching its full potential.

Make no mistake though. Ordinary investors were the ones holding it back. Analysts believed that MU stock was undervalued and still do. In recent months, however, at least some of them have been forced to respect the fact that if the masses irrationally see more risk than reward, then it’s impossible to change their minds. The pros finally started to acquiesce in April, lowering their ratings on Micron even as their average price target increased.

You don’t see something like this very often. Usually, investors eventually acquiesce to analysts’ expectations.

Are investors right or wrong? It’s a good question that’s impossible to answer. The big takeaway, though, is the simple fact that even analysts have their breaking points which force them to abandon their views on the valuation of a stock. In April, Micron’s shares were priced at less than six times their trailing earnings. That’s dirt cheap, even if the memory supercycle is winding down.

The simpler version of the trading lesson: This game doesn’t always make sense.

Bottom Line on MU Stock

As for Micron stock, for the same reason analysts can no longer afford to fight the stubborn bearish crowd, you can’t either.

If it doesn’t feel right, you’re not crazy. It’s not very often that you can buy a solid tech stock at a single-digit price-earnings ratio. Even if RAM and storage prices are poised to hit a headwind, there’s still lots of value packed into MU stock.

Click to Enlarge

The pullback that’s apt to take shape from here is going to drag Micron stock to even lower single-digit price-earnings levels. That would be a bargain-basement price if enough people would see it as such. Too bad they’re choosing not to see it that way.

Welcome to the world of trading.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.