In news that reverberated across financial markets, streaming giant Netflix (NASDAQ:NFLX) is raising its U.S. subscription prices by $2 on its standard plan, marking the largest price hike in the company’s history. In response, Netflix stock rallied more than 6%, continuing what has been a torrid 50%-plus run since Christmas Eve.

Why the big pop in Netflix stock? Won’t price hikes anger existing subscribers, cause churn and scare away new ones from joining?

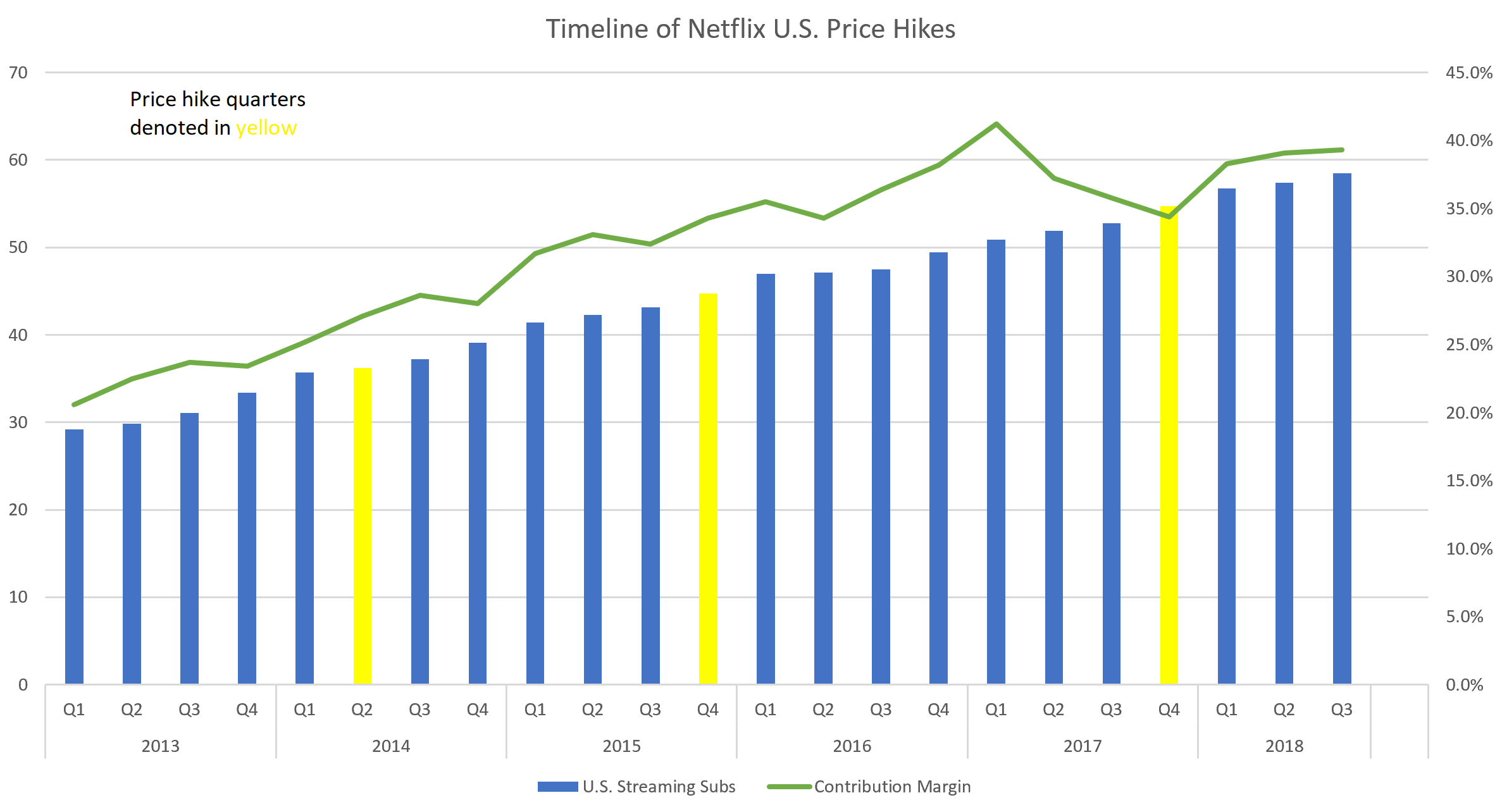

History says no. Netflix has hiked U.S. streaming prices three times before. Each time, the price hike resulted in minimal churn and a minimal affect on user growth. Instead, all the price hike did was push up profit margins.

As such, history says price hikes are a huge win for Netflix stock. They don’t negatively impact user growth, and they simply provide a multi-quarter tailwind for margins.

The same thing will be true with this price hike, and future price hikes until Netflix reaches a price saturation point. At just $13 per month, Netflix isn’t at that price saturation point. Instead, considering HBO is around $15 per month and linear TV packages run north of $50 per month, Netflix is still a ways away from being maxed out on the price front.

As such, this price hike is a huge win for Netflix . Over the next several quarters, all it will do is push margins, profits and NFLX stock higher.

This Netflix Stock Chart Says It All

Netflix has hiked U.S. streaming prices three times before over the past five years. The first hike was in May 2014, when prices on the standard plan went from $8 to $9. In October 2015, Netflix raised the price of its standard plan again from $9 to $10. Two years thereafter, Netflix hiked prices again from $10 to $11.

None of the price hikes negatively impacted subscriber growth, and all of them positively impacted margins.

In the 12 months following the May 2014 price hike, Netflix added 6.1 million domestic subs, versus 6.4 million in the prior twelve month period. Meanwhile, U.S. streaming contribution margins expanded 600 basis points. Following the October 2015 price hike, Netflix added 4.7 million domestic subs, versus 5.6 million in the prior twelve month period. Contribution margins rose 390 basis points.

Click to Enlarge

In the three quarters since the October 2017 price hike, Netflix has added 3.7 million subs, versus 3.9 million in the prior three quarter period. Meanwhile, contribution margins have risen 490 basis points.

Overall, the trend is crystal clear. Netflix hikes prices every one to two years. Those prices hardly impact U.S. subscriber growth trajectory, but they do provide a huge, multi-hundred-basis-point boost to contribution margins.

This hike will be the same. There’s the argument that the January 2019 price hike is $2, versus $1 hikes in each of the three prior price hikes. That’s true. But, the value prop on Netflix has grown immensely over the past twelve months due to its still rapidly growing and only improving original content portfolio. Plus, at $13, Netflix’s cost isn’t anything absurd. HBO is at $15 per month, and Netflix

tied HBO for most Emmy wins this past year.

Thus, this price hike will play out much like prior price hikes. It won’t lead to churn, and it will support further sub growth. Most importantly, it will provide a big boost to margins.

Countdown to $600

Price hikes are just one driver of the long-term NFLX growth narrative. Other drivers include cord cutting, streaming service adoption and original content.

Fortunately for shareholders, all three of those drivers plus price hikes are moving in the right direction for Netflix stock. Everyone’s still cutting the cord. Everyone is still going to streaming. And Netflix’s original content is only getting better.

My long-term base-case scenario for Netflix is 350 million subs at $15 per month, with 30% operating margins. Under those assumptions, my long-term target for Netflix’s EPS is $30, and I think 2027 is the year when Netflix will reach that profit target.

Growth stocks normally trade around 20X forward earnings. A 20 forward multiple on $30 in earnings-per-share implies a fiscal 2026 price target of $600. Thus, it is only a matter of time before Netflix stock breaks out to $600, implying healthy upside in a multiyear window.

Having said that, caution is warranted here. Netflix stock is up almost 40% in just over two weeks. That’s a huge rally. A pullback is warranted. The stock is technically overbought and fundamentally overvalued in the near term (annual return rate from today to $600 by the end of 2026 is just 7%, which isn’t all that great considering the market averages 10% annualized returns).

Bottom Line on NFLX Stock

Price hikes historically provide a huge, multiquarter tailwind for Netflix stock. This price hike should play out no differently. As such, this price hike will keep Netflix stock on a long term winning path, and confirms that $600 within the next several years is attainable.

Having said that, the stock is entering near-term overbought and overvalued territory, so investors should proceed with caution over the next few trading days and weeks. If the stock does pull back — as the laws of financial gravity say it should — then that pullback will be a great buying opportunity.

As of this writing, Luke Lango was long NFLX.