Shares of iRobot (NASDAQ:IRBT) have been on a tear since the company reported a fourth-quarter earnings that impressed just about everyone on Wall Street. Times must be good if U.S. consumers are scooping up robotic vacuums hand over fist, right? Perhaps, but it makes some investors feel that they’ve missed their chance to get long IRBT stock.

Admittedly, it can be hard to buy into iRobot stock after it’s had such a big move, but that may not be the case with IRBT. If the company can maintain momentum, it should have more strong earnings to come. On the chart, technicians surely appreciate the strength brewing in IRBT stock right now, and more could be on the way.

Valuing iRobot Stock

GAAP earnings came in at 88 cents a share, a whopping 38 cents per share (or 76%) ahead of consensus expectations. Revenue of ~$385.7 million topped estimates by just over $3 million or about 1%. This sent shares soaring on the day, although it has met some resistance on these rallies.

For the year, revenue grew about 24% year-over-year (YoY) topping $1 billion, while earnings soared almost 75%. In fiscal 2019, analysts expect iRobot to grow sales 14.4% to $1.25 billion. Their models call for earnings of $2.88 per share. After IRBT crushed Q4 expectations, where analysts expected 7% growth from fiscal 2018 to 2019, the $2.88 per share estimate for 2019 would actually represent a YoY decline.

However, guidance came in stronger than expected. Management is looking for revenue of $1.28 billion to $1.31 billion, representing growth of 17% to 20%. iRobot also expects to earn somewhere in the range of $3.00 per share to $3.25 per share, a growth range of -2.2% to about 6%.

Admittedly, it’d be more encouraging for IRBT stock to see stronger earnings improvements. But given how much the company beat Q4 estimates by — again, by almost 75%! — it’s hard to be too disappointed. Still, some investors feel that this could a “best it will get” situation. This is even more true with shares trading at roughly 33x 2018 earnings.

However, bulls are encouraged by guidance. Management is forecasting

roughly 10% operating margins (stable profitability vs. current levels despite a slight dip in 2019) and mid- to high-teens revenue growth in 2020. Valuation-wise, IRBT stock could be cheaper, but fundamentally speaking it’s doing pretty well overall. It helps that iRobot doesn’t carry any debt.

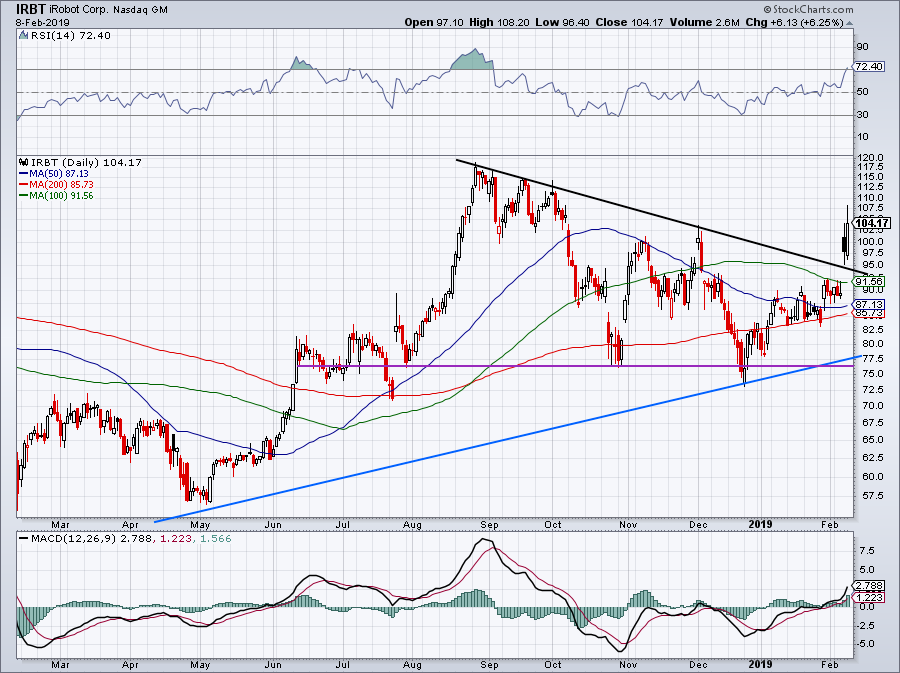

Trading IRBT Stock

Click to Enlarge

One interesting note on IRBT stock is its high short-interest. With more than 31% of the shares sold short — although it’s possible that number shrank post-earnings — iRobot stock could gain some serious upside momentum if bulls start to squeeze the bears.

Shares broke out over downtrend resistance (black line), but didn’t close at the highs. After staggering on Friday, iRobot stock eventually found its footing. Still, this gave bulls an opportunity to get long both days. Further, it gave bears an opportunity to drive IRBT back below resistance, which they failed to do.

I am looking for IRBT to push back up to its prior highs near $117.50. If it can take out that mark, it could really fuel a short-squeeze. On the downside, I don’t want to be long IRBT stock below prior downtrend resistance. More conservative bulls can consider using a stop-loss based on the Thursday-Friday two-day range low.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.