Shares of Tesla (NASDAQ:TSLA) fell sharply in early April after the electric vehicle manufacturer reported first-quarter delivery numbers that widely missed consensus expectations, and represented a huge drop from the prior quarter. Specifically, Tesla delivered just 63,000 vehicles in the first quarter of 2019, falling nearly 20% short of sell-side expectations (76,000 deliveries) and down over 30% from the fourth quarter (90,700 deliveries).

Tesla stock dropped nearly 10% response. It currently trades at the low end of its 52-week trading range.

Many bears see the ugly first-quarter delivery update as confirmation of the short TSLA thesis. Their argument is pretty simple. Older Tesla vehicles (the Model S and X) aren’t selling well, and are actually on the decline. Newer Tesla vehicles (Model 3) are losing steam, and may be peaking. With older vehicles on the decline and newer vehicles peaking, Tesla’s whole growth narrative appears ready to tumble. Consequently, TSLA stock appears ready to tumble, too.

But, even after considering the ugly first-quarter delivery report, I don’t buy that bear thesis. Instead, I remain bullish on Tesla stock for one reason: the long-term trend still looks good.

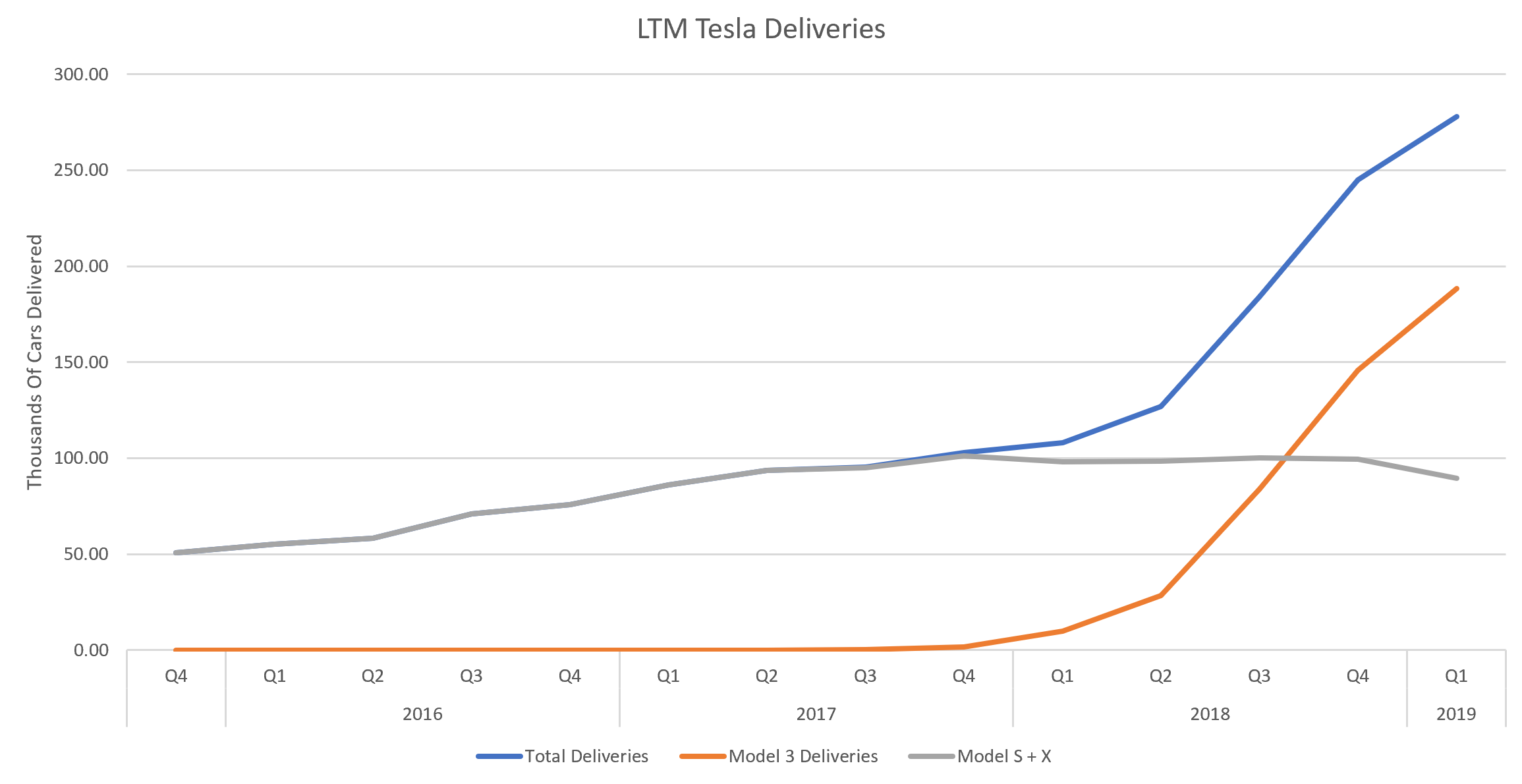

Specifically, over a trailing twelve-month window, Tesla is delivering more vehicles than ever before. That trailing twelve-month delivery volume trend-line has been trending higher for the past several years, and will continue to do so over the next several years, too, thanks to global expansion, new vehicle launches, and broader EV adoption.

As such, the long-term TSLA bull thesis remains intact. This company continues to grow its share in the rapidly expanding global EV market, and that growth trajectory puts Tesla stock in a position to head materially higher in the long run.

The Number Wasn’t That Bad

Although the headline Q1 delivery miss was wide, the number itself wasn’t that bad when you consider the context and all the details.

Tesla delivered 63,000 vehicles in the quarter. That’s far below the 76,000 analysts had expected, and even further below the 90,700 vehicles, Tesla delivered in the previous quarter. Yet, due to logistics-related challenges, there were more than 10,000 vehicles in transit at the end of Q1. Thus, adjusted first-quarter delivery volumes were closer to 75,000, which is just a hair shy of the 76,000 number analysts were looking for.

Further, the all-important Model 3 deliveries in the quarter were 50,900. That is barely shy of the analyst consensus estimate of 52,450 deliveries. Of the 10,000-plus vehicles in transit at the end of the quarter, easily north of 5,000 of them were Model 3 vehicles. Thus, the adjusted first-quarter Model 3 delivery volumes were north of 55,000, and that’s above what analysts were looking for.

Zooming out, then, Tesla’s adjusted delivery volumes were actually pretty good in the quarter, and above-consensus for the Model 3. That’s pretty impressive, especially considering the context of the quarter. The global economy slowed. Auto demand globally cooled off. Pretty much every other auto company has reported awful numbers in early 2019. Tesla announced a lower-priced Model 3 and a new Model Y vehicle, so demand likely flipped to those two new vehicles at the expense of existing vehicle demand.

Broadly speaking, then, Tesla’s Q1 delivery report wasn’t that bad, after adjusting the numbers for vehicles in transit and considering the context of the quarter.

The Long-Term Trend Remains Healthy

In the big picture, a weak Q1 delivery report doesn’t do much to alter the long-term growth trajectory for this company.

Specifically, over the past twelve months, Tesla has delivered nearly 280,000 vehicles globally, and that’s up 14% sequentially from last quarter’s trailing twelve-month vehicle delivery total. Indeed, this trend-line of trailing twelve-month delivery total has been in ramp mode for the past several years. It remains so today, even amid what everyone is calling an awful Q1 delivery report.

Click to Enlarge

Thus, the long-term uptrend in Tesla vehicle delivery volume remains in-tact. Assuming this trend-line continues on a 10% growth path for the rest of the year (which seems likely, given new vehicle launches), then Tesla is on track to deliver 370,000 vehicles this year. That’s largely why I’m not shocked that Tesla maintained its full-year delivery guide of 360,000 to 400,000 vehicles. Current trends imply that a 360,000-plus delivery volume level is achievable and likely this year.

At 370,000 deliveries, Tesla would control roughly 11% of the global EV market in 2019, based on year-to-date trends. That is roughly in-line with last year’s 12% market share, and up from the sub-10% market share the company had in 2016 and 2017. Thus, despite rising competition, Tesla is on track to maintain double-digit market share in the burgeoning global EV market.

So long as this remains true, Tesla stock remains on track to hit a $200 billion-plus valuation at scale.

Bottom Line on TSLA Stock

Tesla stock is reeling after a wide Q1 delivery miss, but as a long-term bull, I’m not too concerned. The Q1 delivery number, after adjusting for vehicles in transit and considering the context, was actually pretty good. Meanwhile, the long-term uptrend in delivery volume implies that the Tesla story is still ramping, and that the company is holding its leadership position atop the global EV market. So long as that remains true, Tesla stock will stay on a long-term winning trajectory.

As of this writing, Luke Lango was long TSLA.