Over the past several months, the bears have taken control of Tesla (NASDAQ:TSLA) shares amid a flurry of negative catalysts. Broadly, they imply that the company’s growth narrative is losing steam. Tesla stock has consequently fallen off a cliff, dropping from $380 in late 2018 to below $200 today. Indeed, the equity currently trades at its lowest levels since late 2016.

To make matters worse, Wall Street analysts are throwing in the towel. Quite a few analyst firms are throwing out doomsday targets for the TSLA stock price which are spooking investors. For instance, Morgan Stanley recently cut its bear-case forecast to $10, while Citi lowered its per-share expectations to $36.

Currently, the Tesla stock price trades just under $200, and that’s a multi-year low. But does that really justify the idea that shares could fall another 90% or more from here?

In a doomsday scenario, yes. But it is highly unlikely to happen. Instead, given current trends, it’s much more likely that TSLA stock stages a meaningful turnaround over the next few months.

How Tesla Stock Could Fall Below $50

There is a viable doomsday scenario wherein Tesla stock does indeed fall below $50 in 2019. That scenario is as follows.

Think out 10 years. The current car market measures around 70 million vehicle sales every year. That market has grown at a steady low-single-digit compounded annual growth rate for a long time. Ride-sharing and car-ownership trends may stall out growth. Over the next decade, the market may not grow at all. If so, the market could measure 70 million cars by 2030.

Electric-vehicle penetration into that market has been steadily rising, and projects to keep doing so. But it may stall out as logistics and price become consumer-pain points, diluting demand. Broadly then, the EV penetration rate may only reach 20% by 2030, implying 14 million EV sales.

Tesla’s current market share of the global EV market exceeds 10% and is rising, thanks to the Model 3 ramp. Worst-case scenario, Tesla loses significant market share as new vehicle ramp slows and more competitors enter the market. Tesla’s market share could fall to 5%, implying only 700,000 vehicles delivered by 2030, representing mild annualized growth from this year’s projected 380,000 vehicle-delivery base.

Average selling prices could fall in the face of competition towards $50,000, as Tesla is forced to discount to sell more cars. Thus, revenues may only round out to around $35 billion in 2030. For the record, analysts project top-line sales to surpass $30 billion next year.

Meanwhile, gross margins may stall out around 20%, while the opex rate may only fall to 15% due to lack of top-line scale. Operating profits, then, would come in around $1.75 billion. Taking out $750 million for interest expense and 20% for taxes, you’re left with around $800 million in net profits. On what will likely be 200 million shares out, that equates to $4 in EPS.

Based on a market average 16-forward multiple, that equates to a 2029 price target of $64. Discounted back by 10% per year, that equates to a 2019 price target of around $25.

Why TSLA Stock Will Rally Back Toward $300

To repeat, we could see Tesla stock drop below $50 in 2019 in a dire circumstance. But it’s highly improbable. Instead, it’s much more likely that it rallies from here.

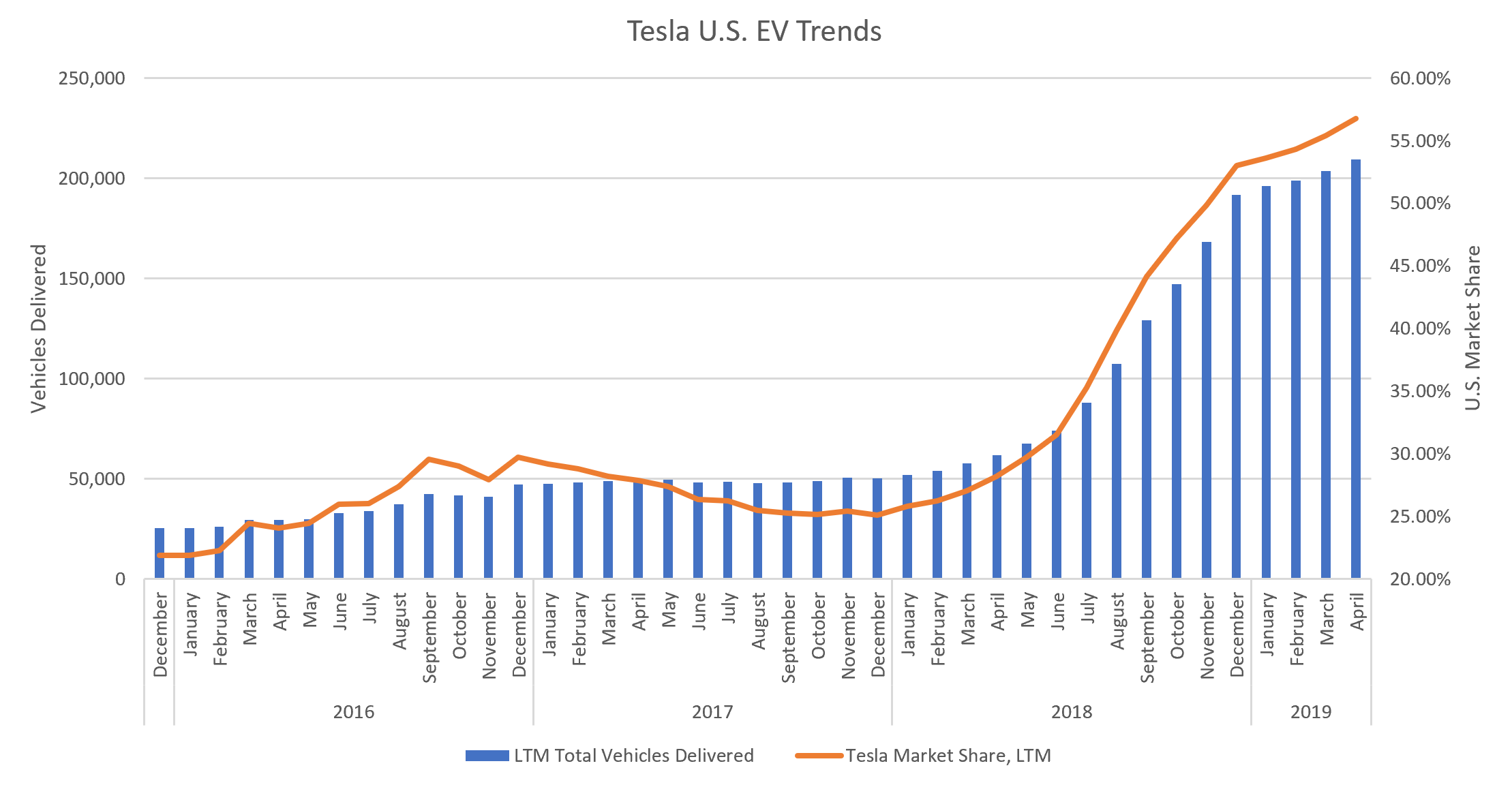

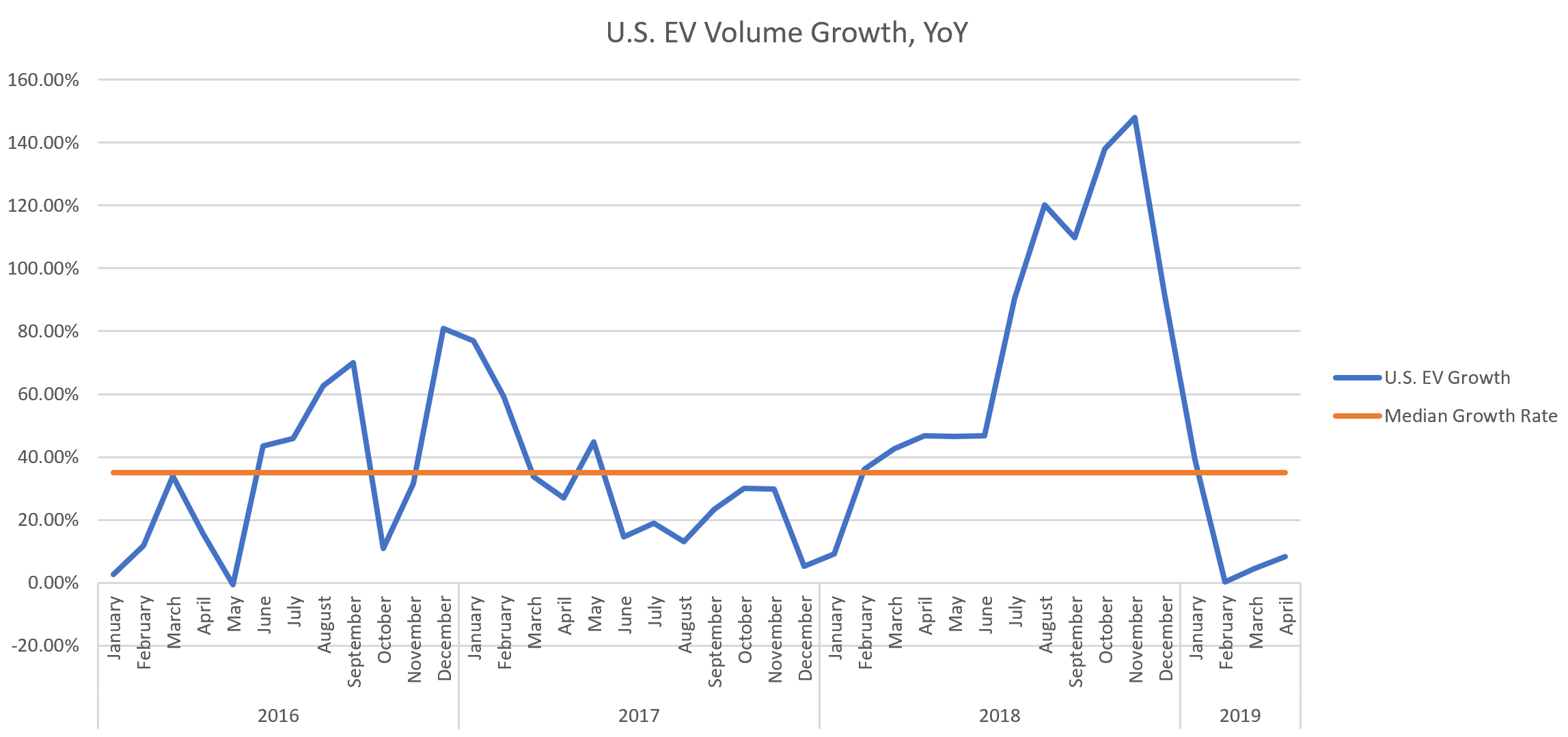

Why? Because most trends remain favorable for Tesla. Sure, demand is waning in the new year, but total vehicle-delivery volume both in the U.S. and globally continues to rise on a trailing-12-month basis. Further, Tesla still has the most popular EVs in the U.S., and the company’s market share similarly continues to head higher. The only problems are that U.S. EV demand is stalling out, and Tesla is having trouble delivering its cars in international markets.

These two problems won’t last. U.S. EV demand surged higher in late 2018. Now, it’s normalizing lower. This is natural. It has happened before; several times, in fact. And every time it does happen, growth eventually picks back up, and the EV industry continues on a secular-growth track.

The same thing will happen this time, mostly because consumer awareness of and demand for EVs remains robust. Moreover, legislation globally continues to promote EV adoption. Thus, EV demand will bounce back, and when it does, Tesla vehicle delivery volume will pick up, too.

Meanwhile, Tesla won’t forever struggle delivering its car in international markets. There was a point in time when Tesla had similar difficulties delivering cars in the U.S. Now, Tesla has three of the top six selling EVs in the U.S., and this has been the case for several quarters. The same dynamic will play out overseas. Tesla will figure out its international logistics issues and eventually turn into the leading player in those markets.

Overall, then, today’s macro and logistics-related headwinds won’t last. Once they pass, all Tesla needs to do is continue stabilizing market share in a rapidly growing global EV market. Later, they can let scale drive operating leverage to produce sizable profits down the road.

By my numbers, the Tesla stock price is actually worth well over $300 today if you consider the big picture. I think that by 2030, TSLA could easily capture 10% of an EV market that will measure around 25 million vehicles, implying 2.5 million deliveries in 2030. I think that will ultimately propel EPS towards $50 by 2030, which again is based on a market average 16-forward multiple and a 10% discount rate.

Combine the metrics together, and they translate to a 2019 price target of over $300.

The Bottom Line

Right now, everyone is focused on the doomsday scenario for TSLA stock, with many analysts suggesting a drop below $50.

But there is a very, very slim chance that doomsday scenario plays out. Instead, given the big-picture fundamentals and long-term growth trends, it is much more likely that Tesla continues to stabilize market share in a rapidly growing EV market. Eventually, this dynamic will help Tesla stock rebound massively from its hugely disappointing 2019 selloff.

As of this writing, Luke Lango was long TSLA.