Canopy Growth (NYSE:CGC) is having growing pains. Canada’s largest cannabis producer posted a $1.28 billion CAN loss (~$960 million) in their fiscal 2020 first quarter. The more disturbing issue for investors in CGC stock was a 4% loss in net revenue from their previous quarter. Analysts were expecting a 17% increase.

Whenever a company misses so badly on earnings, it’s natural for investors to ask what happened. In the case of Canopy, the company clearly misjudged the market for their cannabis oil and softgel products. Was Canopy doing a little bit of channel stuffing? I’ll leave that for others to decide. But it’s clear that Canopy made a miscalculation of the demand for these products.

Another cause for concern is that the company is still looking for a new CEO. After disappointing fourth quarter fiscal 2019 results, Canopy’s board, with a push from big stakeholder Constellation Brands (NYSE:STX), showed CGC founder and former CEO Bruce Linton the door. That vacuum in leadership is more disturbing when investors digest the fact that interim CEO Mark Zekulin is reporting he will leave the company once a suitable replacement is found.

Can Results Match the Optimistic Rhetoric?

Fundamentals matter. Investors are punishing CGC stock and demanding to see at least a path to future profits. On this score, Zekulin is making big promises on his way out the door. In the conference call to report their disappointing earnings, Zekulin reaffirmed that CGC will reach a $1 billion CAN annualized revenue run rate by the end of its current fiscal year. More importantly, Zekulin said the company will deliver a positive adjusted EBITDA on a quarterly basis at some point in their 2021 fiscal year. This would be one step in Canopy ultimately achieving elusive profitability within the next three to five years.

Canopy is Leading a Viable Emerging Market

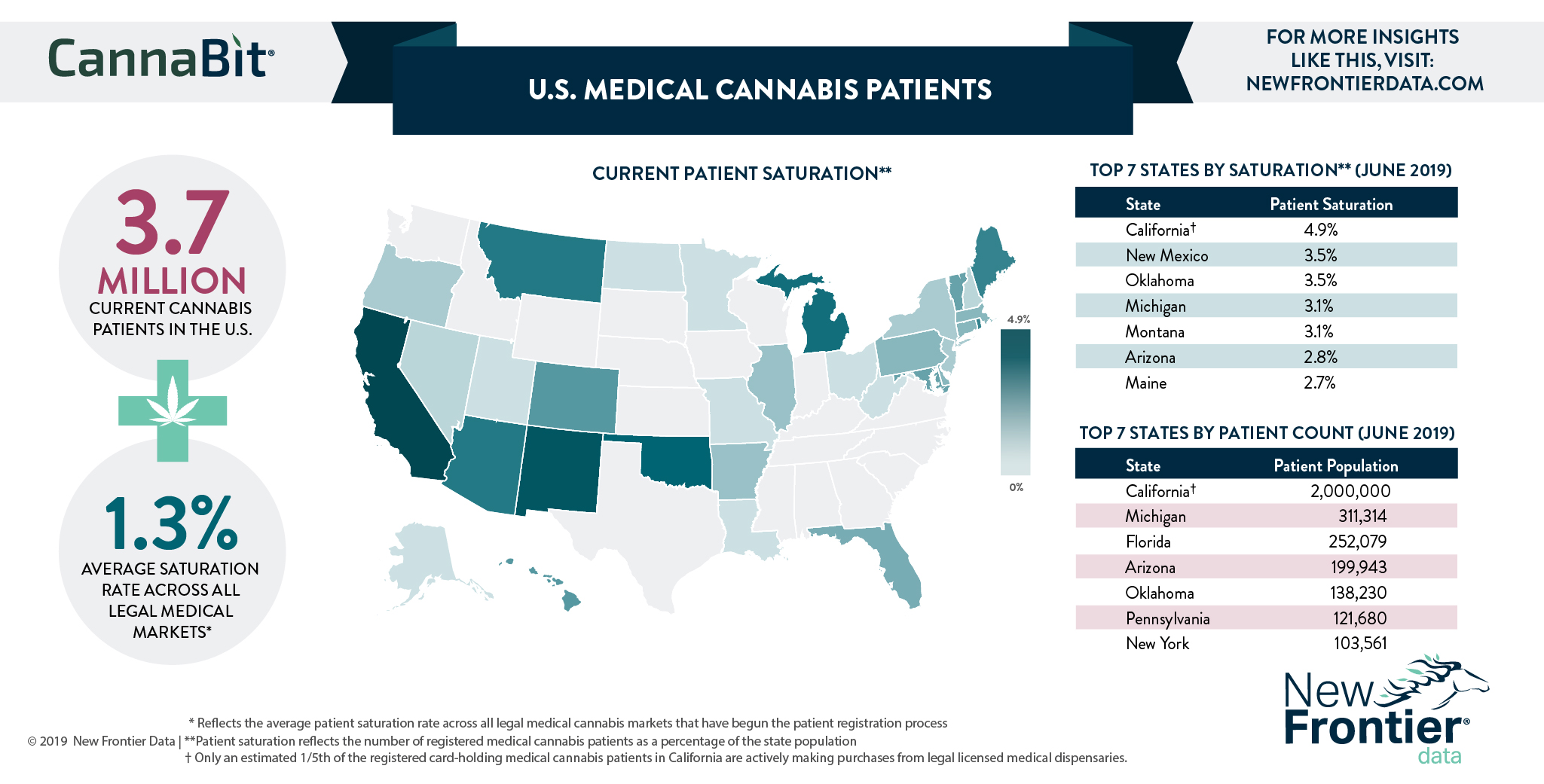

Despite all the negative news, Canopy is a leader in a viable emerging market. For that reason, I believe the current trouble for CGC stock is merely “growing pains.” Cannabis continues to change the way many Americans are thinking about conventional medicine. For evidence of this, investors need to look no further than Florida. The legal cannabis market is growing faster there than almost any other state in the country. From April 2018 to April 2019, the number of licensed dispensaries nearly tripled. And the number of registered patients has almost quadrupled since the beginning of 2018.

Currently, over 23,000 scientific papers espouse the potential medicinal benefits of marijuana. The science behind these reports raises awareness of the medicinal effect of the cannabidiol (or CBD) part of the marijuana plant. CBD is very different from THC — the primary psychoactive ingredient in marijuana.

Not surprisingly, the CBD market is now one of the most rapidly expanding in the United States. Canopy is well positioned to grab a foothold in this market due to its relationship with Constellation Brands. Constellation has paid billions of dollars for a 38% stake in Canopy, and has warrants that will give it majority control.

Even without full legalization, some analysts project the marijuana industry to grow to $50 billion in five years. And if and when full legalization occurs, cannabis may become a $100 billion or even a $1 trillion dollar industry.

Canopy’s Groundwork for Future Growth

This brings me to a key point about the stages of industry growth, and Canopy’s role as one of the largest players in the industry. Currently the cannabis industry is just starting to enter the consolidation phase – – a period highlighted by mergers and acquisitions. Canopy is the largest producer in terms of market cap and it makes sense that they will be an active participant in acquisitions, such as its recent deal to acquire U.S-based cannabis operator Acreage Holdings. But it will take some time for these acquisitions to begin to show up on the company’s bottom line.

Buying or Selling CGC Stock is a Matter of Perspective

Ultimately, how you feel about CGC stock will come down to how you feel about the emerging cannabis sector. This was a sentiment echoed by my InvestorPlace colleague Tim Biggam in a recent article about Canopy.

Do you believe, as I do, that full legalization of marijuana for both recreational and medicinal purposes is a question of when and not if? If so, there are many reasons to buy and hold CGC stock. Or do you believe the United States has significant obstacles to legalization? Or maybe you’re opposed to the industry for any number of reasons.

If either of those statements describe you than Canopy Growth is not the stock for you.

As of this writing, Chris Markoch did not hold a position in any of the aforementioned securities.