Premium athletic-apparel brand Lululemon (NASDAQ:LULU) did it again. In early September, the athletic apparel company most famous for its yoga pants reported second quarter numbers that beat on comparable sales, revenues, and profits, and included a strong, above-consensus guide for next quarter and the full year. LULU stock rallied a few percentage points in response to the beat-and-raise quarter.

This is nothing new for Lululemon. The athletic apparel company has now reported 10 consecutive beat-and-raise quarters — a streak that dates back to early June 2017. Not surprisingly, over that stretch of 10 straight beat-and-raise reports, LULU stock has rallied. And not by a little, by a lot. By more than 300%, to be exact.

Can this red hot rally last forever?

Not forever. Very little in the investment world lasts forever. Especially not a 300% rally over 10 quarters. But this current rally in LULU stock does look good for the foreseeable future to levels above $200.

Why? The fundamentals remain healthy, the optics remain favorable, and the technicals support further upside.

Net net, while the best of the Lululemon stock rally may be in the rear-view mirror, it’s not entirely over just yet, either.

The Fundamentals Remain Healthy

The most important reason to stay long LULU stock is because the fundamentals remain healthy.

This breaks down into parts. First, the company’s numbers continue to be very impressive and aren’t showing any sings of operational weakness. Long story short, comparable sales growth trends remain robust (up 17% last quarter), revenue growth trends remain robust (up 23% last quarter), and both of these project to remain robust for the next two quarters (guide calls for low-teens comps in Q3 and for the full-year). At the same time, gross and operating margins also continue to power higher.

Big picture, then, Lululemon remains a big-time revenue growth company with upside margin drivers, mostly because the company remains the hottest brand in the hottest apparel retail space. So long as all that remains true, LULU stock will continue to be supported by favorable fundamentals.

Second, looking out long term, the fundamentals do support LULU stock at prices above $200. According to my rough calculations, Lululemon in 2019 will own just 1% of the global activewear market — up from 0.75% in 2017 — meaning that the company has both the runway and track record to keep growing at a robust pace. This is especially true considering Lululemon’s target demographic — women — are the demographic that is projected to be the driving force of the activewear market over the next few years.

Thus, Lululemon reasonably projects as a double-digit revenue grower over the next 5-plus years. During that stretch, margins should inch higher, too, because Lululemon should continue to command favorable pricing power over customers. That combination of big revenue growth and margin expansion makes $13 in EPS seem doable by 2025. Based on an athletic apparel retail average 25-times forward multiple and a 10% discount rate, that equates to a 2019 price target for LULU stock of just over $200.

The Optics Remain Favorable

The second big reason to remain long LULU stock is because the optics remain favorable.

Namely, this is a company that’s on fire right now, which has been on fire for the past 10 quarters, and which should remain on fire for the foreseeable future. The Q2 numbers were as good as the numbers have been at any point during this 10 quarter streak, meaning that there aren’t any signs in the financials that this trend is slowing or weakening, at all.

Other data also supports this idea that the Lululemon trend is far from being over.

Web traffic data for lululemon.com is very strong. Search interest trends both domestically and internationally imply that Lululemon is still growing mind-share at a robust rate. And, all the Lululemon stores I visit are always packed… something that has been true for the past 10 quarters.

In other words, the optics here are still very good. When investors look at LULU stock, they see a stock that’s been on fire and which all signs imply will remain on fire for the foreseeable future. That’s the type of stock investors will want to buy into.

The Technicals Support Further Upside

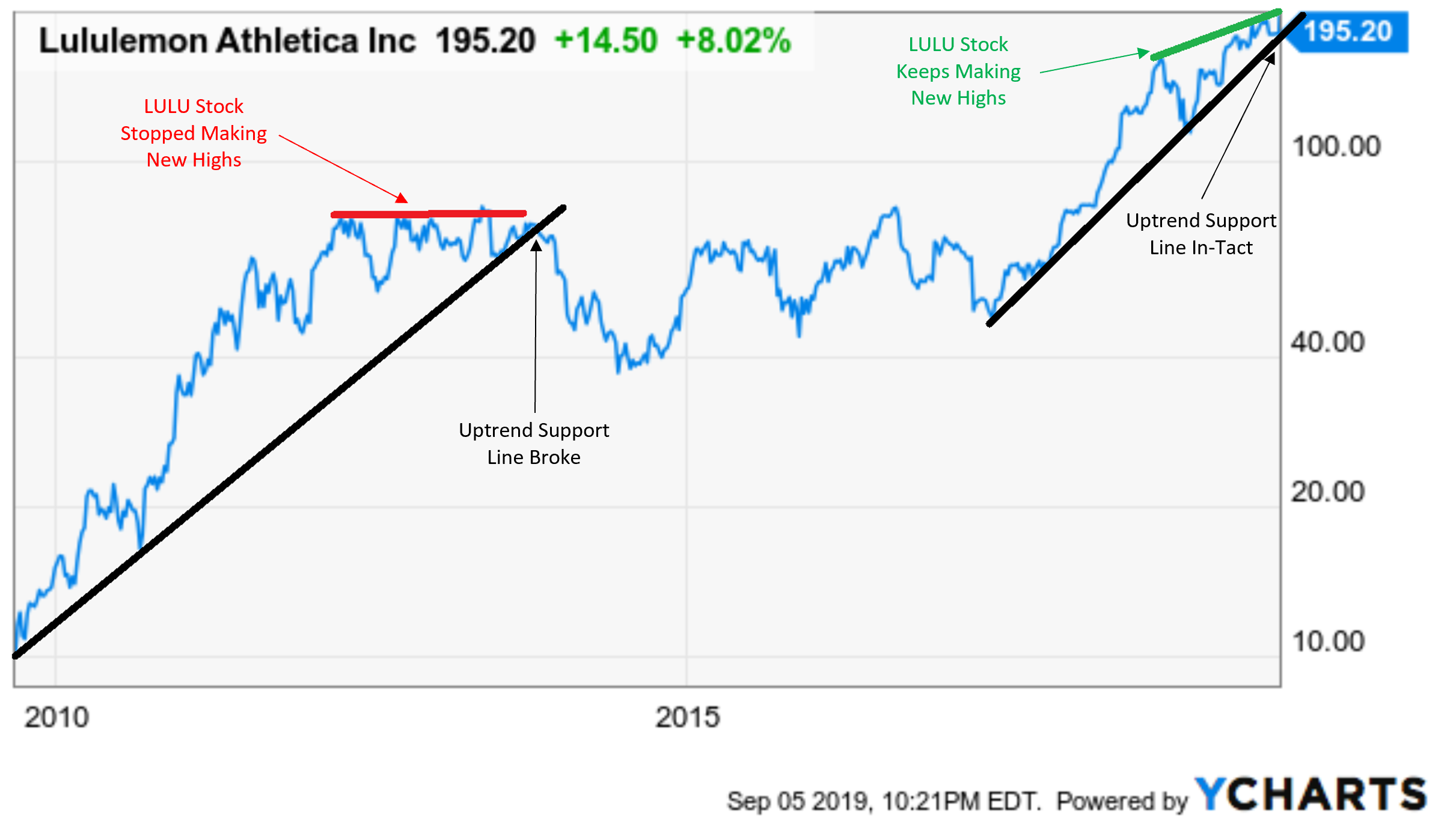

The third big reason to remain long LULU stock is because the chart implies that the uptrend will persist.

Click to Enlarge

See the attached chart. LULU stock has gone through two big upswings in its life on Wall Street — 2010 to 2013, and 2017 to present. In a log scale chart, both upswings look very similar. But, the 2010 to 2013 upswing ended when two things happened on the technical front — the stock stopped making new highs, and the stock broke below its uptrend support line.

Neither of those things are happening today. Instead, LULU stock has consistently made new highs over the past few months, while the stock has also continued to bounce off its secular support line.

Consequently, the technicals imply that Lululemon stock has more room to run here.

Bottom Line on LULU Stock

Lululemon stock won’t go up forever. But, while the best of the LULU stock rally may be in the rear-view mirror, the rally also certainly isn’t entirely over, either. As such, I think the best move is to stick with LULU stock, and let it run above $200.

As of this writing, Luke Lango was long LULU.