Although Starbucks (NASDAQ:SBUX) is enjoying a solid year on paper, Starbucks stock is a fractured investment. In the first half of 2019, shares stormed out of the gate, eventually returning nearly 33%. But in the second half, all that momentum is gone, with the coffee shop incurring a loss of 1%.

Even more startling, since the beginning of September, SBUX stock has looked sickly, dropping 14% in the charts. While the company delivered a beat on earnings per share for its third quarter of 2019, last month, management downgraded their EPS expectations for fiscal 2020.

I don’t find this surprising. In recent years, we’ve witnessed a dramatic rise in full-time wages for those in the restaurant and coffee shop industries. With broadening calls for increased minimum wages, it won’t be long before we start seeing an impact to corporations. Apparently, Starbucks is feeling the heat early, resulting in sharp negativity for Starbucks stock.

That said, SBUX stock represents a global brand whose reach is only expanding. As TradingAnalysis.com founder Todd Gordon suggests, shares might represent a discounted opportunity.

Let’s assess the case for this famous barista, beginning with the upcoming Q4 earnings report:

Starbucks Stock Badly Needs a Beat

I’m not breaking any new ground by saying that mission number one is delivering a strong beat. As everyone knows, the markets represent the ultimate arbiter. And if we look at SBUX stock in the second half, this doesn’t raise confidence. With a convincing performance in Q4, however, management can reshape the narrative.

Ahead of the disclosure, covering analysts peg EPS at 70 cents. Notably, this is near the lower end of estimates, which ranges from 69 cents to 72 cents. In the year-ago quarter, Starbucks delivered an EPS of 62 cents, besting a 60-cent consensus target.

On the revenue front, analysts project

top-line sales to hit $6.7 billion. In contrast to earnings, this figure lies near the upper range of estimates, listing from $6.4 billion to $6.8 billion. One year ago, SBUX rang up $6.3 billion, meeting the consensus target.

Overall, these are reasonable benchmarks. If Starbucks meets its EPS estimate, it would represent a 13% year-over-year lift. For revenue, the company would be looking at a 6% YOY increase.

However, the company needs not just a good showing, but a great one. Thus, the situation gets a little tricky for Starbucks stock.

SBUX Stock Faces a Challenging Macro Environment

Although Starbucks markets itself as a happening eatery and retailer, the reality is that its core product, coffee, is a heavily traded commodity. As such, it’s subject to similar risks impacting other commodities, such as monetary policy, geopolitical tensions, and even the weather.

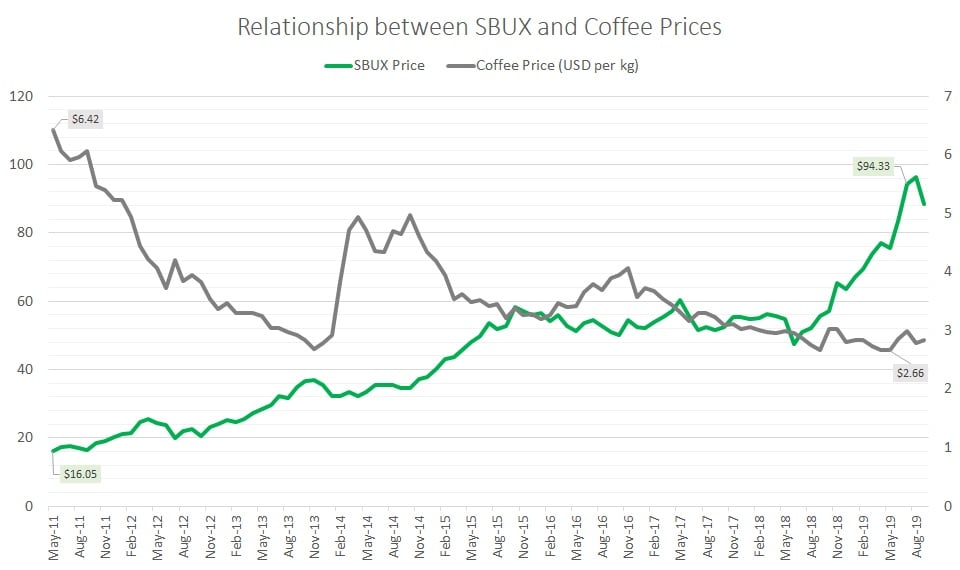

But throughout most of this decade, Starbucks stock has benefitted from positive commodity market dynamics. Since May of 2011, coffee prices have generally declined. Not coincidentally, the SBUX stock price generally increased during this time period.

Click to Enlarge

Mathematically, the coffee price and the Starbucks stock price share an inverse correlation. In fact, I calculated a correlation coefficient of -66%. Stated differently, as coffee prices decline, SBUX rises. Logically, this makes sense: if your inventory costs decline, your profits should increase.

For right now, it appears that coffee prices have stabilized, suggesting continued low overhead for Starbucks stock. However, commodities are inherently wild. For example, coffee prices skyrocketed acutely in the 1990s and earlier this decade.

Furthermore, the recent dovishness by the Federal Reserve makes me suspect that commodities may jump in the future. There’s no question that gold prices benefitted from the Fed’s active role in managing a deflationary environment.

It’s also interesting that management themselves warned about their EPS guidance. Rather than a discount, these macro-headwinds suggest that SBUX stock deserves its recent volatility.

Business Strategy Is a Problem

To me, one of the perplexing mysteries of Starbucks is that their basic, no-frills coffee is not good. If you think about it, they’re actually not a coffee shop; rather, they are a premium coffee shop. If you’re jonesing for a mocha Frappuccino, Starbucks is your place. But basic coffee? Anywhere but Starbucks is your best bet.

In other words, the company imposes all-or-nothing pricing. If you want the good stuff, you have to pay up. Everything else tastes like crap.

Under a bull market, this is totally fine. However, if we fall into a recession like many are beginning to fear, I’d worry about SBUX stock. Starbucks’ premium coffee is a frivolous luxury. And because their basic stuff is wretched, any competitor suddenly becomes a viable competitor.

Thus, I’d play this “opportunity” very carefully. If you’re a conservative investor, you may just want to sit this one out.

As of this writing, Josh Enomoto is long gold bullion.