Without question, one of the biggest surprises of 2019 was the skyrocketing of e-commerce merchant platform Shopify (NYSE:SHOP). In the opening round last year, Shopify stock rang in 2019 with a price of $134. By year’s end, shares closed at $397.58. That’s nearly a 200% return, which is simply phenomenal.

What really makes Shopify stock stand out, though, is how the company has received more than its fair share of criticism. Over the years, one of the most common criticisms is that management won’t release the organization’s churn rate. Especially for a small company, the churn rate would hopefully provide better context and insight. However, Hackernoon.com contributor and ex-Shopify employee Andrew Peek countered that argument with the following insightful commentary:

This is why Shopify won’t report on churn. Because the number won’t be pretty. Businesses fail at an alarming rate. Shopify isn’t some magic bullet that makes your business idea successful. It just reduces the cost of failing.

What’s more, it reduces the likelihood of failure. And that’s all that you should need to know about churn. Though I haven’t worked there in some time, I do recall Shopify merchants succeeding more often than the average business. This shouldn’t come as a surprise. If you give an entrepreneur multiple swings for the same price that they used to get one, they will eventually succeed.

Admittedly I, too, focused on the churn rate, or lack thereof. At the time, I thought it was a credibility issue against Shopify stock. And it still might be. But I also learned that the markets didn’t care, so long as the company was attracting new subscribers. After all, this is a growth organization, and it was doing just that.

Revisiting the Bear Case for Shopify Stock

Given its tremendous success, I also admit another factor: I want to recommend the bullish thesis until Shopify stock hits another plateau. At Monday close, shares had jumped to more than $440.

But I’m also reminded that every rally needs at least a healthy correction before continuing further. Plus, the fundamental evidence I came across suggests that shares have gotten ahead of themselves by a wide margin. Indeed, Shopify stock is so hot that I’m actually tempted to recommend a short position here.

A caveat: I don’t like talking about shorting a company because it immediately creates negative vibes. More critically, shorting is incredibly treacherous. Therefore if you go this route, I suggest using various options strategies to mitigate your overall risk.

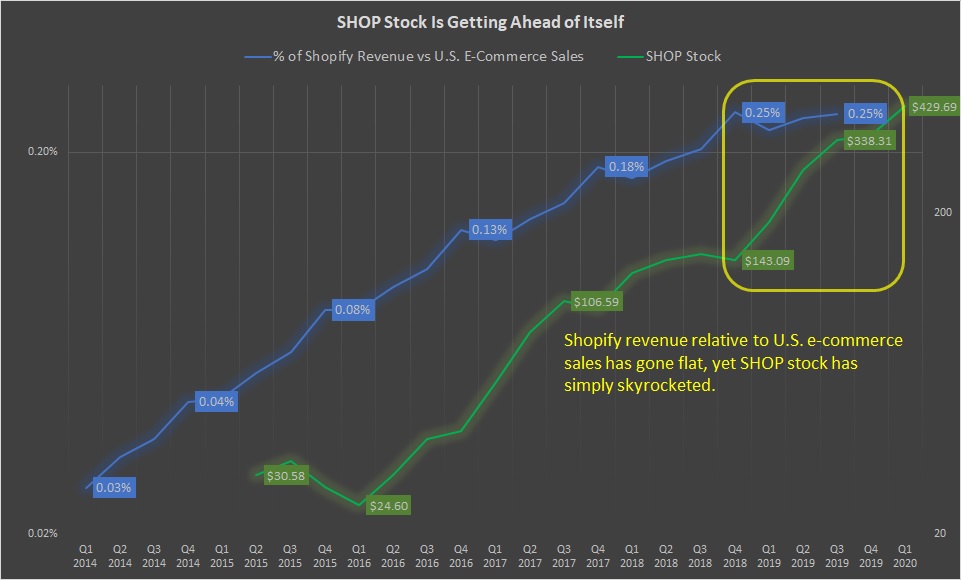

With that warning out of the way, where I’m concerned is that the investor sentiment for Shopify stock has decoupled itself (to the upside) against the underlying company’s fundamentals. Primarily, Shopify’s percentage of sales relative to U.S. e-commerce sales has flatlined over the last four quarters.

Click to Enlarge

Back in the first quarter of 2014, Shopify’s revenue totaled $18.8 million. At the time, U.S. e-commerce sales amounted to $71.2 billion. Do some quick math and Shopify’s revenue accounted for 0.03% of U.S. e-commerce sales.

In Q4 2018, this metric jumped to 0.25%, a whopping 733% gain. In tandem, Shopify stock experienced tremendous gains, from $30.58 in Q2 2015 to $143.09 in Q4 2018, or up 368%.

However, since Q4 2018 the share of Shopify’s revenue against U.S. e-commerce sales has not moved higher than 0.25%. Yet from Q4 2018 through Q3 2019, Shopify stock leapt over 136%. And from then until today, shares have gone up another 27%!

Why It Matters

At this point, skeptics of the bearish thesis may ask, so what? The company is still growing at an impressive rate. For example, in Shopify’s most recent quarter, it rang up $391 million in revenue, a nearly 45% year-over-year lift.

However, while Shopify is undoubtedly growing, the broader e-commerce market is growing as well. Factor in online sales from all sources in the U.S. and Shopify’s growth isn’t that impressive. As I said above, the company has failed to capture additional market share.

To be sure, Shopify has international merchants across 175 countries. But with that international expansion, the company’s total revenue should capture a higher portion of just the U.S. market. Even with this advantage though, the relative growth remains flat.

I’m not suggesting that this is a bad or irrelevant company. It has proved doubters wrong, including me. However, shares have moved disproportionately higher than what its fundamentals justify. And if future quarterly reports fail to move the sales needle relative to the underlying e-commerce market, I can’t imagine investors continuing to pay Shopify’s rich premium.

Obviously, the risk factor is that the company does produce exceptionally robust sales. In that situation, Shopify stock’s present rally would have turned out to be justified. But looking at the contextual sales trend, I highly doubt that it will.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.