Advanced Micro Devices (NASDAQ:AMD) has enjoyed some bullish momentum lately, climbing after a disappointing post-earnings pullback. Despite the latest shake-and-bake action, AMD stock is just 9% off its all-time high and is up more than 46% from the lows.

While that pales in comparison to a stock like Nvidia (NASDAQ:NVDA) — which is up about 80% from its lows and just hit new all-time highs — Advanced Micro Devices isn’t a stock to overlook.

Why’s that? Let’s take a closer look.

AMD Stock Has Growth

Earnings estimates for Advanced Micro Devices have declined over the past 90 days, falling from $1.15 per share to a current $1.04 per share. Even at that figure though, analysts are predicting that 2020 earnings will climb 62.5% this year vs. 2019.

Growth of 62.5% from last year!

Despite the ruthless impact of the novel coronavirus, this company is still forecast to churn out robust growth. That’s expected to come alongside 25.7% revenue growth this year. While 2021 estimates are tough to compute right now — if not outright impossible — analysts expect another strong year. Consensus estimates expect earnings to climb 47% on revenue growth of 20.7%.

For those keeping track at home, that means improving margins too, as earnings growth outpaces sales growth. If that’s the case, it will continue a multi-year trend for AMD stock.

However, this is the most important thing to keep in mind, in my opinion. In 2020, there will be plenty of companies with negative growth. In 2021, many companies will be lucky to generate the financial figures they did in 2019. So the stocks that have growth — and in AMD’s case, robust growth — are worth a premium.

Long-Term Themes Driving Results

When AMD reported earnings in late-April, the results did not impress. In-line earnings and revenue results were just okay, while guidance wasn’t as bullish as investors were hoping for. The quarter wasn’t bad, but with shares basically back to the prior highs, bulls needed to hear something special.

As volatile as AMD stock can be, this is not a quarter-to-quarter story. This company is a long-term play on technology and it has been relentless.

Management continues to go after the big dogs and refuses to lay down and die. CEO Lisa Su has done a stunning job growing AMD over the years. She squashed rumors of her potential departure, leaving investors confident in AMD’s future.

Last quarter, its computing and graphic revenue slipped sequentially, but grew more than 70% year-over-year. Further, the data center should be a robust area of growth. Management expects to grow that segment 44% per year from 2019 through 2023. Even if the company grows at just 25% per year, it will have roughly 20% market share in a $40 billion industry by 2026.

No one cares what’s happening six years from now. But the point is, even by conservative measures, this company has long-term potential. That’s on top of gaming, graphics and other GPU demand that AMD is experiencing. It’s what propelled its financials so significantly over the years.

Revenue has gone from $4.2 billion in 2016 to $6.7 billion in 2019. In that time, net income went from a $497 million loss to a $341 million gain. Also in that time, free cash flow has gone from break-even to $276 million.

Total assets have almost doubled from $3.3 billion to $6 billion, while long-term debt has shrunk from $1.43 billion to just $486 million.

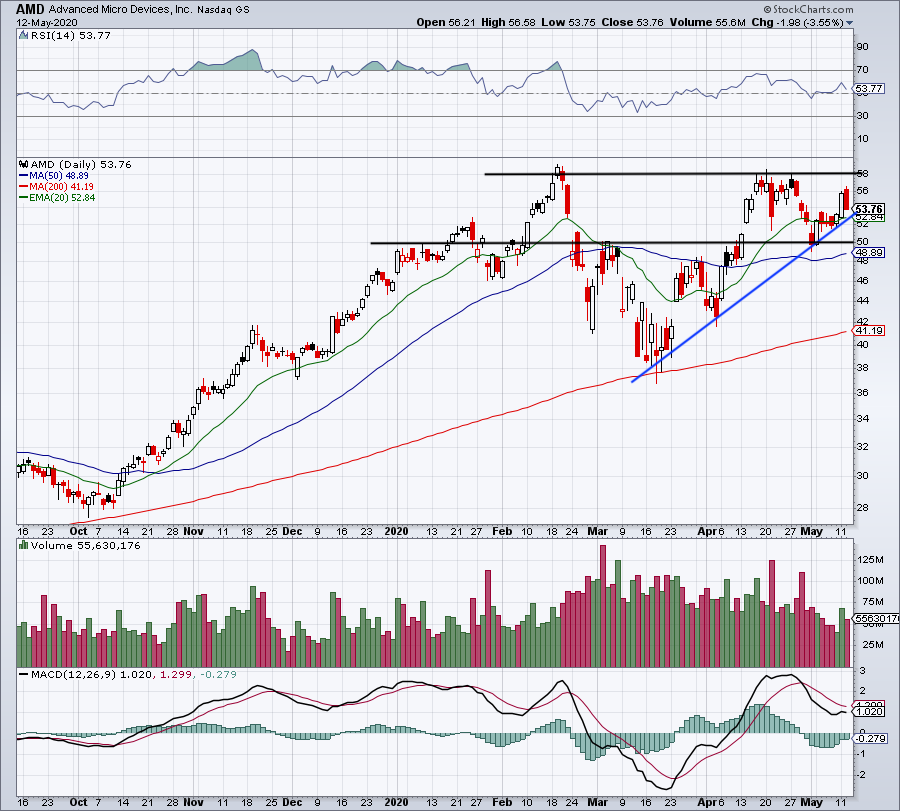

Trading the Chart

Click to Enlarge

In short, AMD stock has tapped into several long-term growth themes, while becoming a leaner and more nimble company. With strong growth forecast to continue, those should be the only catalysts bulls need to see.

But then we’d be forgetting about the chart.

Keep in mind, AMD stock has gone from $28 in October to almost $60 in February. So aside from the Covid-19 panic, the stock is also digesting a massive move over the past seven months.

If we end up in a mild stock market pullback, AMD could come under pressure. For now though, it held $50 on the post-earnings correction, as well as the 50-day moving average and uptrend support (blue line).

Below these three marks and shares may test down into the low- to mid-$40s. Currently, $58 is resistance. Above that area puts $60-plus in play. If support gives way and shares trade down to the 200-day moving average, I’m a buyer.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long NVDA.