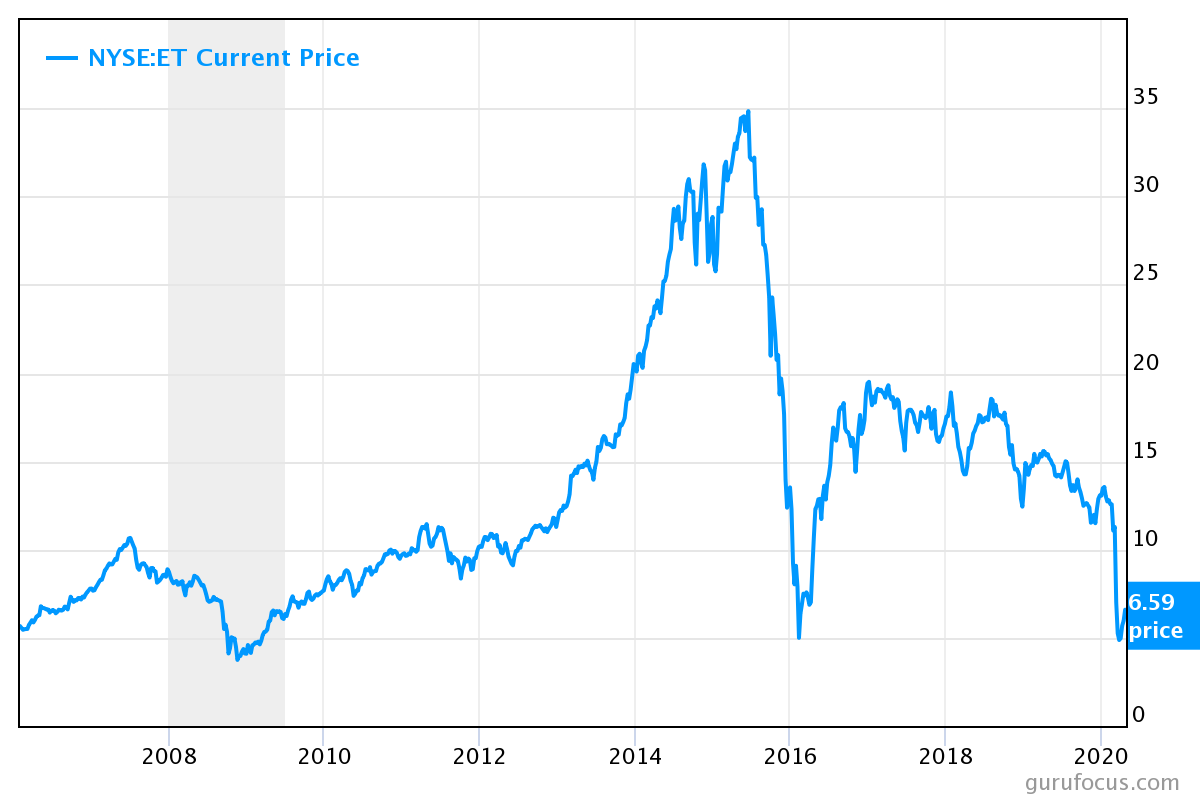

Few things have been more miserable than being long crude oil in 2020 (though being long midstream energy companies isn’t too far behind). Consider the case of Energy Transfer (NYSE:ET) stock, my pick in InvestorPlace’s Best Stocks for 2020 contest.

Between coronavirus market volatility and the plunge in energy prices, Energy Transfer got its head bashed in. At its lows, it was down 76% from its 52-week highs. The shares have nearly doubled off those crisis lows but remain nearly 40% below early March prices.

And the shares weren’t exactly expensive going into the crisis. I recommended Energy Transfer back in December because the shares looked ridiculously cheap even then … before the energy industry blew up.

Click to EnlargeLet’s give Energy Transfer a closer look.

The stock market as a whole isn’t particularly cheap right now. We entered the coronavirus crisis with stock valuations at nosebleed levels, and major market averages never quite reached the valuation lows you’d expect to see at a bottom. But there are bargains out there, and Energy Transfer looks like one of them.

Relative Low Exposure to Crude Oil

It’s understandable why investors are mostly choosing to steer clear of the energy sector. The coronavirus crisis and related lockdowns obviously make things infinitely worse, but the industry was in structural oversupply even before the crisis hit.

Though interestingly, Energy Transfer’s share price has been trending higher throughout April and was essentially unaffected by the negative-crude-price fiasco.

Most of this is due to Energy Transfer’s relatively low exposure to crude oil prices. Only about 5% to 7% of EBITDA is tied to commodity prices, with 85% to 90% fee based. (The remaining 5% to 7% is tied to various spread margins.)

Furthermore, Energy Transfer is actively looking to profit from the crude glut by effectively transforming some of its pipelines into crude storage facilities. According to Bloomberg, ET has identified two pipelines it can use to store about 2 million barrels of oil

.

Energy Transfer does have counterparty risk, of course. The fee agreements are only as good as the balance sheets of the companies obliged to pay them. But it’s worth noting that 81% of its counterparties are rated as investment grade and only 12% are rated below BB.

There is a very real risk of some of ET stock’s fee arrangements being renegotiated in bankruptcy court. But even that would seem manageable given the relatively low exposure to high-risk counterparties.

Energy Transfer Is Dirt Cheap

Energy Transfer’s distribution yield (the equivalent of a dividend yield for an MLP) recently hit all-time highs over 25%. Even after the recent run-up in the stock price, the shares recently yielded more than 14%.

Yield isn’t the best measure of a stock’s valuation because distributions have a way of getting cut when times get tough. Though it’s worth mentioning that Energy Transfer recently reaffirmed its distribution and that is distribution coverage ratio was a healthy 1.96x as of year end.

Let’s forget about the yield for a minute and look deeper. Traditional metrics like the price/earnings ratio tend not to work particularly well for MLPs, as high non-cash expenses tend to distort earnings. But we can use alternative metrics, such as enterprise value to earnings before interest, taxes, depreciation and amortization (EV/EBITDA).

By this metric, Energy Transfer has never been cheaper. The company is trading at a EV/EBITDA ratio of 6.7, less than half the valuation seen for most of 2018.

Cheap stocks can always get cheaper, of course. But there could be some catalysts later this year that will finally shake Energy Transfer out of its funk.

Conversion to C-Corp in the Works?

No one likes MLPs. The structure is confusing and cumbersome, they issue K1 forms that make taxes a beatdown, and limited partners generally don’t have the the same rights as proper corporate shareholders. Many institutional investors are forbidden from investing in them. And the only reason a lot of investors were willing to put up with all of this was the favorable taxation. Limited partnerships avoided corporate taxation, but even this is less favorable now that corporate taxes have been slashed from 35% to 21%.

All of this partly explains why true MLPs like Energy Transfer have performed worse than substantially similar C-corp pipeline operators like Kinder Morgan (NYSE:KMI).

Well, there may be changes afoot. During the February 19 investor call, Chairman Kelcy Warren said that the company would be offering a “C-corp alternative” later this year.

We’ll see. Warren has teased us with this possibility before, and we’re still waiting on it. But should it happen, it should mean a nice pop to the share price. As a point of reference, Kinder Morgan trades at a EV/EBITDA ratio of 10.7, while Energy Transfer’s stands at 6.7.

In the meantime, Energy Transfer offers a yield of nearly 20% that seems safe for the time being. Even if the price continues to lag for a while, the yield alone would make the shares wildly attractive.

Charles Lewis Sizemore, CFA is the principal of Sizemore Capital, an investment advisory firm based in Dallas, Texas. As of this writing he was long ET and KMI.