Perhaps one of the most confusing investment sectors amid this novel coronavirus pandemic is big banking. For instance, a recent report from CNBC indicated that the options market, while implying downside risk for banking giant JPMorgan Chase (NYSE:JPM), actually bodes well for Wells Fargo (NYSE:WFC). From what I can gather, the upcoming results for the Federal Reserve bank stress tests should be better than expected for the latter, invariably boosting WFC stock.

If you’re perplexed at these granular dynamics, you’re not alone. However, in the broader sense, some justification exists for optimism in the big banks. As the Wharton School of the University of Pennsylvania noted before the crisis struck, the financial system is much better off than it was before the Great Recession. Particularly, the banking system no longer carries the magnitude of toxic debt that led to the historic collapse in 2008.

Plus, you can trust Wharton. Only the smartest individuals of our time, titans of academic brilliance such as Donald J. Trump, Ivanka Trump and Donald Trump, Jr. have even a shot of gracing their halls. Therefore, on the surface, WFC stock looks good.

However, my contention is that merely being better capitalized (i.e. having more money), is not enough for this sector. Rather, banks are successful because they are the conduits and beneficiaries of money velocity. And it is velocity that the pandemic has imposed the most pressure.

You know this intuitively. If money velocity didn’t matter, shareholders of WFC stock would be having a jolly good time today. Certainly, with so much money in reserves relative to the pre-Great Recession era, the big banks would be able to walk over this calamity easily.

Why 2020 Is Different for WFC Stock and the Banking Sector

According to the Federal Reserve Economic Data blog, a key reason why the Great Recession was so “great” was because of household debt. Specifically, household debt jumped to 98% of GDP in 2009

. Of course, this indicated that the consumer was too highly leveraged.

As well, the banking sector didn’t do itself any favors, fueling the unsustainable housing boom of the mid-2000s. But when the smelly stuff hit the fan, hardly anyone was able to pay back their toxic debts. Again, this is the reason why some are bullish on WFC stock – we don’t have this circumstance anymore.

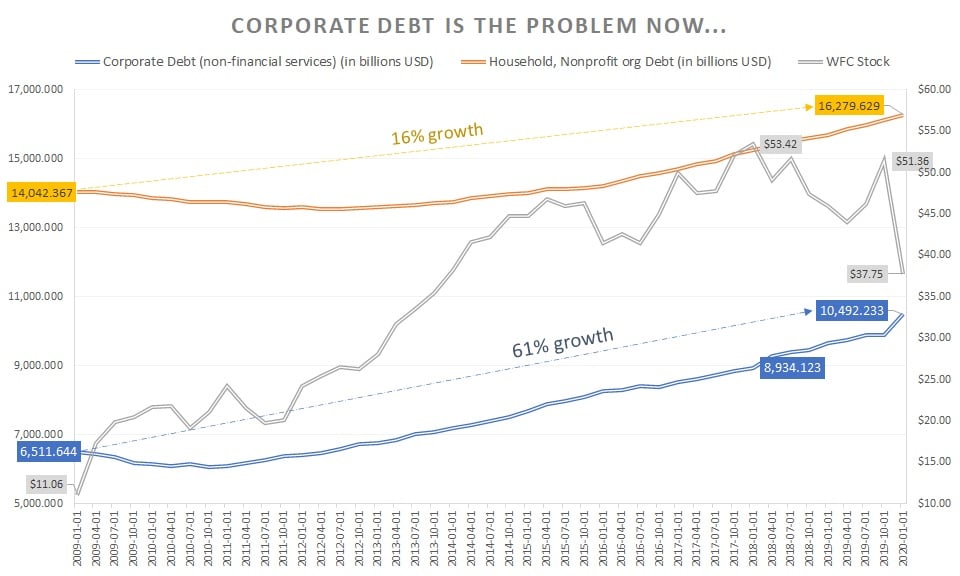

While true, we can’t forget that the fat cats are always looking to fatten their wallets. Thus, in the post-recession recovery, nonfinancial corporate business debt soared substantially, growing 61% between the first quarter of 2009 to Q1 2020.

Click to Enlarge

That’s not to say that household debt didn’t increase because it did. But during this period, this segment grew 16%, down massively from corporate debt growth. It was also slower than the pace of GDP growth.

Now here’s where it gets interesting. Between Q1 2009 to Q1 2020, WFC stock more than tripled in value. Mathematically, we know that Wells Fargo’s market value expanded more heavily on the expansion of business loans than consumer loans. The correlation coefficient between WFC versus corporate debt and household debt is 85% and 66%, respectively.

In a genuine bull market, this is acceptable. Typically, businesses acquire debt to advantage opportunities in the here and now. Later, they will pay off the debt as they reap the benefits of their growth strategy.

But what happens when the justification for making those loans stops abruptly? If you’re thinking about buying WFC stock, this, and not how much money the bank has is the real question.

Velocity Will Slow but By How Much?

A common observation that keeps popping up is the disconnect between Wall Street and Main Street. After thinking about this, here’s my take: the disconnect isn’t based on the fundamentals but rather on timing. If this Covid-19 crisis doesn’t fade soon, we eventually will be talking about “the connect” between these entities.

If you consider the details, the picture does not look good. Yes, we’ve all heard about people not being able to pay their rent but what about businesses that employ those very people? According to the Washington Post, “Nearly half of commercial retail rents were not paid in April and May.”

When you look at the stunning growth of corporate debt and the sudden closure of the economy, this shouldn’t surprise you. If money velocity goes to zero, the economy goes to zero.

Of course, we’re not headed to a complete annihilation of our country. But certainly, money velocity has slowed down. How much it will slow to in the coming months and years ahead is what will likely determine the long-term trajectory of WFC stock. Personally, I’m hopeful but I’m also not holding my breath.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare. As of this writing, he did not hold a position in any of the aforementioned securities.