Invariably, the novel coronavirus has created winners and losers in this market. Fundamentally, it appears that CarParts.com (NASDAQ:PRTS), formerly known as U.S. Auto Parts Network until recently, is destined to be one of those losers. If I’m being honest, the signs suggest that PRTS stock is a shorting candidate. Shares have jumped almost outrageously, yet the underlying business model appears contextually flawed.

As the name suggests, CarParts.com maintains an inventory of various automotive parts and accessories. Primarily, the company specializes in “automotive replacement collision, repair, and maintenance parts.” I would argue that under any other circumstance, PRTS stock is a compelling investment (at the right price). But on the surface, the price is out of control for a busted business model.

Due to the initial coronavirus impact, most state governments issued stay-at-home orders. Effectively, this reduced automotive traffic to a fraction of what it was. Moreover, it wasn’t just urban areas that saw steep declines, where jurisdictional authorities pushed social distancing. Rather, rural regions suffered similar declines in year-over-year traffic volumes from March through May.

Of course, this dynamic directly impedes PRTS stock. With a huge decline in driving, there’s less demand for maintenance parts. More importantly, with less traffic comes less automobile accidents. Given that this is the crux of CarParts.com’s business, the dramatic rise in PRTS seems unjustified.

In fact, many auto-insurance companies have refunded some portion of drivers’ monthly premiums. This unusual move demonstrates how traffic accidents have plummeted, presenting a headwind for PRTS stock.

Also, with a possible economic crisis over the horizon, this severely disincentivizes driving due to cost reasons. Yet the broader narrative for CarParts.com isn’t so simple as it first appears.

The Unintuitive Bull Case for PRTS Stock

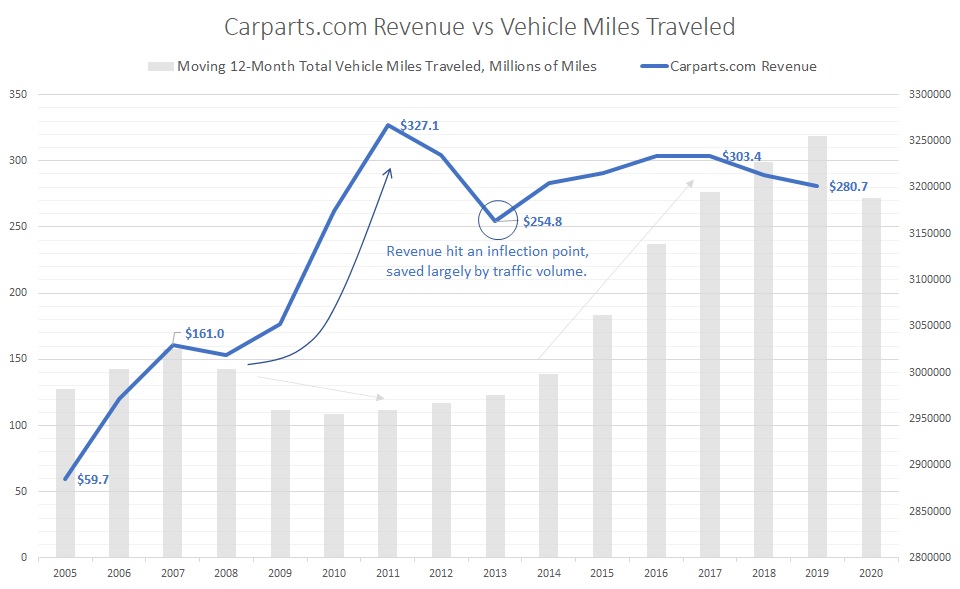

In the latter half of 2007, the economy peaked as unbeknownst at the time, we were headed toward the Great Recession. Not surprisingly, the moving 12-month tally of total vehicle miles traveled also plateaued. From November 2007 onward, vehicle miles traveled declined until early 2015, when this metric returned to break even.

Intuitively, you might expect CarParts.com’s revenue to decline or at least stay rangebound. Yes, an incentive exists to extend the life of your car as much as possible. However, in a deflated jobs market, you’re also likely to spend money on core essentials, like housing and nourishment.

Yet between 2008 through 2011, the correlation coefficient between CarParts.com’s sales and vehicle miles driven was -63%, indicating an inverse relationship. Sure enough, take a look at PRTS stock during this time frame. After incurring an initial shock, shares bounced from 2009’s doldrums and peaked in early 2011.

Click to Enlarge

Right up until the point where the pandemic began shuttering states’ economies, vehicle miles driven were looking very strong. Subsequently, CarParts.com’s revenue showed much promise. In its first quarter of 2020 earnings report, the company generated $87.8 million in revenue, up 17.5% from the year-ago quarter.

So, without this coronavirus, it’s conceivable that PRTS stock would have increased significantly. As well, once the pandemic is over, shares have some upside credibility.

And despite the present ugliness, CarParts.com has some legitimate catalysts in this malaise. Primarily, people still need to get around. With many folks still scared of using ride-sharing services like Uber (NYSE:UBER), they’re electing to drive themselves.

That’s why you’re seeing – again, unintuitively – used-car companies like CarMax (NYSE:KMX) perform very well. And what do folks who drive used cars need? Parts. With CarParts.com’s “contactless” e-commerce platform, PRTS makes sense on some levels.

Nevertheless, It’s a Risky Ride

But now, we’ve arrived at the deciding moment: would I buy PRTS stock after considering the key bullish and bearish arguments?

I don’t like to leave my articles on an even-handed note, just for the sake of avoiding hate mail. With that said, in my opinion, I believe PRTS stock is too risky at this price point.

Though not discounting CarParts.com’s historical strength as a recession-resistant name, I think it’s telling that the stock price and revenue began slipping from 2011. That was really an inflection point. Until automotive traffic started picking up substantively, PRTS did not look like a good investment.

Also, consider that the coronavirus pandemic is unprecedented. Admittedly, this cuts both ways. With a sharp decline in traffic, it’s possible for a quick, V-shaped recovery. But it’s also just as possible that this potential economic crisis may be the worst in American history. After all, you can’t just have millions of Americans facing homelessness and not have that impacting every branch of this consumer-driven economy.

Plus, PRTS stock may have priced in the enthusiasm that I just mentioned. And while a positive earnings report could do wonders, if the economy is in tatters, it might be a moot point.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare. As of this writing, he did not hold a position in any of the aforementioned securities.