Here we are in mid-July, and the novel coronavirus remains a runaway train for much of the U.S. The airline industry shows no signs of life, and airline stock holders are wondering if the rout is an opportunity or a trap. Fortunately, there’s a surprising aviation company that will survive the pandemic unscathed: General Electric (NYSE:GE) and GE stock.

The Covid-19 pandemic created a rare opportunity to buy GE stock for a fraction of its true value. As investors fled aviation stocks, many overlooked how resilient GE’s jet engine servicing business remained to industry downturns.

“It’s actually harder on an engine for aircraft engines to sit idle in a hanger – or worse – a ramp queen,” according to a widely-circulated FAA safety memo. So while Boeing may stumble from delayed aircraft orders, GE Aviation will continue to churn out profits as airlines grudgingly pay for service on their grounded fleets. Once investors add in GE’s profitable healthcare business and improving debt structure, GE stock remains a clear buy.

Click to Enlarge

GE Stock’s Hidden Gem

Today’s GE is almost unrecognizable to the industrial conglomerate that “Neutron Jack” Welch built in the 1990s. Household appliances? Sold to Chinese maker Haier in 2016. Diesel locomotives? Traded to Westinghouse in 2019. So what does GE do today?

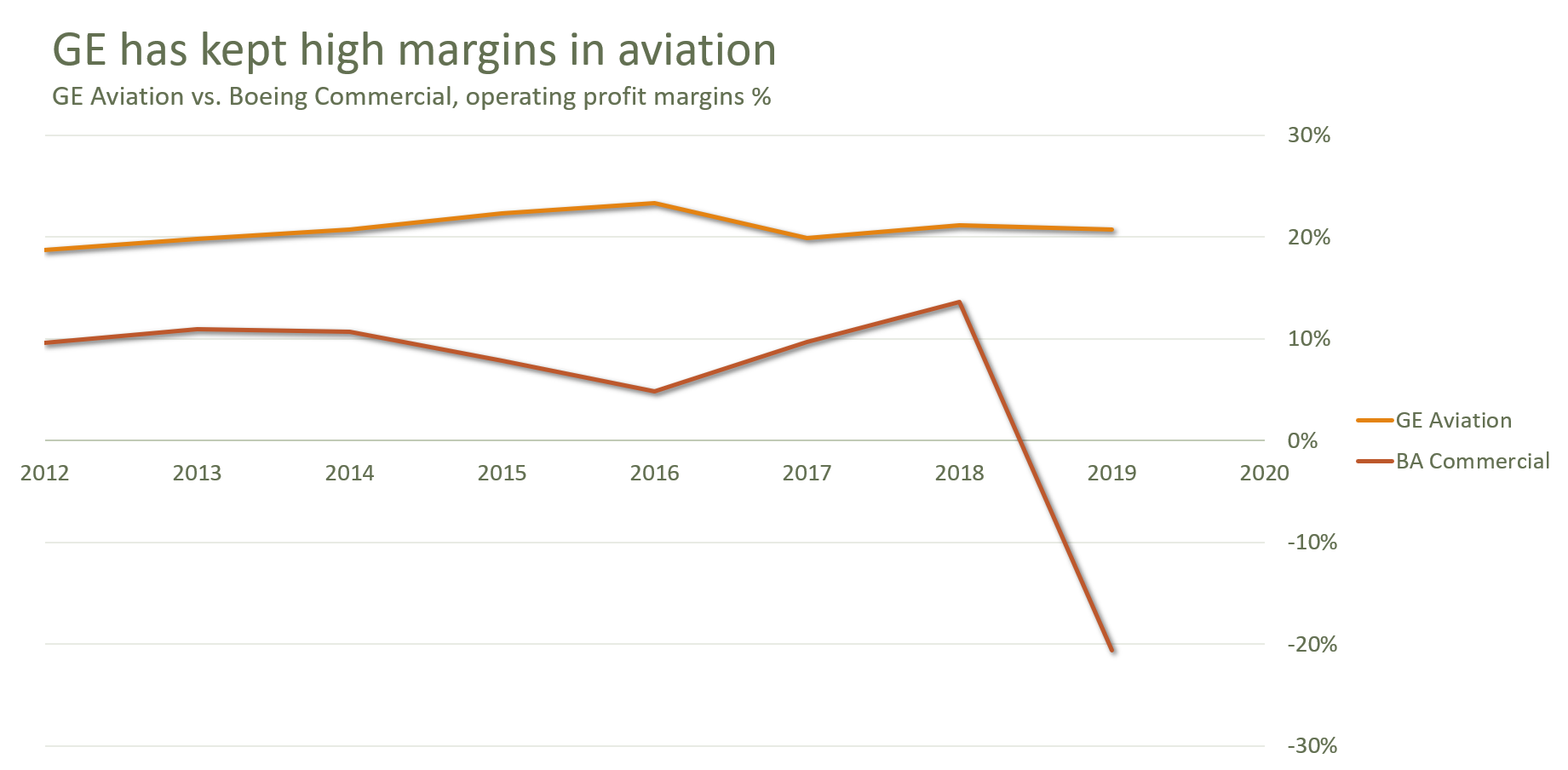

While the company still retains significant business in healthcare and power generation, GE’s true crown jewel is its aviation segment, which provides 65% of corporate profits. There, GE operates in a high-margin duopoly for aircraft engine design and production. In wide body jets, GE competes with Rolls-Royce (LON:RR). In narrow body jets, Pratt and Whitney, owned by parent company Raytheon (NYSE:RTX).

The jet engine industry operates on a razor/razor-blade model. In other words, GE engines must be maintained and serviced by GE itself.

The tight-knit business model gives GE a huge advantage. Airlines will often choose between dozens of aircraft models and leasing companies. But when it comes to a new engine manufacturer, airlines despise change. Besides safety concerns, airlines know that buying a new engine type will also mean hiring an entirely new service team. And adding to cost is the last thing on airline companies’ minds.

Click to Enlarge

This wide-moat business has greatly benefited General Electric. The company commands an astonishing 58% of the global aircraft engine market and produces an eye-popping 20% margin. Even Boeing, a firm that operates in a near-duopoly with Airbus, doesn’t come close.

While airlines can choose to delay buying new aircraft, no company can afford to delay servicing their engines, even if planes are grounded. GE stock is an ideal aviation investment for risk-aware investors.

General Electric’s Long Turnaround

GE’s future didn’t always seem so bright. Long a poster child of industrial conglomerates, General Electric hit turbulent times during the mid-2000s. Unrelated businesses, such as GE Capital, lost the parent company billions. Critics panned GE as too complicated and totally unmanageable.

And they were right …

The company’s unwieldy businesses floundered under Jeff Immelt. Even shedding its appliance business and long-term care insurance couldn’t reverse the company’s fortunes. By the time Jeff Immelt resigned in 2017, profits had plummeted from its 2007 peak of $22.2 billion to negative $8.9 billion.

To add to the embarrassment, Dow Jones dropped GE from the Dow Jones Index the following year.

In 2018, GE’s board finally turned to veteran CEO, Larry Culp, for help. And Mr. Culp was no ordinary CEO. As the head of Danaher (NYSE:DHR) between 2000-2014, he was credited with turning around the industrial giant. Over his tenure, Danaher’s shares grew 465%, versus the S&P 500’s 105% gain.

As the new head of GE, Larry Culp has moved quickly to shed General Electric’s legacy businesses. The company sold GE Biopharma in 2018 for $21.4 billion dollars and its 63% stake in energy giant Baker Hughes. In 2020, proving no business is truly sacred in a turnaround, Mr. Culp sold GE’s lighting business to Savant Systems for $250 million.

GE is now a leaner company.

Culp’s actions had an immediate effect on GE’s mountain of debt. Long-term borrowings decreased from $108.5 billion in 2017 to $67.2 billion in 2019. And while the company’s 2.2x interest coverage (interest/EBIT) still worries many investors, Culp’s 2018 decision to cut dividends to a penny means GE’s cash position will quickly improve over the next several years. Analysts surveyed by Markets Insider expect GE’s net debt to reach zero by mid-2023.

GE Healthcare Provides Another Wide-Moat Business

As a bonus to GE’s investors, General Electric also owns a high-quality healthcare division. Healthcare provides the remaining 35% of GE’s operating profits.

Two-thirds of GE’s healthcare business comes from medical imaging, where it operates in a duopoly with Siemens. Operating margins of 19% rival GE Aviation’s, and the U.S.’ aging population makes this an attractive long-term business.

What Does This Mean For Investors?

Analysts estimate that General Electric’s earnings before interest and taxes (EBIT) will grow from $3.7 billion in 2020 to $9.2 billion in 2022, as GE either sheds or improves its remaining legacy businesses. Interest burden will also decline as CEO Larry Culp continues to cut down GE’s legacy debt. Put together, analysts predict GE’s net profit will rocket 1,080% to $1.08/share by 2023. Investors would be foolhardy to miss out.

Tom Yeung, CFA, is a registered investment advisor on a mission to bring simplicity to the world of investing. As of this writing, Thomas Yeung did not hold a position in any of the aforementioned securities.