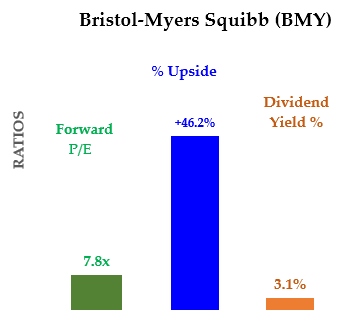

Bristol-Myers Squibb (NYSE:BMY) is incredibly cheap. For example, based on earnings estimates, BMY stock trades at just 7.8 times next year’s earnings.

In addition, it has an attractive dividend yield of 3.11%, which is likely to increase soon. I estimate the stock is worth at least $84.47, or 46% more than its present price.

And that is after discounting its real worth significantly, to add in a margin of safety. The target price is primarily based on its expected earnings and dividends, its history, and comparisons with its peers.

BMY Stock Earnings and Dividend Expectations

Last quarter, the company blew away analysts’ earnings forecasts. It is likely to do so again this quarter. For example, Bristol Myers was supposed to hit $1.48 earnings per share in the second quarter, according to analysts’ average estimates. But the actual EPS came in at $1.63, or over 10% higher than forecasts.

This quarter it is likely to do the same thing. Analysts’ expectations are again at $1.49 per share, just a penny higher than their low-ball expectations last quarter.

Moreover, on Sept. 10, Bristol-Myers Squibb declared its fourth quarterly dividend of 45 cents per share. You can see this stellar dividend payment history in the chart below.

Click to Enlarge

By early December it is likely to announce a dividend increase, if its past history is a good guide. I expect the company will raise the payout by over 10% to $2.00 per share.

Bristol-Myers Squibb’s historical dividend yield has been 2.97% over the last four years, according to Morningstar. BMY stock is worth $67.34 per share. To get that result, divide $2.00 by 2.97%. That equals the target price of $67.34, or 16.7% more than today’s (Sept. 21) price of $57.77.

Historical P/E and Comps

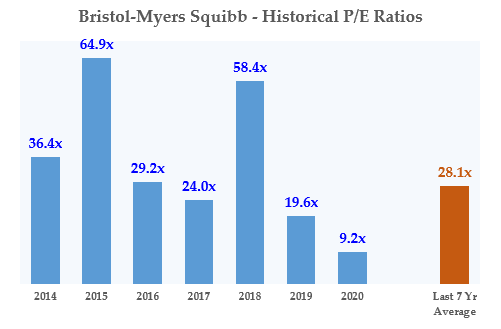

Historically, Bristol-Myers Squibb has had very high price-to-earnings (P/E) ratios. You can see this in the chart on the right.

Click to Enlarge

It shows that the average P/E over the past seven years has been over 28x, but ranged from 9x recently to over 64x earnings.

This analysis is based on figures provided on Morningstar’s Valuation page for BMY stock.

If we apply that earnings multiple to Bristol-Myers Squibb’s EPS forecasts for 2021, $7.45, we would have a price target of $209.50. That is over 263% higher than today’s price of $57.77.

Click to Enlarge

Just to be safe, and to introduce a margin of safety, let’s use just 50% of that number. So now the target price is $104.61 per share, or 81% higher than today.

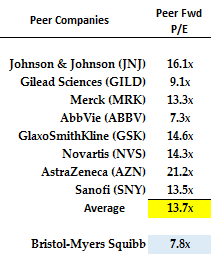

In addition, we compare the P/E ratios of a number of the drug maker’s peers, we find the stock is worth much more as well, as seen on the right.

It shows that the average of eight of Bristol-Myers Squibb’s peers’ P/E ratio is 13.7x forward earnings.

By contrast, BMY stock trades at almost half that level at 7.8 times 2021 earnings.

This implies that the stock should be worth $102.07, or 76.7% higher than today. But, again, to use a margin of safety I applied a 20% discount. That puts BMY stock’s value at $81.47, or 41% higher than today.

What to Do With BMY Stock

So now we have three ways of valuing Bristol-Myers Squibb stock. Using its own dividend forecast and historical yield, the price target is $67.34, or 16.6% higher.

Using a historical P/E ratio analysis, the price should be $104.61, using a 50% discount for a margin of safety. That is still 81% higher than today.

Click to Enlarge

And using a peer analysis, using comp P/E ratios, the price should be $102.07, using a 20% discount. That is still 41% higher.

You can probably guess what’s next. The average of these three price targets is $84.47, which represents a potential upside of 46.2%.

Moreover, even if it takes two years for BMY stock to rise to that target, it still represents a compound annual gain of 20.9% each year.

In addition, with its 3.1% dividend yield, the stock’s total return each year will be 24%. That is a reasonably good return for most investors.

The patient value investor will average cost into BMY stock. It has the potential to gain a substantial amount just based on a re-rating of its multiples.

Last quarter the stock rose after its earnings came out, as Barron’s Josh Nathan-Kazis reported in May. I suspect the same will happen this quarter. Moreover, the company has already guided for its earnings this year to be between $6.00 and $6.20 per share.

Those are the numbers on which I based my valuation. Therefore, I expect that most serious value investors will average cost into this stock to participate in its expected re-rating.

On the date of publication, Mark R. Hake did not have (either directly or indirectly) any positions in any of the securities mentioned in this article.

Mark Hake runs the Total Yield Value Guide which you can review here.