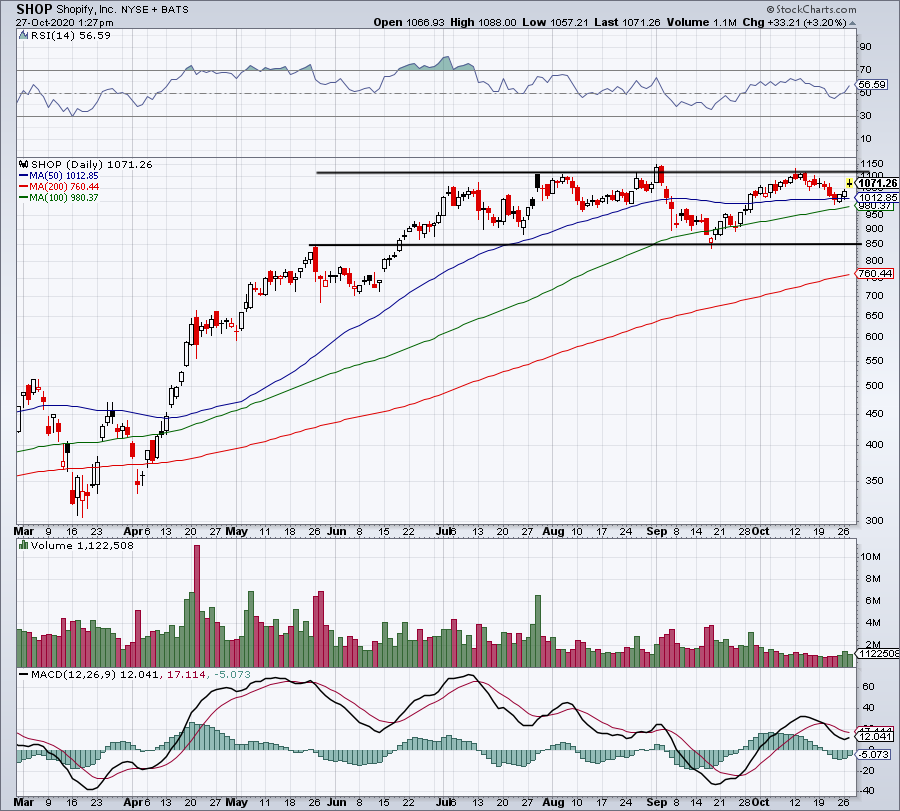

Shopify (NYSE:SHOP) has been a fascinating holding this year. At first, shares were caught up in the beatdown that seemingly every other stock suffered from in the first quarter. But then something happened, and it resulted in Shopify stock exploding higher.

The stock rallied 250% from its March lows to its highs in early September. That doesn’t happen to just any stock, even though the broader indices have roared higher.

However, something else made Shopify stock even more interesting. Shares were pummeled in February and March, falling almost 50% from peak to trough. However, while the rest of the market was bouncing, Shopify was back under pressure.

That came after a guidance update from management. It spooked investors, who then sold the stock lower by more than 22% in just three days. Investors shouldn’t kick themselves if they weren’t able to capitalize, but they should learn for next time.

Shopify stock looked like it was going to retest the lows on that guidance update, but instead found its footing and ripped to the upside.

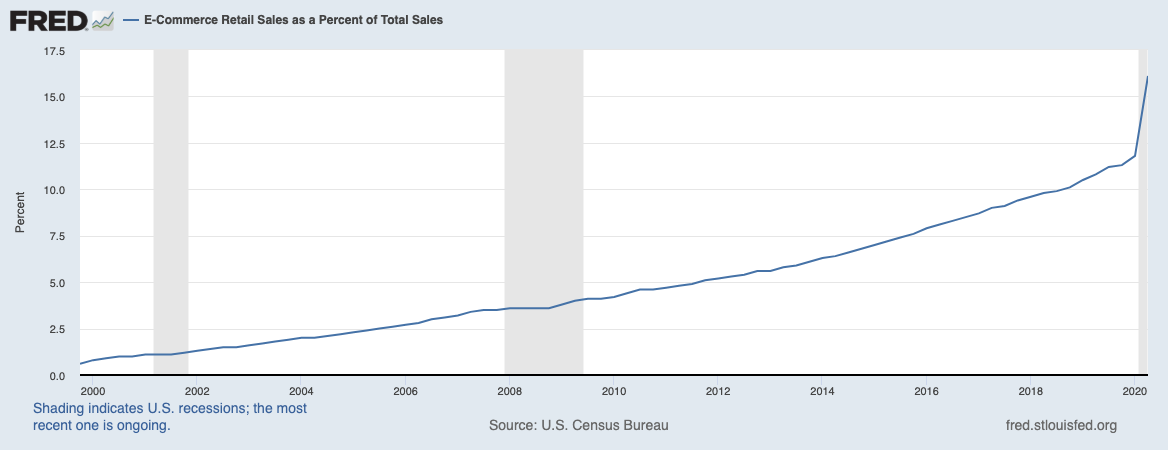

E-Commerce Trends Support Shopify

Click to Enlarge

We’re looking for secular trends that are not seeing a temporary boost from the novel coronavirus. Instead, we’re looking for secular trends seeing an acceleration in growth. That said, e-commerce fits that observation very well.

Online sales have continued to make up a larger and larger portion of retail sales for years now. And the above illustration highlights that fact.

It’s really no surprise, either. As the internet becomes a more powerful place — full of analytics, targeted advertising and plenty of convenience — it only makes sense for customers to shift their habits online.

With shoppers looking online, companies had to migrate there too. But it’s not just big-box stores and well-known retailers making the shift. We now have small- and medium-sized businesses, as well as the individual shop owners opening online operations.

That’s where Shopify steps in.

It can handle business for the single-person operation, up to Kylie Jenner’s cosmetics business to a multi-billion firm. And as long as the internet and e-commerce continues to expand, so too shall Shopify — and that’s why investors are willing to pay such a premium for it.

Breaking Down Shopify Stock

That premium is what’s caused many investors to miss out on Shopify stock. Simply put, this is an expensive name. But guess what? It’s only gotten more expensive this year.

Valuation only goes so far as a negative catalyst. Unfortunately for many of Shopify’s short-sellers, the valuation hasn’t really been the kryptonite they were hoping for. At the end of the day, high-quality growth stocks with incredibly long runways come with high valuations.

That’s been the case for the last 15 to 20 years in tech. Think back. Look back. The biggest winners over the last decade or two had what many considered a sky-high valuation. “No way can we buy this stock — it has a triple-digit P/E ratio and trades at 30 times sales!”

Admittedly, those valuations can give a rational investor pause. Obviously, not every one pans out to be a huge winner. But the high-quality growth stock that went from a $100 billion market capitalization in 2012 to a $1.6 billion valuation this year never came cheap. Same with the streaming giant that went from a $20 billion market cap in December 2014 to a $220 billion company now.

Good stocks don’t come at a discount, and Shopify is no different.

Shopify stock now trades at about 400 times this year’s earnings estimates and 50 times this year’s sales estimates. Also, based on next year’s expectations, shares trade at roughly 35 times revenue — provided the estimates are accurate (although likely conservative).

The point is, this name is not cheap, but it shouldn’t be.

Building the Future

Click to Enlarge

Collectively, analysts expect 65% revenue growth this year and 32.4% growth next year. On the earnings front, estimates call for a 730% explosion in earnings growth this year.

Cash flows are also moving in the right direction. In 2018, Shopify had free cash outflow of $32.2 million. In 2019, it swung to free cash flow positive, generating just over $8 million in free cash flow. It’s not much, but the swing from negative to positive is noteworthy. And now, its trailing free cash flow hovers near $50 million and we haven’t even hit the holidays.

Additionally, its operating cash flow is potentially an even more important metric. Free cash flow “suffers” as Shopify reinvests in its business. Here’s its operating cash flow from 2017 to 2019: $7.9 million, $9.3 million, $70.6 million. The trailing 12 months are even better, at $103.4 million.

But more importantly, Shopify is building out a new platform for e-commerce. It’s not one that forces millions of businesses to conform. Instead, it’s a platform that encourages entities as small as entrepreneurs and as large as billion-dollar brands to harness control of their online operations and dominate the customer experience from start to finish.

The stock is expensive, but it’s also operating in a secular growth industry. It’s changing the game and that doesn’t come cheap. It’s also profitable, cash flow positive and has a strong balance sheet.

That said, look for the domination to continue.

On the date of publication, the author held a long position in Shopify.