As the U.S. Navy SEALs like to say, it pays to be a winner. Certainly, it pays to be an early-bird shareholder in Landcadia Holdings II (NASDAQ:LCA). Despite the horrors and the everyday inconveniences associated with the novel coronavirus pandemic, the appetite for gambling has been surprisingly robust. Therefore, we shouldn’t be too terribly surprised that LCA stock has so far performed outstandingly.

To be sure, Landcadia, which will be known as Golden Nugget Online Gaming following a reverse merger approval, received a nice shot in the arm recently. Before heading into the Thanksgiving holiday, the company announced that the New Jersey Casino Control Commission granted regulatory approval for the merger with GNOG. Now, Landcadia must wait for approval by the Securities and Exchange Commission (SEC).

Naturally, LCA stock skyrocketed on the announcement. With more states opening up to online gambling, Golden Nugget Online is poised to capture market share. And this notion is further evidenced by the aforementioned appetite for such risky endeavors. After all, the Wall Street Journal discussed at length how millions of physically displaced worker bees have begun channeling their inner Gordon Gekko.

If you’ve seen the movie Wall Street, you’ll know that the film’s antagonist didn’t make his money by stocking money away in a mutual fund, nor by playing by the rules. But stocks usually take time to actualize their profitability narrative, if they actualize at all. With online gaming, you can potentially receive immediate gratification.

With the addiction setting in from coronavirus-fueled securities trading, it’s not inconceivable that Landcadia can harness this demand into its online casino platform; hence, the cynical narrative for LCA stock.

But as our own Dana Blankenhorn expertly wrote, Landcadia may not have the clearest motivation. Blankenhorn stated, “[GNOG controlling shareholder Tillman] Fertitta didn’t get to be the owner of the Houston Rockets by making other people rich. Landry’s [restaurant/casino owned by Fertitta] doesn’t have partners. He feeds his ego with a CNBC show called Billion Dollar Buyer. If he’s looking for you to partner with him, you need to ask why.”

Should investors take a shot on LCA stock? Or is it best to wait it out, particularly with shares having jumped so much?

First, Look to the Health of the Broader Market

I must admit that Blankenhorn made me rethink the idea of betting on this special purpose acquisition company. Although the online gambling market should be big, LCA stock may also be a case where you’re helping a billionaire more so than you’re helping yourself. As Blankenhorn put it:

“The miracle of a SPAC is there’s no S-1. You’re taking the promoter’s word on things. As Chamath Palihapitiya of Social Capital, one of the best-known promoters, put it recently, he just goes on CNBC and sells the deal.

“SPACs are not profitable when they come public. They’re operating companies that have exhausted venture capital’s patience, like Virgin Galactic (NYSE:SPCE). In this case, it’s even worse, because the company you’re buying is controlled by the SPAC promoter.”

Still, let’s be fair: Plenty of companies have performed well despite the underlying executives’ selfish ambitions. It’s called investing.

Therefore, I wouldn’t avoid LCA stock based solely on Fertitta’s questionable self-promotion. Really, it’s part of the game. However, what could cast doubt on the stock’s future viability is the health of the stock market.

Presently, I believe that the S&P 500 is charting a bearish broadening wedge pattern. This is a volatile situation where bulls and bears negotiate wildly while driving up the target asset. However, the formation typically ends up resolving itself to the downside.

Of course, I understand the criticisms against technical analysis, which sometimes sounds like charting voodoo. However, it’s interesting to point out that Sven Henrich, founder and lead market strategist at NorthmanTrader, stated that the S&P 500 was a screaming sell in September of 2019.

How right he was, and he had no idea that the coronavirus pandemic was coming!

LCA Stock Is Likely to Fail if the Market Does

Initially, you might think that LCA stock will outperform the broader market even if the latter tumbles. As I mentioned earlier, online gambling has become one of the hottest tickets in town. Further, consumers have demonstrated that despite a terrible pandemic, their personal economies have yet to suffer.

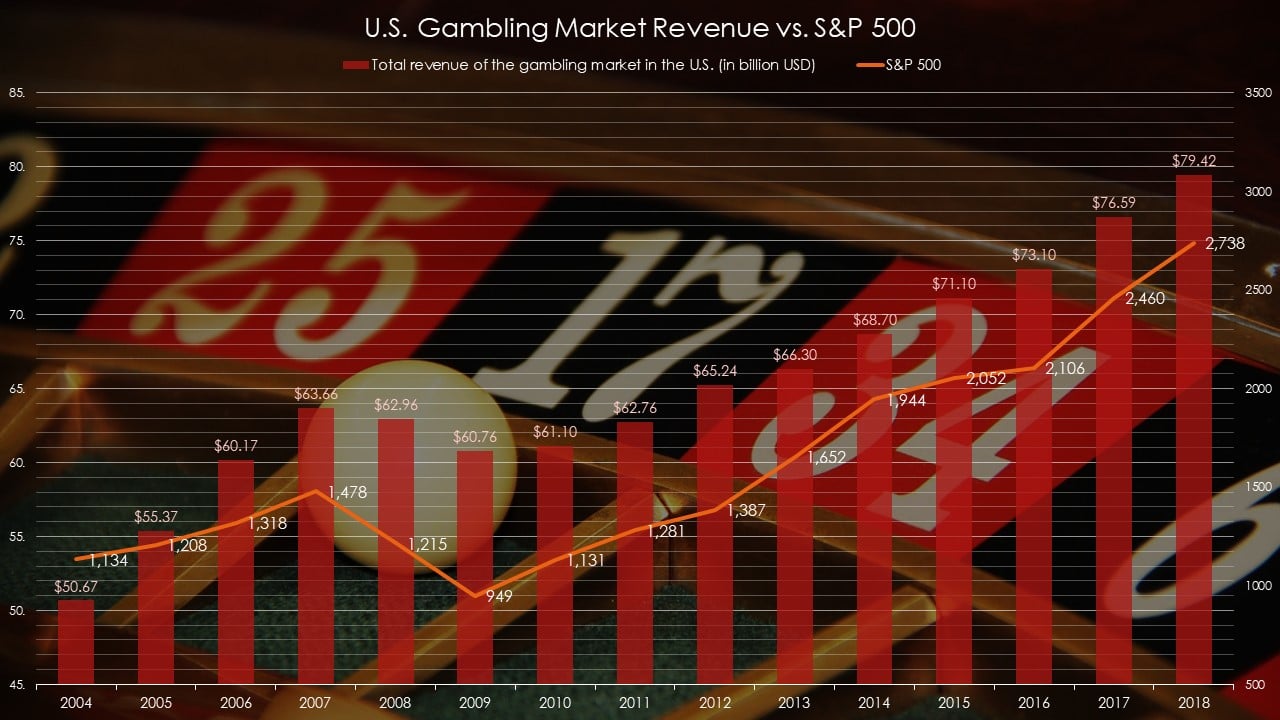

But how long can this strange dichotomy last? According to historical data, the answer is not long. Back in 2007, total revenue of the U.S. gambling market hit a peak of $63.66 billion. Later, the market crash and the subsequent Great Recession dropped sector revenue to a low of $60.76 billion in 2009. Following the market and economic recovery, revenue jumped to over $79 billion in 2018.

Click to Enlarge

Essentially, this trend mimics the S&P 500’s ebb and flow. In 2007, the benchmark index hit an annual average peak of 1,478 points in 2007 before dropping to 949 points in 2009. But from there, the index has been on a blistering run. In case you’re interested, the correlation coefficient between the two metrics is over 91%.

Basically, wherever the market goes, so too does gambling revenue. That’s a little different from online gambling and LCA stock. But I’d wager that if the S&P 500 takes a hit, so will LCA.

Wait for Further Clarity

In many ways, I’m glad that LCA stock jumped the way it did. At $12, there was vigorous debate about whether this was the right entry point or if shares could fall further. At the time of writing, the stock price is about $18. I’m more convinced that waiting for a discount is the smarter approach.

Don’t get me wrong — it’s not just about the price tag. Rather, the possibility of broader market weakness worries me. History has shown that gambling sentiment dies when the market does. Therefore, I see more incentive in waiting than taking a wild wager.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.