If you’re getting tired of this year’s market phenomenon — the special purpose acquisition company (SPAC) — you’re far from the only one. In fact, if it makes you feel any better, I’m tired of writing about it. But for the sake of thoroughness, we have to talk about CIIG Merger (NASDAQ:CIIC). Over the past few weeks, CIIC stock has enjoyed tremendous demand, suggesting greater things to come.

First, though, we should start with some background information. CIIC stock is what we might call a “two-fer” in 2020. That’s because it’s both a SPAC and an investment levered to electric vehicles (EVs), the other craze this year. Unsurprisingly, that combination has delivered some ridiculous profits for early-bird speculators and CIIG Merger is making good on the trend.

But this SPAC will not become a “garden variety” EV maker. Rather than competing in the saturated passenger vehicle segment, CIIG – which will merge with Arrival – focuses on the commercial EV space. This is also a highly competitive arena, largely because of the massive scale involved. But scale is exactly where this company has an advantage.

As InvestorPlace’s Matt McCall has mentioned, Arrival utilizes a unique asset-light “microfactory” approach that has sparked (and some would say justified) the intense demand for its acquisition company’s stock. McCall writes:

“The company — which is based in the U.K. — is hoping to build electric buses and vans and begin doing so in the fourth quarter of 2021. While some are critical of that start day, it’s much closer than many of its peers, assuming the company can execute.

“However, because of its microfactory approach, building and transporting these vehicles may be less of a costly chore than expected. Essentially, the company plans to be able to set up operations almost anywhere in the world. This will allow for regional operations and easier deployment.”

If this methodology is the real deal, that puts CIIG firmly in the driver’s seat as far as commercial EVs are concerned. But could we be hurtling into an unsustainable SPAC mania?

CIIC Stock Might Be the Victim of Poor Timing

On the surface, CIIC stock seems like the perfect EV investment. For instance, the underlying company developed a proprietary composite material. This enables CIIG to make pretty much any vehicle it wants, eliminating the complicated stamping and welding processes that cost money and time.

That’s a convincing point. More importantly, McCall also notes that the folks buying the stuff are convinced, noting that “one postal company has already put in an order for 10,000 electric delivery vans with an option for another 10,000 more […] Arrival has already secured $1.2 billion in initial orders.”

So, that’s about as good of an argument you need to buy CIIC, right? It would be, except for one little problem — the novel coronavirus.

With new daily infections rising to insane figures, as well as a shocking number of deaths, even those who have downplayed the pandemic are reconsidering. And, while I haven’t done a survey to gauge consumer sentiment, I don’t have to. I believe

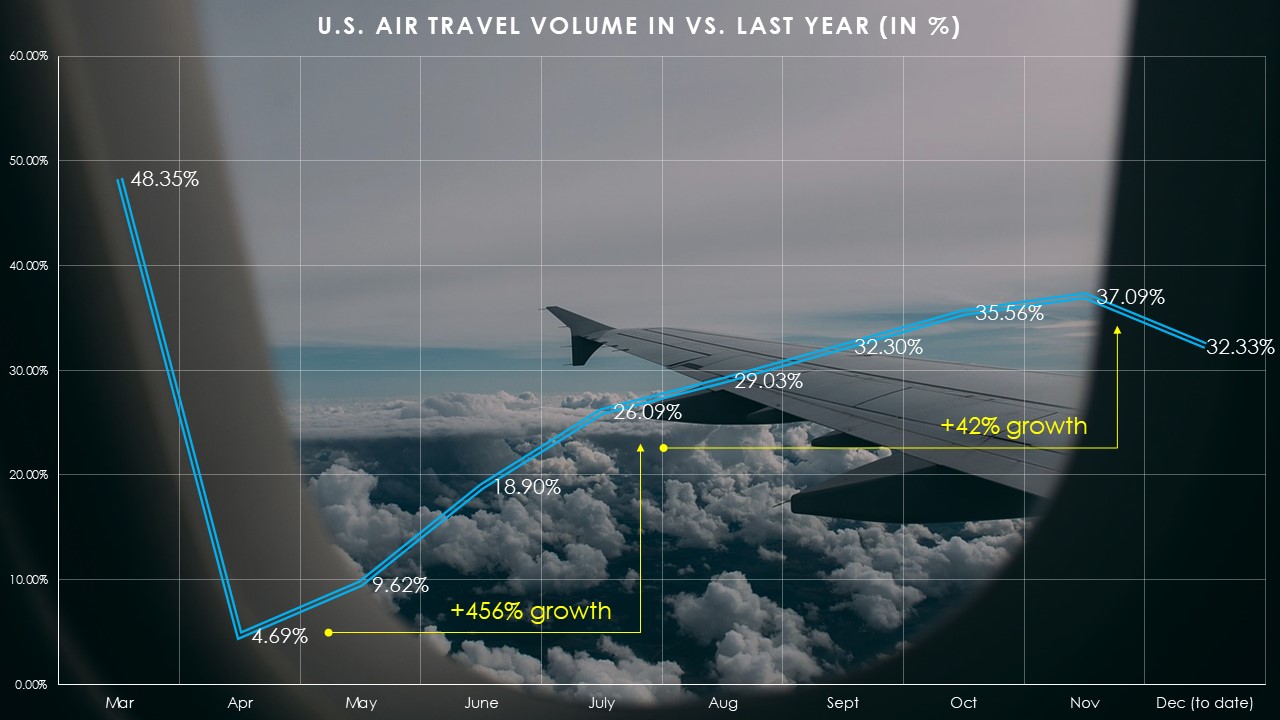

air passenger traffic volume tells you everything you need to know.

Click to Enlarge

During the worst of April’s initial wave, average passenger volume relative to last year was less than 5%. However, over the next few months, this rate picked up rapidly. But now growth has dramatically slowed down since July. In November, volume accounted for only 37% of last year’s volume. Plus, month-to-date information this December suggests that we’re moving in the wrong direction.

So — if you read between the lines — we can also assume people are also afraid to use public transportation. As further evidence, data from CouponFollow.com indicates that those traveling for the holidays prefer their personal vehicles over any other transportation method.

And this lends confirmation to what the Wall Street Journal has also reported — that many urban dwellers are buying their first cars for fear of mass transit. Logically, then, buying shares in a company focused heavily on mass transit is actually a tough proposition.

Waiting Could Be the Better Approach

Overall, CIIC stock really intrigues me. While we hear so many EV companies talk about their vehicles, Arrival’s investment thesis centers on its advanced manufacturing process and adaptability. In a sector saturated with competition, this pivotal advantage could be what separates it from the crowd.

Unfortunately, though, the timing couldn’t be worse in my opinion. With Covid-19 fears gripping the world and worsening, investors may find themselves losing their appetite for the stock. Nevertheless, I wouldn’t be opposed to taking a nibble at the present price. However, long-term believers may be able to get an even better price further down the line.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.