As of Dec. 16, PayPal (NASDAQ:PYPL) is up over 110% in the past one year. In fact, PayPal stock is up about 43% in the past six months and even 20% in the past month. The stock is on a tear, but I believe it could rise at least another 30% or so in the next year.

But why am I so bullish on PayPal?

I base that 30% on the company’s powerful free cash flow (FCF), which goes from strength to strength.

PayPal Stock’s Powerful Free Cash Flow

To start off, perhaps it’s best to go over what exactly free cash flow is.

FCF is taken from the company’s cash flow statement. It represents the result after deducting capital expenditure (capex) spending from the company’s cash flow from operations (CFFO). And CFFO has basically three components: net income, non-cash charges (including non-cash capital gains and depreciation and amortization) and changes in working capital (i.e., changes in current assets less current liabilities).

In the past year, PayPal had tremendous gains in its FCF. For example, in its latest Q3 earnings report, the company reported that FCF was $3.97 billion year-to-date (YTD), up 43% year-over-year (YOY) (Page 2).

Moreover, in the company’s buyside investor transcript, management indicated that they expect to make $5 billion in FCF in 2020. That would be nearly 30% greater than the FCF last year, which was roughly $3.85 billion.

That means FCF is growing from 30% to 43% on a YOY basis each quarter. This is very strong.

What’s the root cause? Well, the company’s underlying Total Payments Volume (TPV) is growing strong as well. I wrote about this in my last PYPL article on Oct. 1.

PayPal makes the majority of its revenue by charging fees on transaction-based TPV. In Q3, the company’s TPV grew 36% to $247 billion. Its take rate on the TPV — which is its net revenue — grew 25% to $5.46 billion. That implies that PYPL’s take rate is 2.21%. This was driven by its massive 55% YOY growth in net new active accounts (NNA).

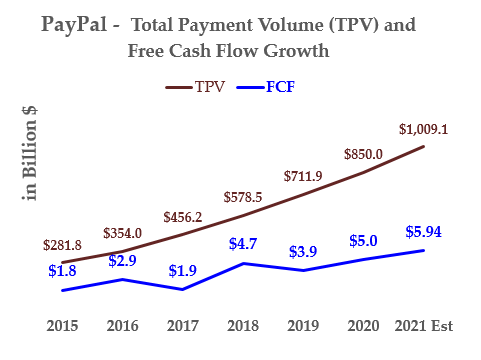

You can see the relationship between these factors in the following chart. The first one shows that as TPV rises, FCF goes up.

Click to Enlarge

Therefore, as long as its NNA is spiraling upward, its TPV will skyrocket, which will feed into net revenue and FCF. Of course, this is a lot of terminology. But it’s the basics of PayPal’s business model and it shows why the company’s FCF will keep growing from strength to strength.

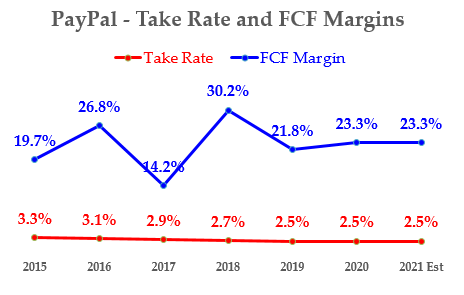

The model can also be seen in the second chart and the associated table that I have included below.

For example, the next chart at the right shows that as the take rate on the company’s TPV hovers around 2.5% over the next year, its FCF margin will be about 23% or so.

Click to Enlarge

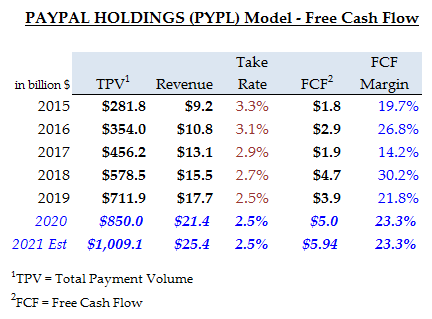

This is also seen in the next table, which places all five of these variables together and shows how they correlate with one another.

Essentially, they form a simplified model of how the business behind PayPal stock works, allowing anyone to estimate its future FCF.

Click to Enlarge

PayPal’s Valuation

So, now let’s assume that PayPal’s FCF grows 30% on average over the next three years. That would make 120% times its $5 billion in FCF forecast this year and put free cash flow at about $11 billion.

Today, PayPal stock has a FCF yield of 1.9%. Therefore, in three years — assuming the company makes $11 billion in FCF — its market value would be worth over $578 billion. That is derived by dividing $11 billion by 1.9%.

This means that PYPL will be worth 103% more than today. But we can’t use this number. For one, there are a lot of risks that could stop this from happening. So, the best way to handicap that figure is to take a discount rate.

At a 15% discount rate — which represents the minimum return on investment (ROI) that most investors want to see annually — the discount factor is 65.75%. Therefore, the real return will be 68%. This is the result of taking 68.3% of the 103% expected return.

And that means the stock has a present value target price of $387.42. That is the result of multiplying 1.68 times today’s price of $230.20 (Dec. 16).

So, you can see that — based on its powerful free cash flow growth — PayPal stock is worth $387.42 today, or a potential 68% gain.

What To Do With PayPal Stock

As readers of my InvestorPlace articles already well know, I like to put together simple models like this in order to derive a stock’s value. You should always have this kind of simple model in your head when thinking about buying a stock.

And I am not the only one that likes PayPal. For example, TipRanks.com reports that 31 analysts have an average price target of $227 per share on the stock. That represents a 6% increase over the price on Dec. 11.

But remember, an average means there are higher price targets than the middle or mean. For example, the highest estimate on TipRanks.com is $290 per share.

In other words, the range from the mean target price — what analysts call the standard deviation — is quite large. Another example from Yahoo! Finance shows that the mean price target of 41 analysts is $226.32 per share. But the range is quite wide. On the upside of the range, the highest price target is $312 per share.

The bottom line? It’s not unreasonable to use my simple model of PayPal stock to believe that it is worth 68% more to $387.42.

On the date of publication, Mark R. Hake did not have (either directly or indirectly) any positions in any of the securities mentioned in this article.

Mark Hake runs the Total Yield Value Guide which you can review here.