PayPal Holdings (NASDAQ:PYPL) has been on a tear this past year, even after taking a small hit this past month. PayPal stock is likely to continue to do well as it is a free cash flow (FCF) powerhouse, going from strength to strength.

In the past year, PayPal stock has risen 80% and is up about 73% year-to-date. This is remarkable given this it has a massive $225 billion market capitalization and does not pay a dividend.

Moreover, there is every reason to believe that PayPal stock will continue to do extremely well over the next several years. This is because the company has a very powerful, consistent, and fast-growing FCF business.

PayPal’s Powerful FCF

Essentially it makes fees on money transactions which it calls “Total Payment Volume” (TPV). Last quarter it made $5.26 billion on TPV of $222 billion. Therefore, its “take rate” (my term) is about 2.37% (i.e., $5.26 billion divided by $222 billion).

So you can see that the business is very simple. As transactions increase in both velocity and value, PayPal’s “take” increases. And this is exactly what happened in Q2.

Everyone got stuck home and they conducted most of their business online. A lot more people started paying by using PayPal for their transactions. Moreover, undoubtedly PayPal picked up a ton of new customers that it wouldn’t have done so otherwise.

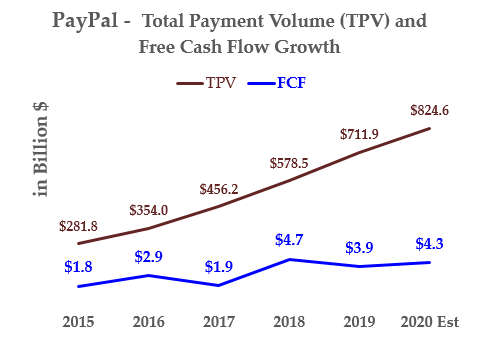

Total Payment Volume and Free Cash Flow

These customers are purchasing more online. This spills over to PayPal’s benefit. That is why its FCF has been growing.

Click to Enlarge

You can see this in the chart I made on the right. As TPV rises each year, FCF tends to rise as well.

For example, since 2017 the total payment volume has almost doubled to an estimated $825 billion this year.

And FCF will have more than doubled over the same period, from $1.9 billion in 2017 to an estimated $4.3 billion this year. In fact, as of the half-year to June, total payment volume has already grown 23.5% to $413 billion.

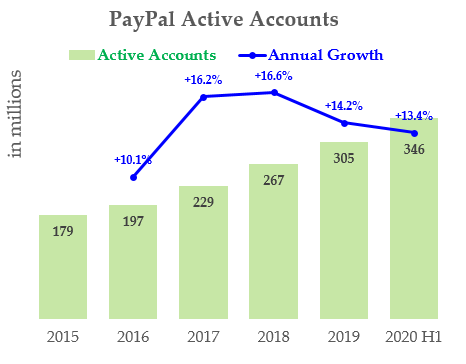

Click to Enlarge

The second chart on the right shows that PayPal’s active accounts are on a tear. In the past 4.5 years from 2015 to mid-2020, the number has grown from 179 million to 346 million.

That represents an increase of 93.3% over 4.5 years, or 15.8% annually, on a compounded basis.

Therefore, no wonder FCF is set to continue to grow. As more people buy things online and use PayPal to pay for them, the company’s FCF will rise.

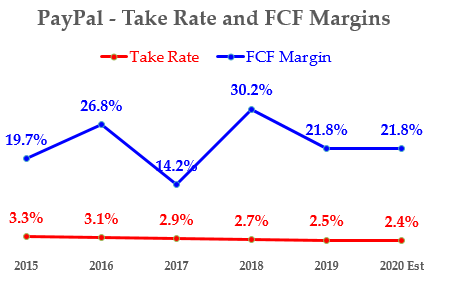

One thing to note. The take rate has been falling. Net revenue in 2015 was $9.2 billion on $282 billion in TPV. That represents a take rate of 3.3%.

Click to Enlarge

But in the first half of 2020 net revenue was $9.9 billion on TPV of $413 billion. That was a take rate of just 2.4%.

Nevertheless, its FCF margins have stayed steady. You can see this on the chart.

As the number of transactions increases that PayPal is involved in, competitive pressures have forced them to lower overall transaction fees.

What to Do With PayPal Stock

PayPal stock is not cheap. I am not arguing that. But I do believe that its FCF will continue forcing the stock higher. One way you can see is its FCF yield.

For example, PayPal has a $225 billion market capitalization but it produces about $4.3 billion in FCF. That means that its FCF yield is 1.9% (i.e., $4.3 billion divided by $225 billion). That is not out of line with other mega-cap stocks.

For example, Visa (NYSE:V) has a $420 billion market cap and produced $11.57 billion in FCF over the last 12 months. That gives it a 2.75% FCF yield.

But American Express (NYSE:AXP) made $563 million in FCF in the last 12 months on a market cap of $77.5 billion. That is a 0.73% FCF yield.

PayPal stands in the middle of these two consumer payments peers at a 1.9% FCF yield.

My point is simple. The multiple for PayPal stock may not increase much. But the rise in TPV volume and FCF over the next several years as e-commerce grows will continue to push up PayPal stock.

On the date of publication, Mark R. Hake did not have (either directly or indirectly) any positions in any of the securities mentioned in this article.

Mark Hake runs the Total Yield Value Guide which you can review here.