Pinterest (NYSE:PINS) can’t sustain its sky-high valuation. That was the thesis of my Nov. 19 article on PINS stock and I wanted to follow up. This time I will try to make my reasoning much simpler. My previous article on Pinterest’s valuation was a little math-heavy (although all my articles tend to be).

By the way, if you are going to invest money in a highly valued stock, you need to know the math of valuation. You should also always have what professional gamblers call “expected value” (EV) or what most analysts call a “target price.”

Basic Thesis Why Pinterest Is Overvalued

In a nutshell, here is the thesis on why PINS stock is too high. Pinterest trades for more than twice the price-to-sales multiple of Facebook (NASDAQ:FB). But Facebook makes twice the revenue per user than Pinterest. Its ARPU (average revenue per user) is 100% higher than Pinterest’s. In other words, PINS stock needs to fall, or its ARPU needs to rise.

This is not an unrealistic possibility. For example, last quarter Facebook’s revenue grew 22% year-over-year.

But Pinterest’s revenue growth was 58%. So over a period of five to 10 years, it is possible that Pinterest’s ARPU could catch up to Facebook’s. Maybe. Maybe not, though, since it is also highly likely that Pinterest’s revenue growth will slow just as Facebook’s slowed.

So you see the quandary that investors in PINS stock are in right now. Pinterest’s ARPU can rise faster than Facebook’s ARPU only if its relative revenue growth rate per user is higher than Facebook’s.

That is likely going to be hard to achieve. Let’s look at my thesis more carefully.

Pinterest’s Valuation

In my last article, I argued that PINS stock was worth no more than $40.76. I still believe that is the case. Here is a simpler way to understand this.

First, Pinterest calculated its Q3 ARPU at $1.03 for the quarter. That means on a full-year basis (run-rate) it will make $4.12 per average user.

By contrast, Facebook said its ad revenue was

$21.221 billion for the quarter. It no longer calculates ARPU. However, Facebook’s MAU (monthly average users) was 2.74 billion as of September. Therefore, roughly speaking, its quarterly ARPU was $7.45 in Q3. Annually, that works out to a run-rate of $29.80 per user.

So Pinterest makes $4.12, Facebook makes $29.80 annually per user. Facebook’s revenue productivity is seven times better than Pinterest.

So why does PINS stock have a 2021 price-to-sales multiple of 18.6 times? FB stock’s multiple is 7.55 times. In other words, PINS stock is likely overvalued by a significant margin.

Click to Enlarge

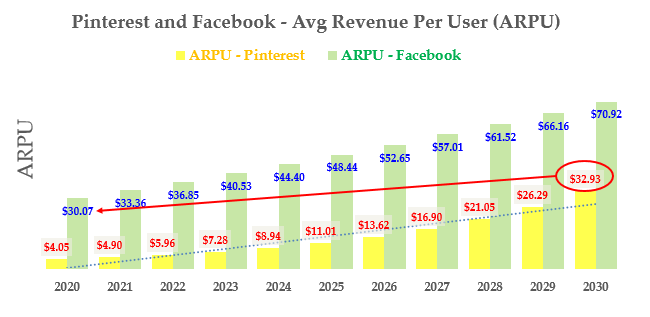

In fact, based on my estimates of ARPU growth rates, Pinterest will not reach Facebook’s level of ARPU for about 10 years.

You can see this in the table at the right. It shows that sometime between 2029 and 2030 Pinterest will have an ARPU of more than $30. But that is exactly where Facebook will be in 2020.

This is 8.1 times growth over 10 years, and it implies an average annual growth rate of 23.3%.

What to Do With Pinterest Stock

Pinterest has a market cap of $43.7 billion. But the implied market cap in 2030 will be $416.9 billion. This leads to an estimated share price of $595.63 per share in 10 years, or 8.42 times in 10 years. (This is based on 700 million shares outstanding, 1,677 MAUs in 10 years, and a Facebook price-to-sales ratio of 7.55 times.)

That represents an annual gain of 23.7%, or roughly similar to the ARPU growth rate. This implies that Pinterest is basically fairly valued right now.

On the other hand, if we take the ARPU of $32.90 in 10 years (see chart above) and discount it to the present at 20%, it is worth $5.31. But now we have to use the Facebook valuation parameters.

For example, $5.31 times MAUs of 442 million times Facebook’s multiple of 7.55 equals a market cap of $17.7 billion. That is only 40.5% of Pinterest’s existing $43.7 billion market cap. This suggests PINS stock is way overvalued.

So that is the quandary most investors are in about Pinterest. They can predict the growth, but the implied valuation is somewhere between 100% overvalued and fairly valued.

I suspect that PINS stock will likely tread water for a while before it moves up again, based on this quandary.

On the date of publication, Mark R. Hake did not have (either directly or indirectly) any positions in any of the securities mentioned in this article.

Mark Hake runs the Total Yield Value Guide which you can review here.