Having analyzed the electric vehicle phenomenon for the last several months, I’m coming to the conclusion that Switchback Energy Acquisition (NYSE:SBE), the special purpose acquisition company that aims to merge with EV charging station specialist ChargePoint, is an “on-the-cusp investment.” By that, I mean SBE stock is on the cusp of greatness. But on the flipside, it’s also on the cusp of a correction.

Before you barrage me with hate mail, let me pay my obligatory homage to electric vehicles. They are awesome. So awesome that they will change the world. When you look at EVs, there are zero setbacks associated with them. Indeed, they are superior to clunky, dirty cars based on the tired and anachronistic internal combustion engine. Happy?

Now, I’m being a little bit facetious. However, if you listen to the user reviews of popular EV manufacturers like Tesla (NASDAQ:TSLA), my description above isn’t too far off from this community’s commonly distributed opinions. In fact, EVs are brilliantly convenient, so long as you can “holistically” afford one.

According to information from the Office of Energy Efficiency & Renewable Energy, most plug-in EV drivers “do more than 80% of their charging at home. Charging in a single-family home, usually in a garage, allows you to take advantage of low, stable residential electricity rates.” But if you’re in the lower-to-middle income bracket? Assuming you can even afford an EV, you may not have access to personal infrastructure.

Ah, but this is where the bullish narrative for SBE stock arrives front and center stage! Thanks to ChargePoint’s comprehensive charging station portfolio – which covers high-volume locales such as business plazas and residential complexes – the company can fill a vast opportunity gap.

Therefore, the paper argument for SBE stock makes much sense. But the broader realities of EVs and its proposed infrastructure rollout is a concern you don’t want to ignore.

Multiple Headwinds Blowing Against SBE Stock

With the administration of President Joe Biden, it seems to add the political cherry on top for EVs and by logical deduction, SBE stock. More people recognize climate change and going electric can help mitigate environmental damage.

Certainly, if stocks gained on eco-friendly morals, I’d be hard-pressed to even conjure up a cautious take on SBE stock. But usually, a different kind of green has always been the bane of the go-green movement. Yes, a

majority of consumers will pay more for sustainable products but goodness me, there’s a limit to this ship. From my perspective, I see three main factors that could negatively impact ChargePoint.

- Combustion cars are no slouch.

- Public charging is surprisingly complicated.

- Charging stations are “derivative” businesses.

First, while we celebrate the innovation and profound efficiencies of EVs, we can’t forget that combustion cars are also improving. It would be disingenuous not to acknowledge that modern cars are more fuel efficient and less polluting than prior generational examples.

Also, while EV battery costs are declining heavily, combustion cars have superior economies of scale. Currently, the world has better use of “analog” vehicles than electric vehicles. That won’t change until infrastructural access changes dramatically.

This segues into my second point: ChargePoint on paper promotes solutions toward said access problem. However, the process of charging can be complicated because there’s no universal standardization of charging station protocols.

On the residential front, not every complex has the space to incorporate charging-dedicated parking spots. Therefore, all parking spots must have access to Level 2 chargers, which then brings up economic efficiency issues since not everyone will drive an EV.

Third, charging stations are derivative businesses in that they derive value from broader EV integration. But if that integration doesn’t occur as planned, it doesn’t matter what ChargePoint does. It’s down at the bottom of the EV supply chain.

Don’t Ignore SPAC Fever But Be Careful

Having said all that, the above points can easily be muted at least in the near term if SPAC fevers gives another bullish round for SBE stock. Obviously, retail activist investors are having their day and they can turn their attention toward noble pursuits – after they’re done killing billionaires’ portfolios – such as green energy infrastructure.

That’s why I’m not suggesting that investors should short ChargePoint. With the present environment, all shorting ideas are treacherous.

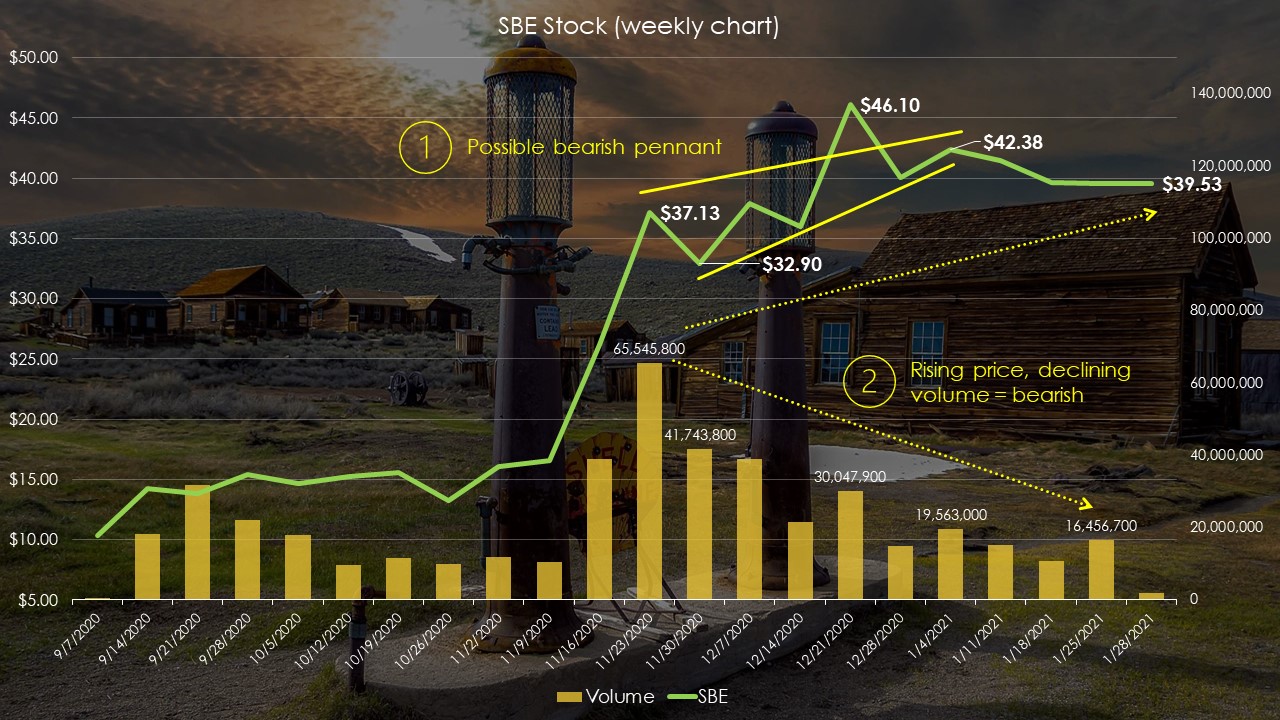

Click to Enlarge

However, I also can’t ignore that the technical chart for SBE stock is not encouraging. It looks to me that between November and December, ChargePoint charted a bearish pennant formation. Additional confirmation comes from the declining volume, rising price dynamic. According to the technical discipline, this is a bearish setup.

Again, I’m not suggesting you should short SBE stock. But if you’re profitable, you may want to exit out. On the bright side, you can probably pickup shares on a discount soon.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.