Last year, special purpose acquisition companies listings triggered a euphoria of investors seeking easy gains. Workhorse Group (NASDAQ:WKHS) is one of the early companies that took the SPAC route. By bypassing the initial public offering format of raising cash, WKHS stock rose from the $1.32 low to its current price at more than $34.

Lately, shares in the auto manufacturer got stuck in a trading range. Investors are waiting on a few catalysts before buying the stock again.

WKHS Stock Missing a Catalyst

For months, investors waited for Workhorse to announce a purchase order from the U.S. Postal Service. When that did not come, the stock fell to as low as $15 in the last quarter. Smaller orders re-ignited some buying interest but not enough.

On Jan. 4, Workhorse announced a purchase order from Pride Group Enterprises. The customer will buy 6,320 C-Series all-electric delivery vehicles. Hitachi Capital America will provide the inventory financing. That means the loan will be collateralized by the inventory in the purchasing. This is a common financing method for companies that don’t have easy access to loans.

Workhorse will start delivering the product this July through 2026.

In November, Workhorse received a purchase order from Prichard Companies for 500 C-1000 delivery vehicles. The deal, worth around $40 million, raises awareness for its all-electric truck fleet. For example, the lightweight design and low floors have advantages over conventional trucks. This increases the volume available for carrying packages in the cargo area.

Investors may only imagine how many unit orders Workhorse would get if it won a deal with a government entity like the Postal Service and its $6.1 billion contract.

Fair Value

Given the limited sales at this time, investors cannot use current consolidated financial statements to forecast the stock’s fair value. It posted net sales of $565,000, while the cost of sales was $2.8 million. After losing $84.1 million, Workhorse needs a deal worth at least $100 million.

Optimists may assume that the company will win supply deals worth at least $70 million in the fiscal year 2021. In this scenario, apply a pessimistic discount rate of 16%. This would suggest that Workhorse stock has a fair value of $29:

| Metrics | Range | Conclusion |

| Discount Rate | 17% – 15% | 16% |

| Perpetuity Growth Rate | Zero – 0.5% | Zero |

| Fair Value | $29.02 – $29.46 | $29.24 |

Model courtesy of finbox

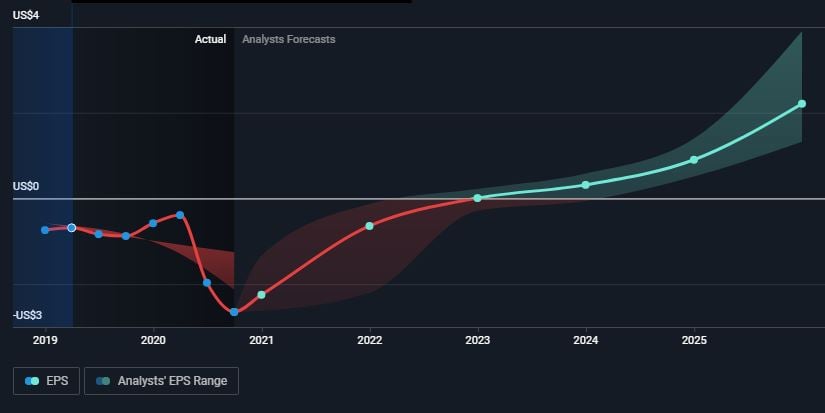

In another scenario, consider Workhorse posting revenue of $2 billion in 2025. If it also posts positive earnings starting in 2022, the stock would have a fair value of $27 (per simplywall.st).

Click to Enlarge

In the chart, Workhorse posts the maximum loss in the last quarter. After winning several purchase orders, losses shrink.

Risks

Speculators are banking on this technology automotive company to supply EVs to the delivery sector. Growing popularity in battery-electric vehicles could create a shortage of raw materials. This would increase the product cost and hurt margins. Furthermore, competitors could enter the market to compete with Workhorse. This would put pressure on the company’s selling prices, driving out profits.

Any of those risks would hurt profitability. And any slowdown in revenue growth in the next few years would hurt investor confidence. Shareholders would sell shares, weakening the stock price.

The financial statements above are troubling. Between 2015 and 2019, the company’s revenue disappeared. Net income turned negative, worsening by 2019. The average share dilution also hurt investors over that period.

Your Takeaway

The market is betting heavily for and against WKHS stock. At a short float of 31%, the bears stand to gain if the company fails to solidify a deal with a major customer this year. The stock could move in either direction next. Investors have no way of knowing which way that will be.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article.