Social Capital Hedosophia V (NYSE:IPOE), a SPAC (special purpose acquisition corp.), should close its merger with Social Finance (SOFI) soon.

The deal was announced on Jan.7, and at the time, the firm indicated it would close by the end of first quarter of 2021. Overall, though, IPOE stock (to be renamed Social Finance) looks undervalued as it stands using my calculations.

In fact, the merged company will be worth over 30% more or $23.91 per share — compared to its price of $18.27, as of March 22. And in this article, I will show you how came up with that calculation.

What IPOE (Sofi) Is Worth Post Merger

Sofi just released its 2020 earnings results. The financial technology company, which bills itself as a leading next-generation financial services platform, produced better revenue and adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) than forecast. That said, revenue for 2020 came in at $621.2 million, whereas its slide presentation forecast $621 million.

Additionally, its adjusted EBITDA performance for 2020 was even better. It originally forecast a loss of $66 million, but the actual results were a loss of just $44 million. Also, the company stands by its forecast of positive EBITDA profits in 2021.

Click to Enlarge

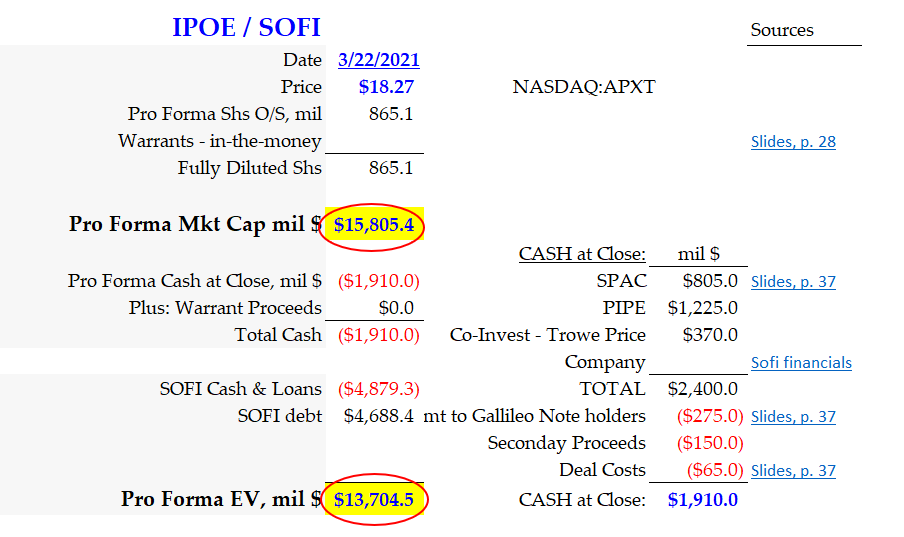

As you can see from the table on the right, the proforma market cap for IPOE, as of March 22 is $15.8 billion.

In addition, the pro forma Enterprise Value (EV) is $13.7 billion. This is calculated by taking the sources and uses of cash figures from the slide presentation.

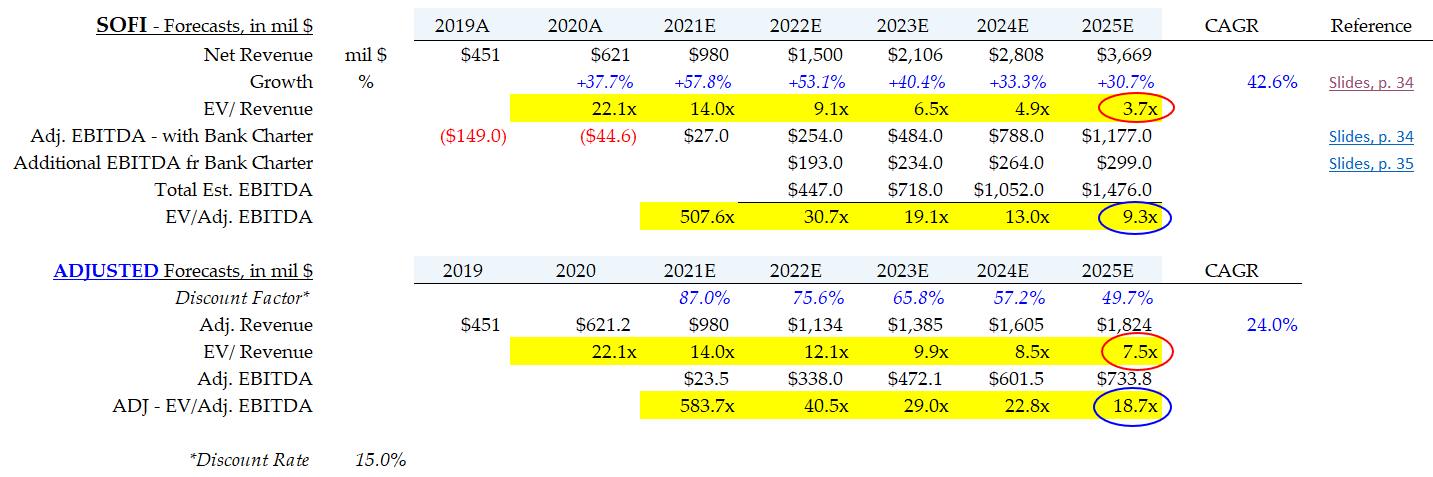

We use these numbers to estimate the EV-to-EBITDA metrics and valuation for IPOE stock (Sofi). This uses the forecast sales numbers, both adjusted (see above) and unadjusted.

The second table below the first shows an adjusted EBITDA forecast. This adjusts the forecasts out to 2025 for risks and the time value of money. I use a 15% discount rate.

Click to Enlarge

This works out to a factor of 49% in the fifth year 2025, effectively lowering the adj. EBITDA by that amount. The results are this: by 2025 the EV-to-EBITDA multiple is a reasonable 9.3 times, but after adjusting it for risk and time value of money, the multiple rises to 18.7 times. Note that this also includes the effect of Sofi obtaining a banking license, which will lower its interest and borrowing costs.

Many of Sofi’s “neobank” peers are not public yet. Slide 17 of the IPOE presentation shows that 296 neobanks have emerged in the last 10 years, mostly in the last 5 years. The presentations from both IPOE and Sofi do not include any peer comp valuations.

Click to Enlarge

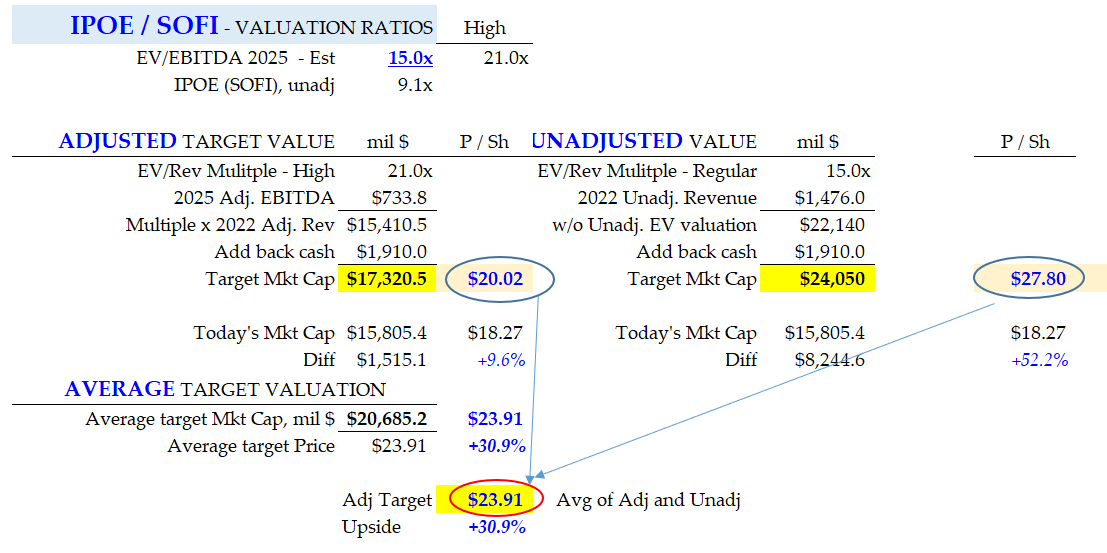

However, it seems to stand to reason that 9 times 2025 EV-to-EBITDA is too low. A more normal valuation would be at least 15, and possibly as high as 40% higher or 21 times.

The table at the right shows that at these ratios IPOE stock (SOFI) is worth at least 30% more. This is taken as an average of the adjusted and unadjusted EBITDA numbers.

The table shows that the average value ranges from $20.02 to $27.870, or an average of $23.91. this represents a value about 30% higher than the March 22 price.

What To Do With IPOE Stock

This analysis shows that there is still good upside left in IPOE stock (SOFI). I believe that once the company merges and collects the $1.9 billion in new cash at the close, the stock will break higher. I suspect that the close will happen daily soon, although there is no definite date set yet.

Therefore, this looks like a reasonably good investment. I suspect that its valuation will actually spur a new set of neobanks, like Bluevine, Chime, Monzo, and Robinhood to go public. In fact, CNBC reported recently that Robinhood has filed documents with the SEC to go public soon. It is not clear yet if it will be an IPO or a direct listing. Page 38 of the Social Capital Hedosophia presentation shows 9 other private neobanks with which Sofi competes.

Look to make money with IPOE stock (SOFI) once it closes its SPAC merger, as it appears to be worth $23.91 or 30% more than the price on March 22. It will also set a valuation yardstick vs. other neobanks that emerge on the public trading scene.

On the date of publication, Mark R. Hake did not hold a long or short position in any of the securities in this article.

Mark Hake writes about personal finance on mrhake.medium.com and runs the Total Yield Value Guide which you can review here.