Earlier this week, we learned that March’s U.S. consumer prices rose for the fourth straight month. Meanwhile, the pace of inflation notched its highest level in two and a half years.

Even though inflation is back on the radar, we’re being told that, on the whole, it’s mild. The Fed says any uptick we see will be transitory.

InvestorPlace CEO Brian Hunt disagrees. And in this essay, Brian reveals what he thinks is really going on with inflation … and points toward how you can help safeguard your wealth in the years to come.

Brian asked me to help him gather data in order to put together a proprietary price index for high earners for this essay. I’m always happy to help Brian out — and I’m even happier to give him another spot to run his intriguing thoughts.

I’ll let him take it from here.

America’s Top Stock Picker Reveals Next Big Winner (Free)

Don’t Let the Fed Tell You Inflation Isn’t a Problem

By Brian Hunt, InvestorPlace CEO

In the wake of the financial crisis of 2007-2008, the U.S. government launched one of the largest stimulus packages in our country’s history.

When it was all said and done, the government spent a total of $2.8 trillion on stimulus and housing crisis relief … all in an effort to prop up industries, save jobs and get people spending again.

That huge sum now seems small when we talk about government stimulus related to the COVID-19 pandemic. As I write this in April 2021, Uncle Sam is on the hook for at least $5 trillion in spending. Trillions more will likely follow. It’s the largest spending program relative to the size of our economy since World War II.

America’s Top Stock Picker Reveals Next 1,000% Winner (Free)

As these spending programs rolled out over the past decade, scores of financial experts predicted the return of painful inflation.

After all, as the supply of money increases, so should prices, right?

Yet, conventional inflation has failed to materialize in the United States. According to the government’s consumer price index (CPI) statistics, inflation has increased at around 1.77% per year since 2010, which is substantially lower than the long-term U.S. average of 3.1% per year.

But are we looking at the right numbers?

It’s easy to make the case that we are not. At least the wealthy aren’t.

How the Wealthy Are Different

History shows wealthy people spend their earnings differently than those with lower incomes. For example, wealthy people tend to spend a smaller percentage of their income on gasoline than low-income Americans do. The opposite is true for education (lower income earners spend less on it).

The wealthy also spend far more on financial services — like insurance and pensions — than low-income earners. The wealthy are much more likely to use their earnings to accumulate investments in real estate and businesses (often purchased in the form of stocks).

When you take the differences in financial habits into account, a different “cost of living” picture emerges than the one people paint while quoting the government’s sub-2% annual consumer price inflation figures.

This picture shows inflation is here. It shows that many supposed “wealthy” people are running as fast as they can just to stay in place.

We know the wealthy often own businesses and employ many people. The price of the business world’s building blocks has skyrocketed. The price of corporate assets — as measured by the benchmark S&P 500 index — has climbed 123% since 2014. This is another way of saying $1 earmarked for the purchase of corporate assets in 2014 is worth about half as much today.

Or, take another area of major spending for the wealthy: education.

Over the past decade, the cost of a public college education climbed 29.8%. The cost of a private college education climbed 25%. This is another way of saying one dollar earmarked for education is worth 25% to 30% less than it was in 2010.

Then you have the soaring cost of medical care. After all, what good is money if you’re not healthy enough to enjoy it? The cost of medical care (for people at all income levels) has soared 25% since 2012. That’s more devaluation of the money you socked away eight years ago.

And then you have homes. According to the S&P CoreLogic Case-Shiller U.S. National Home Price Index, home prices in America have climbed 58% since 2013. Yet more devaluation of your savings, manifested in higher prices.

America to END China’s Monopoly on Rare Earth Elements?!?

That’s not to say we should feel sorry for the wealthy. Of course, it’s better to be wealthy than not. But let’s not kid ourselves about inflation, and how it affects people with $250,000 to $5 million in assets.

These people help form the backbone of our economy. These people are not taking private jets to watch the Super Bowl in luxury suites. They are small-business owners, dentists, doctors, teachers, firefighters, engineers, contractors, sales reps, pilots and business managers.

They have studied, worked hard and saved — and the cost to live the life they want is soaring. Tell two middle- to upper-class parents working their tails off to provide their three kids with a good start in life that their cost of living is rising at just 1.77% a year. They will either laugh or curse you out of the room.

Thanks to the ever increasing costs of housing, education, medical care and business assets, many families with $250,000 to $5 million in assets — the supposed “wealthy” — are working harder than ever to maintain their standard of living.

Since 2010, the Federal Reserve’s balance sheet (aka the money supply) has exploded by more than 200%. However, this huge increase in the money supply hasn’t caused conventional inflation because of a lack of something called “monetary velocity.” The Fed is getting money into banks, but all that money isn’t getting into the hands of regular people.

Instead, it has found its way into stocks, homes, the price of college and many other things wealthy people tend to buy. Inflation for low-income earners may be mild, but for higher earners it is raging.

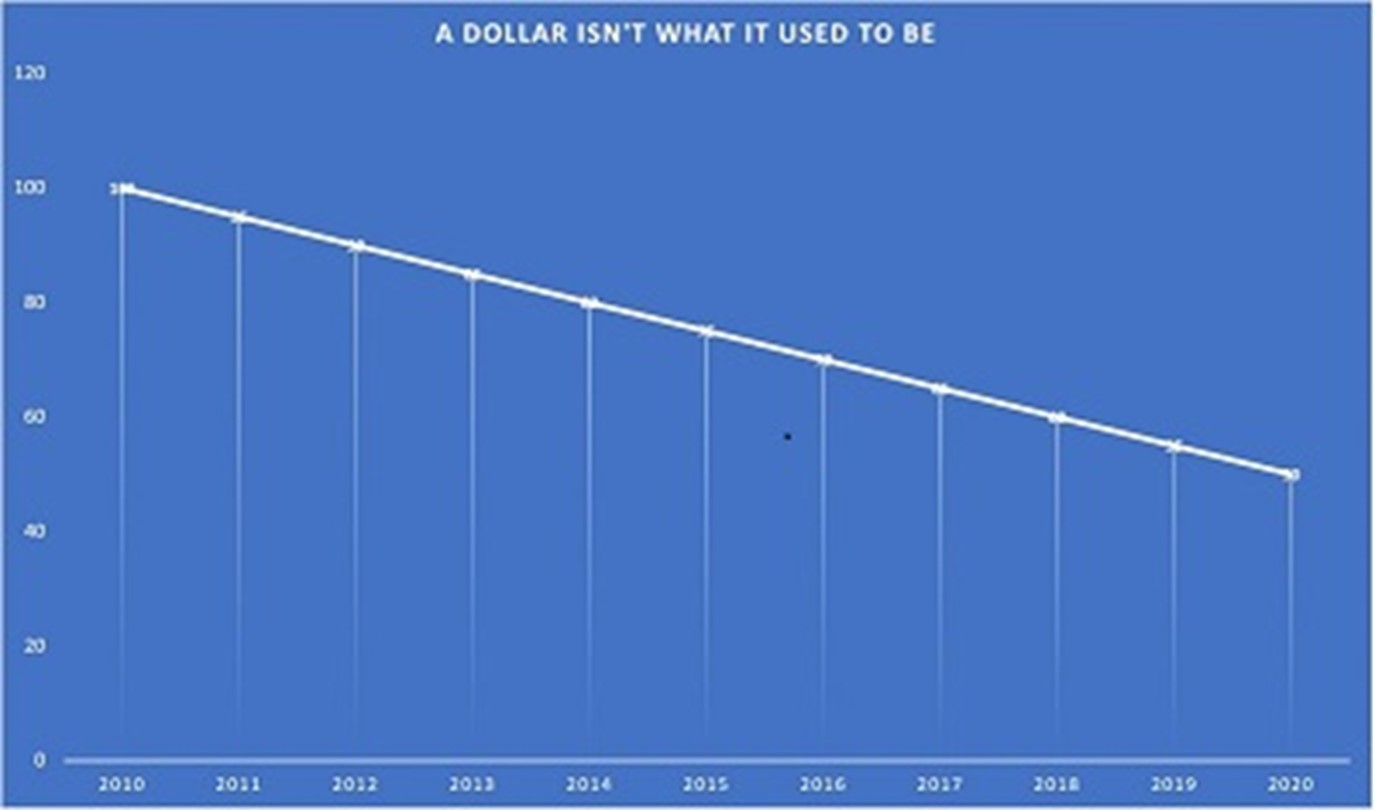

To get an idea of how the cost of living is rising for relatively wealthy people, I worked with Eric and others at InvestorPlace to construct a proprietary price index for high earners. We placed heavy weightings on homes, tuition, medical care, food, transportation, and — this is key — business assets.

Proving What We Already Know

The government’s CPI calculations do not include businesses asset costs. It focuses on consumer prices. But we believe a useful measure of inflation for the relatively wealthy must include the price of the building blocks of capitalism. After all, starting, building, and/or owning businesses is how most people get and stay wealthy in the first place.

Our rate of “inflation for the wealthy” (graphed below) shows their earnings and savings are losing purchasing power at a rate of 5% per year.

When I show this chart to people, I often see a powerful thought register on their faces. It graphically represents a strong feeling many of us have:

Counter to what our government says, the price of living the life we want is soaring … and the value of our money is going down.

Losing your purchasing power at a rate of 5% per year makes it so every $1 of savings is worth just $0.66 after eight years (a 33.6% loss in purchasing power).

The next time you see a chart of stocks, homes or tuition going from the lower left to the upper right, keep in mind that chart also shows the value of your earnings and savings going down. As the price of something increases, your ability to buy a unit of that something decreases.

The proponents of enormous government spending, borrowing and money printing like to point out that the significant outlays of the past decade are not producing currency debasement, also known as inflation. The soaring prices of the things many of us buy in volume say otherwise.

If there’s one thing both political parties can agree on, it’s that their reelection chances are improved by a firm commitment to more government spending, more borrowing and more money printing. And because the ideas in this essay don’t get traction in the mainstream press, the widespread belief that inflation is not a problem gives Washington political cover to spend without serious consequences.

Given this outlook, the investment implications for the relatively wealthy are clear: Avoid holding cash over the long term. A large sum of cash held for years in the bank will prove to be a melting ice cube.

Instead of holding cash over the long term, we recommend owning shares of businesses (public or private) and real estate. We expect them to hold their value over the next decade just as they did over the previous one. We expect cryptocurrencies like Bitcoin (CCC:BTC-USD) will continue to be a good defense against currency debasement. And while gold hasn’t done much in the past year, we still like its prospects as a hedge against currency debasement. Call us old fashioned.

The trend driving the dollar’s devaluation is unlikely to stop. The value of our money is going down. The relatively wealthy would do well to act on the facts in this essay, which put a point on what we already intuitively know.

Regards,

Brian Hunt

CEO, InvestorPlace

P.S. Hundreds of thousands of folks saw Eric’s “Technochasm” viral video from earlier this year.

Well, the whole world has changed since then … and Eric is back to talk about the Technochasm, the biggest megatrend in investing, in ways he couldn’t before … and discuss opportunities for even bigger market gains … the kind to keep you from falling behind. And Eric is bringing along investing legend Louis Navellier to join him on camera for the first time ever.

Click here to check out their conversation – and to get their No. 1 stock pick right now.

On the date of publication, Eric Fry did not own either directly or indirectly any positions in the securities mentioned in this article.

Eric Fry is an award-winning stock picker with numerous “10-bagger” calls —in good markets AND bad. How? By finding potent global megatrends… before they take off. In fact, Eric has recommended 41 different 1,000%+ stock market winners in his career. Plus, he beat 650 of the world’s most famous investors (including Bill Ackman and David Einhorn) in a contest. And today he’s revealing his next potential 1,000% winner for free, right here.