When Zomedica (NYSE:ZOM) “double-peaked” at above $2.50 between February and March, speculators recently bet on the downtrend to end. ZOM stock may have bottomed at below a dollar in the last week.

To know for sure if the selling pressure ended, traders first need to ask why the stock fell in the first place. Readers should also ask what the fundamentals changes are that would justify a rebound in shares.

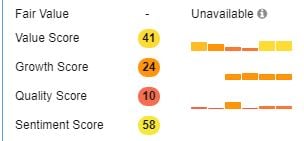

Why the ZOM Stock Rally Faded

On Feb. 8, Zomedica increased its bought deal offering. At $1.90 a share at the time on 91.32 million shares, the company raised around $173.5 million. Though selling shares typically hurts shareholders, markets interpreted the strong demand as a bullish sign.

The veterinary health firm, which wants to create point-of-care diagnostics products for dogs and cats, needs a cash raise. According to the press release, the company “intends to use the net proceeds from the offering for the continued development of its diagnostic platforms.” This would include any related milestone payments connected to its licensing and collaboration agreements.

H.C. Wainwright acted as the sole book-running manager for the stock sale. The analyst who issued a $1.20 price target also works at that firm. Investors who bought the stock without knowing that may want to consider the conflict of interest. For example, Tipranks issued a smart score of just 5/10.

As shown to the right, ZOM stock does not have a good score on any of the metrics. Only the sentiment score is above the 50% mark due to the stock’s rally in 2021.

The weak stock score suggests that investors should look at the quarterly and full-year 2020 results more carefully.

In the fourth quarter, Zomedica posted a loss of 5 cents a share

. This is still better than the 19 cents a share, or $19.8 million, loss in the year-ago period ended Dec. 31, 2019. The firm is in the development stage, so the lack of recorded revenue is not a concern.

Research and development costs were $8 million. This is lower than the $10.3 million Y/Y because of a drop in general R&D activity. It focused on Truforma development and had lower milestone expenses.

Looking ahead, the distribution agreement with Miller Veterinary Supply is a positive catalyst. Started in 1920, Miller is the oldest wholesale veterinary distributor in the U.S. region. The distribution of Truforma started on March 30. The distributor will target key states like Texas and Maine. Geographically, it will concentrate in the eastern and mid-eastern regions of the U.S.

Zomedica has very low operating costs within the deal. It is supporting Miller with only a few sales representatives, so Miller will only get enough Zomedica staff expertise to elevate customer service levels related to Truforma.

About Truforma

Readers should familiarize themselves with Truforma, a veterinary diagnostic tool. It announced the first commercial sale on March 16. Chief Executive Officer Robert Cohen thanked Zomedica staff. He said they dedicated the past two years of their lives to achieving the critical milestone of commercialization.

James Klein, president of Qorvo Biotechnologies described the platform as a “disruptive milestone in the veterinary diagnostics testing industry that will raise the standard of point-of-care for companion animals.”

Risks

Investors should brace for the possibility of slow initial sales of Truforma. The distributor may need time to ramp up activities to grow sales. Zomedica may need to increase support representative staffing to facilitate Miller’s commercialization activities of the product.

Investors do not have a future cash flow forecast discounted to present value to assess the company’s fair value. Simplywall.st warns that the company is unprofitable. It forecasted earnings losses until FY 2023. It may post profits starting in 2024.

Zomedica is a pure gamble at this juncture. The speculator may bet on the stock bottoming anytime from here. Conversely, the patient investor should wait for the company to post initial revenue figures first before starting a position.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article.

Chris Lau is a contributing author for InvestorPlace.com and numerous other financial sites. Chris has over 20 years of investing experience in the stock market and runs the Do-It-Yourself Value Investing Marketplace on Seeking Alpha. He shares his stock picks so readers get original insight that helps improve investment returns.