Just as I predicted in my last article on ViacomCBS (NASDAQ:VIAC), the company produced a large increase in free cash flow (FCF) during Q1. On May 6, the company presented its latest earnings and cash flow release. As a result of its astounding jump in FCF, I now estimate that VIAC stock is worth at least 81.7% more at $77.70 per share. And it could even go much higher than that target price.

Here is the bottom line. FCF exploded in Q1 to $1.589 billion, up from just $306 million a year ago. In fact, in all of 2020, the company made $1.891 billion in FCF, even though Q4 had negative FCF. So the Q1 2021 number was 84% of the total cash the company produced in 2020.

The reason this happened is that the TV and film entertainment company is hitting on all cylinders. Revenue was up 14% year-over-year (YoY) to $7.4 billion. Of this, the advertising revenue segment was up 21% to $2.681 billion. In addition, its streaming segment grew 65% to $816 million. These were the two largest contributors to the company’s $913 million gain in revenue year-over-year.

So, along with operating cost cuts, this was why ViacomCBS had a gain of $1.283 billion in FCF YoY (i.e., $1.589 b – $306 m). It also implies that full-year FCF for 2021 could be as high as $6.356 billion on a “run-rate” basis.

Valuing ViacomCBS Using Its FCF

Keep in mind that VIAC stock has a market capitalization of just $27.79 billion as of July 9. If we divide its run-rate FCF by the market cap, the FCF yield is an astoundingly high number: 22.87% (i.e., $6.356b/$27.59b). Just to put this in perspective, most stocks with this huge level of FCF will have a much lower FCF yield ratio of say 3% or even 5%. That implies that the market cap must go significantly higher.

In fact, just to be conservative, and, given that its FCF was negative during Q4, let’s assume that the ViacomCBS will be 75% of its run-rate figure. That means we should use $4.767 billion. Now, if we divide $4.767 b by 5%, the target market cap works out to $95.34 billion. That is 3.43 times today’s market cap, implying that VIAC stock should be at $146.70.

Let’s also assume that it will take 2 years for the market to realize this. That means that the stock will rise 85.22% annually, on a compound basis for the next 2 years. So this year, its price target is $79.21.

Just so you don’t think this method is too far out of the question, take a note of this. At the end of 2019, VIAC stock was at $43.72 and had a market cap of $26.887 billion (with 615 million shares outstanding). But during 2019, the company had adj. FCF of $826 million. So, as a result, its FCF yield at the time was 3.07%. Compare that with my projection that it will have $4.767 billion in run-rate FCF with its $27.79 billion market cap today. That is an FCF yield of 17.15%. In other words, VIAC is very undervalued.

Using Historical Dividend Yield To Value ViacomCBS

Another way to value VIAC stock is to look at its historical dividend yield. Right now the company pays a quarterly dividend of 24 cents. Its 96 cents annual dividend per share represents 2.245% of its stock price as of July 9 of $42.77.

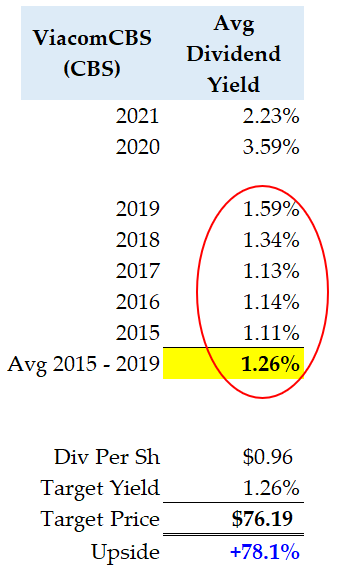

But if we look at its past historical dividend yield history, the stock has had a much lower average yield. For example, if you look at the table on the right you can see that the average yield over the five-year period from 2015 to 2019 was 1.26%. These figures came from Seeking Alpha’s dividend yield data

.

Click to Enlarge

I excluded the 2 most recent years due to the Covid-19 effect on the stock. Once VIAC stock returns to its historical yield, it will move substantially higher.

Therefore, if we divide the 96 cents dividend by 1.26%, the target price is $76.19 per share. That represents a potential 78% upside for VIAC stock.

What To Do with VIAC Stock

We now have two interesting ways to value the stock. Using its FCF yield, the stock target price is $79.21 this year. Using its historical dividend yield, the target price is $76.19. The average target is $77.70, which gives it an upside potential of 81.7% over July 9’s price of $42.77.

Even it takes two years for the stock to reach these levels, the upside is still 34.8% per year. But that is a worst-case situation. I believe that once the market realizes that this company is gushing cash the stock will move substantially higher, likely close to my $77.70 target price.

On the date of publication, Mark R. Hake did not hold a position in any security mentioned in the article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Mark Hake writes about personal finance on mrhake.medium.com and runs the Total Yield Value Guide which you can review here.