Blackberry (NYSE: BB) is one of those companies thats price, revenue and net income charts tell only a part of the business’ story. The company released its fiscal second-quarter results on Sept. 22. Losses ($144 million) were significantly worse than the prior-year quarter. Revenue fell to $175 million from $259 million a year ago. Still, BB stock jumped over 10% in pre-market trading.

Does this mean it’s a good time to buy BB stock? The answer is yes, but only if you’ll be in for the long haul. Here’s why.

What’s Up With BB Stock?

It helps to start with some background of what’s been happening with BlackBerry.

Following the restructuring away from being predominantly a mobile phone maker (remember Blackberry phones?), the company’s revenue took a big hit. It wasn’t until fiscal 2020 that the company reported revenue growth — the first in 10 years.

However, the Canada-based company couldn’t carry the revenue growth momentum into fiscal 2021, no thanks to covid-19.

When analyzing a company undergoing restructuring, it helps to focus on company-specific micro trends as opposed to macro trends. Because those little details are what add up to sustainable growth. Let’s look at some of those micro-trends at Blackberry.

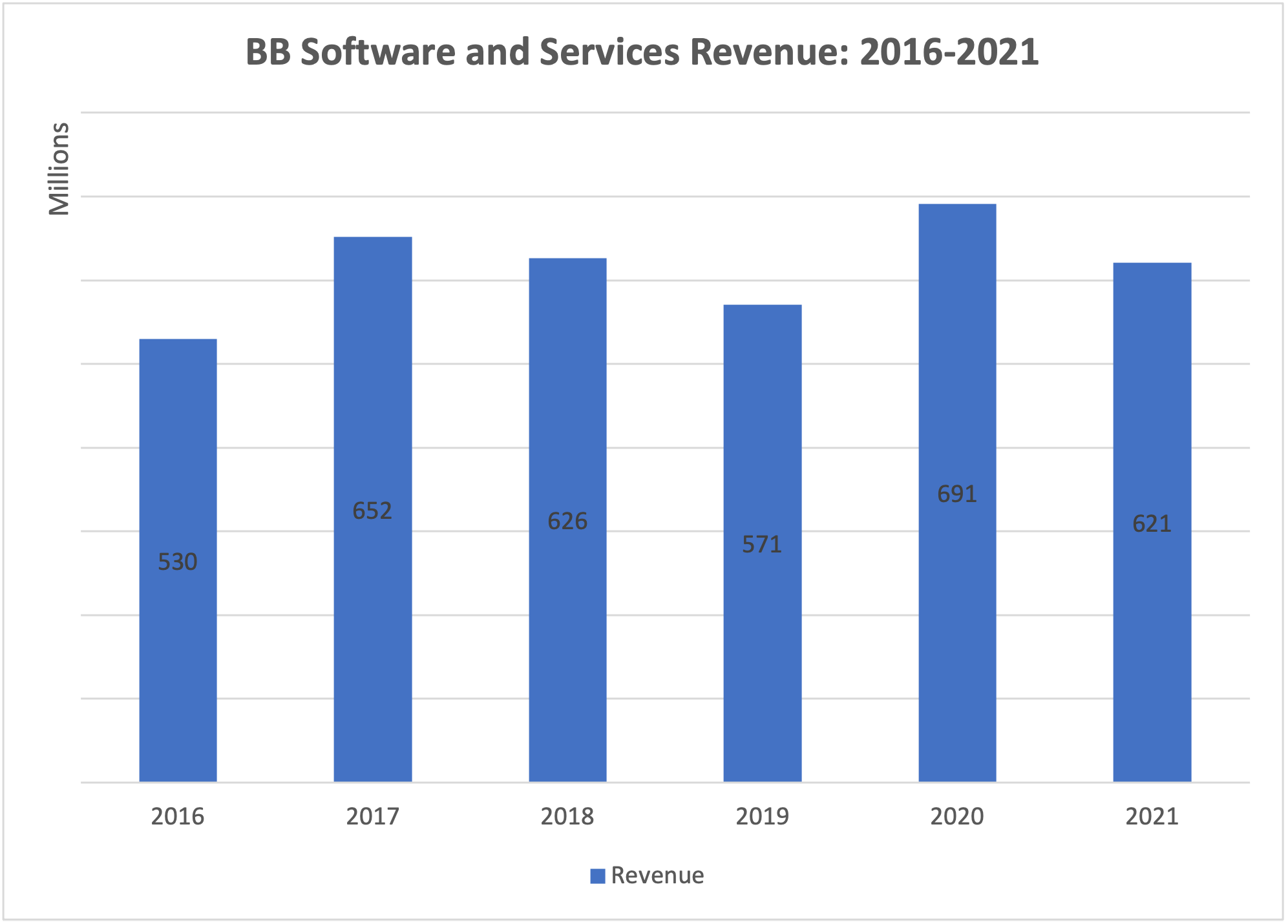

Software and Services Business

Blackberry has two operating segments — software and services, and licensing and others. Its software and services business accounts for much of its business — nearly 70% last year. This segment features its cybersecurity and internet of things (IoT) products.

The licensing business, as the company puts it, “is responsible for the management and monetization of the Company’s global patent portfolio.”

Investors’ focus when considering BB stock should be on the software and services business, given how important the segment is to the company’s top-line. It’s also the business arm that the company is prioritizing for growth.

The chart below shows the revenue from this segment over the last six years.

Click to Enlarge

As the chart shows, there isn’t a clear sign of growth. Of course, one can argue that the company might have built on the growth in fiscal 2020 (i.e., Mar. 1, 2019 to Feb. 28, 2020) had Covid not happened. However, the performance of the years before don’t instill much confidence.

Also, Blackberry isn’t out of the woods yet regarding Covid-driven challenges. During the Q2 call, Chief executive John Chen said, “In terms of outlook, we continue to see the past quarter as the low point but significant headwinds I expect it to continue into Q4 and — Q3 and Q4, and perhaps even beyond that, albeit with a sequentially decreasing impact.”

Here’s a look at the software and services revenue over the past six fiscal quarters.

Click to Enlarge

And that’s part of why I said buying BB stock only works if you’re a long-term investor.

Management Efficiency

While profitability is the ultimate judge of how efficient a company’s management team is with resources, details such as gross and operating margins give better context. Blackberry isn’t profitable at present, with a net loss of $144 million reported in the recently released second-quarter report.

But that doesn’t mean the management isn’t efficient.

The reported loss in recent times is mostly down to high operating expenses — driven by unusually high expenses for certain line items.

For instance, expenses related to amortization, impairment and debenture fair value adjustment totaled roughly $1.19 billion in fiscal 2021 — over 68% of the company’s operating expenses. Expenses related to these items have shrunk in the last two quarters, which should help the company get back to profitability soon.

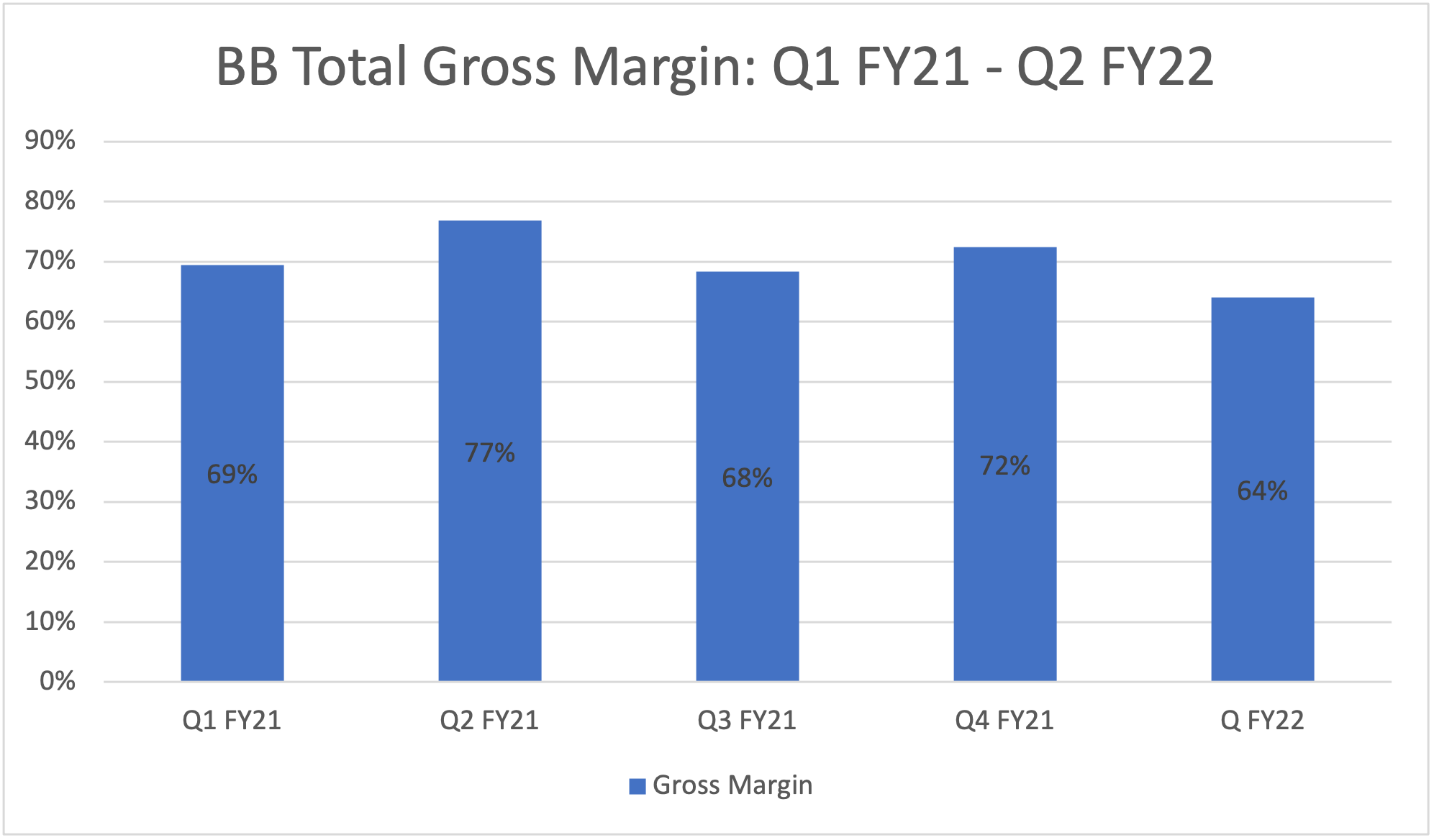

Blackberry’s gross margin is another item that investors should watch. A high gross margin generally means there’s a higher chance of reporting a positive net income — especially if operating losses are controlled.

As the chart shows below, BB has had a gross margin that ranged between 64% and 77% over the past six quarters. This could be higher.

Click to Enlarge

Analyzing segment performance, you’d notice that the cybersecurity division is causing the drag. For the record, cybersecurity is responsible for over 70% of Blackberry’s software and service revenue ($120 million in the most recent quarter). Basically, it’s the biggest operation at Blackberry.

During the Q1 earnings call, Chen estimated cybersecurity gross margin would improve to between 75% and 80% by the middle of next year thanks to increased investment in the sales team. This would certainly help the company get closer to profitability.

BB Stock Verdict

Beyond the numbers, blackberry looks like a pretty solid company.

You don’t get to list your customers and partners without having strong offerings.

For instance, Blackberry’s top IoT offering QNX is the market leader for safety-certified embedded software in automotive, with over 195 million vehicles protected by QNX. On the cybersecurity side, Blackberry now provides its unified endpoint management product to the Microsoft 365 product suite.

To drive it home, I expect the continuous addition of big names to its customer list will help revenue growth over the next few years. And if management can continue to improve its cost structure, Blackberry could potentially become a reliable portfolio holding for several years.

On the date of publication, Craig Adeyanju did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.