Lilium, NV (NASDAQ:LILM) just went public on Sept. 14 via a reverse merger with a SPAC (special purpose acquisition company). It now looks like a bargain. SPAC shareholders have been selling after the merger and indeed, 65% of the SPAC owners sold their shares of LILM stock back to the company at the merger.

So that reduced the total cash available to Lilium. However, the institutional investors did not reduce their deal. They still provided $450 million to Lilium. Originally, the SPAC had $380 million, but it had to pay out 65% of that at $10 per share to the redeeming SPAC shareholders. That reduces the cash in the SPAC available to Lilium to $133 million.

As a result, the gross cash available to Lilium is $583 million. After $50 million in transaction expenses, the gross cash available was $533 million. Lilium was originally expecting $830 million.

Click to Enlarge

However, since there is also $166 million in debt, the net cash is $367 million. That is $247 million lower than the original net cash expected by Lilium of $614 million.

Bottom line: Lilium may have to raise more cash. All of this information is available from page 51 of Lilium’s slide deck.

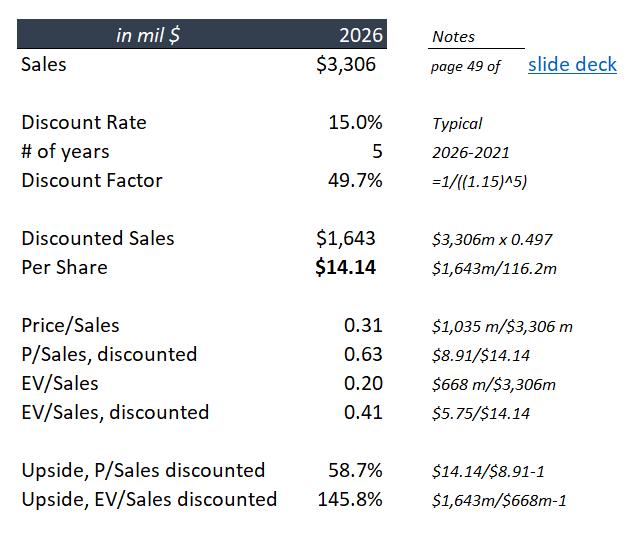

You can see the details of the revised transaction in the table I have prepared. It shows that the market cap is now $1.035 billion and its enterprise value (EV) is 668 million, or $5.75 per share.

I am going to show in this article why I think this valuation is a bargain for most investors now. My calculations are based on the company’s slide deck presentation.

Analyzing Lilium

Lilium has a very unique electric vertical take-off and landing (eVTOL) jet technology and a unique business plan. Moreover, its ducted electric vectored thrust (DEVT) technology truly sets it apart from virtually all other typical propeller blade eVTOLs planes.

This can be seen on page 21 of its slide deck. But I think the best way to understand the company is to watch this very interesting YouTube video. It explains the technology in much more detail.

As a result of this unique niche as well as its funding I think it’s more likely than not that Lilium will be able to execute its business plan. On page 49 of the deck, Lilium shows its sales and EBITDA projections and assumptions. By 2026 it expects to have over $3 billion in sales.

The best way to see my calculations is to study the spreadsheet I’ve prepared. You can also see how I made the calculation with my notes.

Click to Enlarge

The table shows that the present value of the 2026 forecast sales is $1.643 billion. As a result, the price/sales multiple is just 0.31. However, if we take into account enterprise value and divide it by the present value of sales the multiple rises to 0.41.

That seems to be too cheap. That is especially the case since I already discounted the future revenue 0f 2026 by over 50% to reduce it to its present monetary value.

For example, if we assume that the stock should trade at 1 times discounted sales, the upside is 59% (i.e., $14.14/$8.91). However, using an EV/Sales discounted multiple of 1 times the upside is 146%. But to keep things simple and conservative say that the target price should be $14.14.

In fact, on page 50 of the slide deck, Lilium indicates that its comp valuation should be between 1.2x and 2.3x EV/Sales. So our metric of 1 times sales is very defensive and conservative.

What To Do With LILM Stock

This shows that investors can reasonably expect to make a minimum of 59% and up to 146% in LILM. Let’s say it takes up to 4 years for the stock to basically double (since the market would anticipate the 2026 sales by 2025). That implies that the average annual return would be 18.9% per year on a compounded basis each year. That is a pretty good return for most investors.

Bottom line: take advantage of the price here as it is selling below the original $10 SPAC price as well as the price that the institutional investors paid for their shares. LILM stock is worth at least $14.14 per share, or 59% more.

On the date of publication, Mark R. Hake did not hold any position (either directly or indirectly) in any of the securities mentioned in the article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Mark Hake writes about personal finance on mrhake.medium.com and runs the Total Yield Value Guide which you can review here.