- Carnival Cruises’ (CCL) long term recovery continues.

- Industry experts and fans can carry it over the hump.

- Investors must navigate current macroeconomic and geopolitical obstacles.

Carnival Cruises (NYSE:CCL) stock had its best days in 2017. Unfortunately, now it sits near levels that have been in contention since 2000. The fall from grace five years ago was violent and persistent. CCL stock is now but a quarter of its high watermark value. At its lowest during the pandemic, Carnival almost crashed 90%.

Unlike most of the stock market, the cruise industry has not yet recovered its pandemic neckline. When the lockdowns happened, the travel and leisure sectors suffered in a bad way. Cruise lines especially took it hard. They were last to come back into business because of government restrictions.

Cruising was already susceptible to having sicknesses on board. Convincing strangers to gather on a vessel post Covid-19 was not going to come easy. With vaccines, now it’s a possibility. The reconstruction of the cruise line businesses can resume. Meanwhile, the fundamentals for CCL stock are likely to remain horrendous a bit longer.

We can’t even discuss valuations because the metrics are completely out of whack. For example, CCL revenues are one fifth those from 2019. And they are still carrying a $9 billion net yearly loss. Last year, Carnival lost $4 billion in cash from operations. It is a miracle that these companies are still in business. This is a testament to the competence of the management teams. They don’t make tests tougher than what this sector just went through.

| CCL | Carnival Corporation & plc | $17.83 |

CCL Stock Needs Time to Heal

Click to Enlarge

It will take time, but the reparations are afoot. Buying the stock now as an investment makes some sense. This is not a slam dunk and it will require patience, not a quick flip. However, because of the Reddit effect, sharp spikes are happening sporadically. Investors would do well booking profits if they get such opportunities.

In the long run, CCL stock could recover to $40. However, it would need a few miracles in the short term. Management will need to show tangible progress in the financial metrics. That is not likely going to be a quick feat.

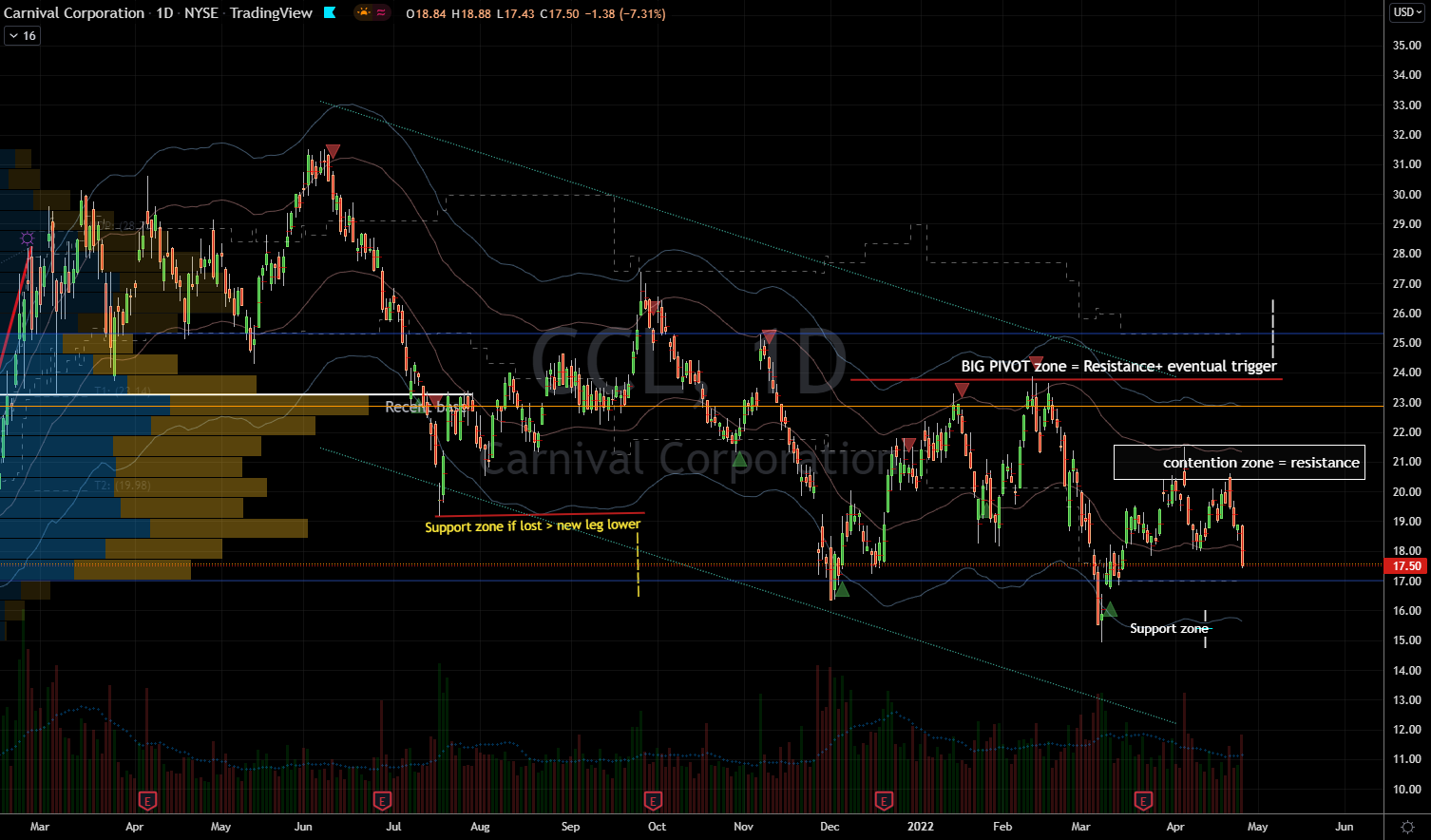

Meanwhile, the sector stocks are volatile enough for traders to have fun too. There is support below $16.50, just as there is resistance above $21. These are ranges that can deliver short-term profits for those who can trade fast. Otherwise, it may require a lot of patience and intestinal fortitude to sit on under-performing stocks for a while. The trend is still in the hands of the CCL bears.

This means that I expect rallies to fade in a descending channel of lower-lows and lower-highs. CCL stock is still seeking a true bottom. The March 8th low could be it, but I would rather see evidence of that before I can trust it. Those who trusted the December 1st low learned that they made a mistake.

Since equities are wobbly, I would caution against having complete confidence in this thesis. Investors and traders alike need to be more humble than normal under these iffy conditions. The U.S. Federal Reserve’s rhetoric is causing a ruckus in all markets, not just equities. This week the currency markets are also in trouble and causing broad repercussions. CCL stock cannot rally if the markets are correcting. Therefore, we must pay attention to what happens this week to the entire market on Wall Street.

From conversing with hundreds of traders on a regular basis, the fans of cruise stocks are staunch. Even the experts can’t fall out of love with the sector given all these challenges. According to Yahoo! Finance, 16 out of 25 analysts who CCL stock rate it as a buy or strong buy. Frankly I find this majority exuberance rather strange. But it is an intangible asset to the stock price in the long run.

On the date of publication, Nicolas Chahine did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.