If you have a budget of around $1,000 and you’d like to buy some solid stocks to beat the market, I’ve got you covered! The stocks in this article total around ~$383 as of writing if you bought one of each. With a modest $1,000 investment, you have ample dry powder to allocate into whichever stocks you like the most and potentially have money left over to dabble in some penny stocks as well.

Investing with a limited budget can be daunting, but as the saying goes, “Mighty oaks from little acorns grow.” Even with a small initial investment, compounding returns can work their magic over time. Regardless of whether you have a much smaller or bigger budget, it’s worth looking into the following seven stocks for potential market-beating gains:

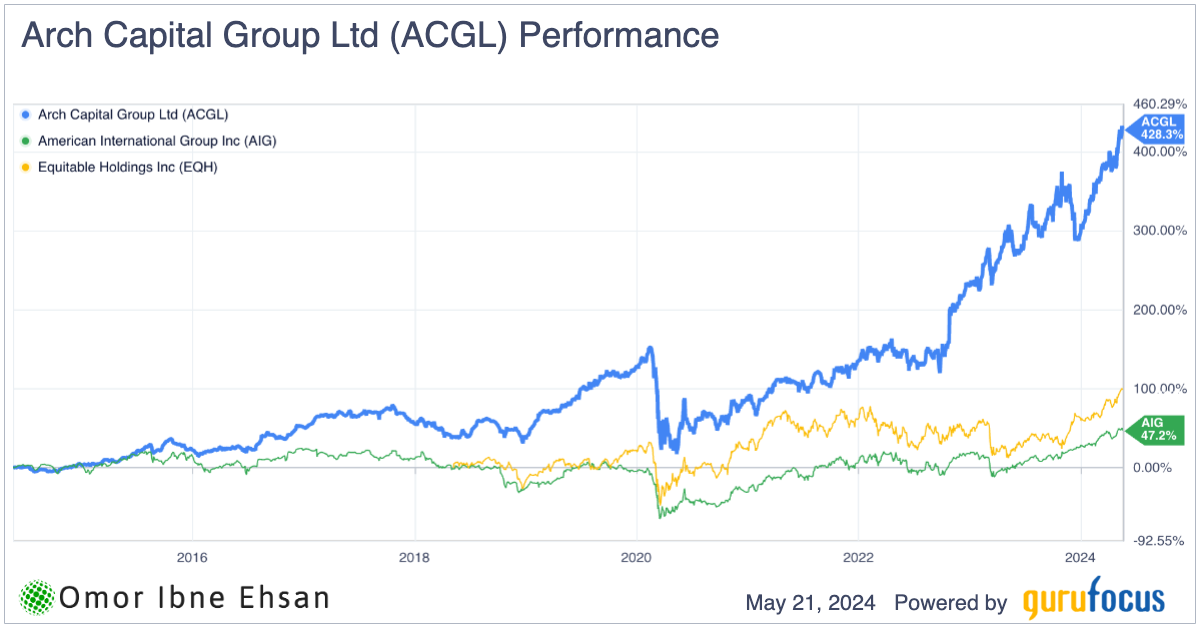

Arch Capital Group (ACGL)

Arch Capital Group (NASDAQ:ACGL) has been one of the best-performing insurance companies post-COVID.

Click to Enlarge

Q1 results highlight why I’m optimistic about this experienced insurance company’s future. Their underwriting income grew tremendously thanks to favorable market conditions, reaching an impressive $736 million. With gross premiums written increasing substantially to $5.6 billion, a 26% jumpy.

It is also acquiring parts of Allianz’s U.S. business. Adding their middle market and entertainment operations should complement Arch’s specialized focus well by bringing in more reliable, recurring premium income. Arch pointed out that it opens major new avenues in the huge U.S. middle market sector of over $100 billion.

While severe weather events this quarter, such as the Baltimore accident, reduced the bottom line somewhat, Arch’s diversified portfolio allowed them to weather the impact successfully. I see Arch continuing its pattern of strong, profitable expansion going forward.

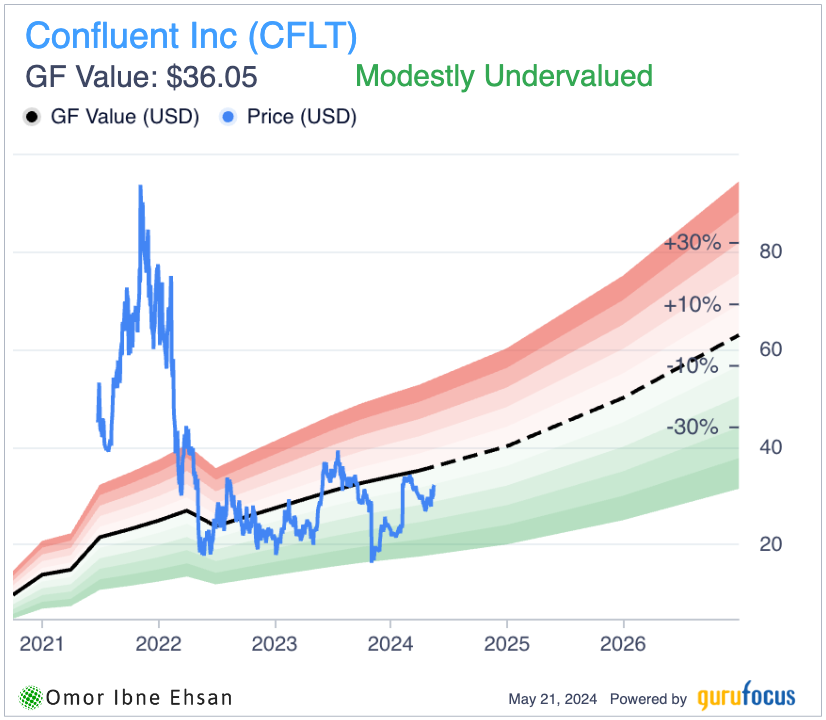

Confluent (CFLT)

Confluent’s (NASDAQ:CFLT) performance this earnings season has also been stellar, with beats on both the top and bottom lines. I think this is a no-brainer bet if you think the cloud and data sector will continue to do well in the coming years.

Revenue increased by 25% to $217 million, and over half of subscription income now comes from their cloud offering. The launch of Tableflow could be a game-changer in seamlessly combining real-time data with broader analytics tools using open standards. As companies collect more data from different sources, Confluent will likely land much more business.

Click to Enlarge

I believe the stock has big upside potential if it can keep up this momentum. While uncertainties remain in the broader economy, Confluent’s strong execution and expanding product offerings put them in a good position to capitalize on the explosive growth in real-time data streams. Definitely one of the best growth stocks you can buy right now.

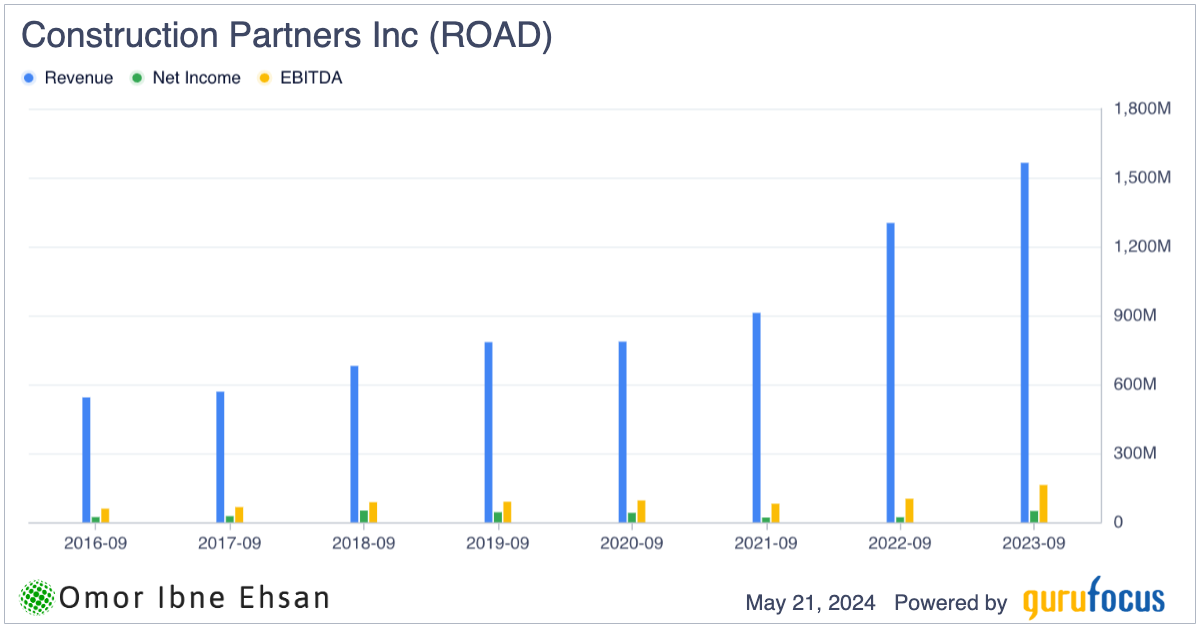

Construction Partners (ROAD)

Construction Partners (NASDAQ:ROAD) delivered solid FY2024 Q2 results despite the seasonally slow winter quarter. It also benefits from solid tailwinds from onshoring megatrends. Revenue grew 14% YOY to $371 million, exceeding Wall Street estimates. It is not profitable right now, but analysts expect full-year profits and a 25.6% EPS increase next year. The growth has been very stellar.

Click to Enlarge

Federal and state infrastructure spending and healthy commercial real estate activity in Construction Partners’ key states are driving growth. This strong demand environment allowed the company to increase its backlog to an impressive $1.79 billion.

With most of the fiscal year 2024’s revenue already secured through signed contracts, Construction Partners is well-positioned to be choosy on new projects while maintaining healthy profit margins. The strategy of expanding market share organically while making strategic acquisitions in key markets like the Atlanta suburbs also appears to be yielding results.

Given the strong performance in the first half of the year and positive demand outlook, it’s no surprise management raised full-year guidance. While shares aren’t cheap based on current valuation metrics, I believe the long-term growth story remains intact for this leading infrastructure services provider in the fast-growing Southeast region.

Li Auto (LI)

Li Auto’s (NASDAQ:LI) has been disappointing lately, much like many other EV companies, but I still think it is the best EV stock you can buy all around. The growth here remains stellar and has been better than almost all of its competitors, and sales volume has bested even BYD (OTCMKTS:BYDDY) and Tesla (NASDAQ:TSLA) in many Chinese regions.

Q1 wasn’t the best. While vehicle deliveries jumped 52.9% to over 80,400, revenue growth of 36.4% to RMB25.6 billion fell short of market expectations. The 20.6% gross margin was respectable given the introduction of the new model, but Li faced some challenges in meeting its targets.

Surpassing 41,000 orders in just weeks for the L6 model is certainly nothing to overlook. However, Li acknowledged facing internal and external obstacles that make me cautious about their ability to navigate issues.

The company is taking steps in the right direction by reorganizing to boost productivity and reacting swiftly to shifting market conditions with almost RMB100 billion in funds.

I still think it is one of the best growth stocks you can buy, as EV sales will likely recover in the coming quarters. Analysts also remain bullish.

Click to Enlarge

CRISPR Therapeutics (CRSP)

CRISPR (NASDAQ:CRSP) is riskier than most stocks on this list, but I think it has found a bottom. If this tech pays off, the upside here could be enormous.

CRISPR continues making headway in developing treatments across a variety of health conditions. Their work to edit genes in vivo, as well as research into cancer, immune diseases, and diabetes, holds promising opportunities. The addition of two preclinical programs, CTX340 for treatment-resistant high blood pressure and CTX450 for acute hepatic porphyria, shows how their modular nanoparticle platform could apply gene editing across multiple areas. With initial animal testing underway, both programs may enter human testing in late 2025.

While their goals remain long-term, CRISPR is making steady, methodical progress, changing their gene editing expertise into potential new medical solutions. The company seems well set up for growth, with important results expected over the next year and a half.

VGP NV (VGPBF)

VGP NV (OTCMKTS:VGPBF) is an investment holding company. It did well in 2023, even with the challenges in the market environment. They reported strong leasing activity, with more than half of new leases coming from light industrial spaces. Diversifying beyond just logistics into other areas should help provide some stability when times are tough.

VGP generated solid profits before taxes of €112.7 million and earnings per share of €3.20. But what caught my eye was the €676 million they could recycle through their joint venture partnerships.

With nearly 2 million square meters of new land acquired, including prime locations near major cities like Paris and Frankfurt, VGP is well set up for continued growth. The €170 million sale of their 50% stake in the Moerdijk project also seems well-timed and should boost their available funds.

While leasing e-commerce spaces was muted at just 1%, management expects that segment to rebound by 2025. I think if execution remains strong, the stock could make a full recovery back to its 2022 highs in the coming years.

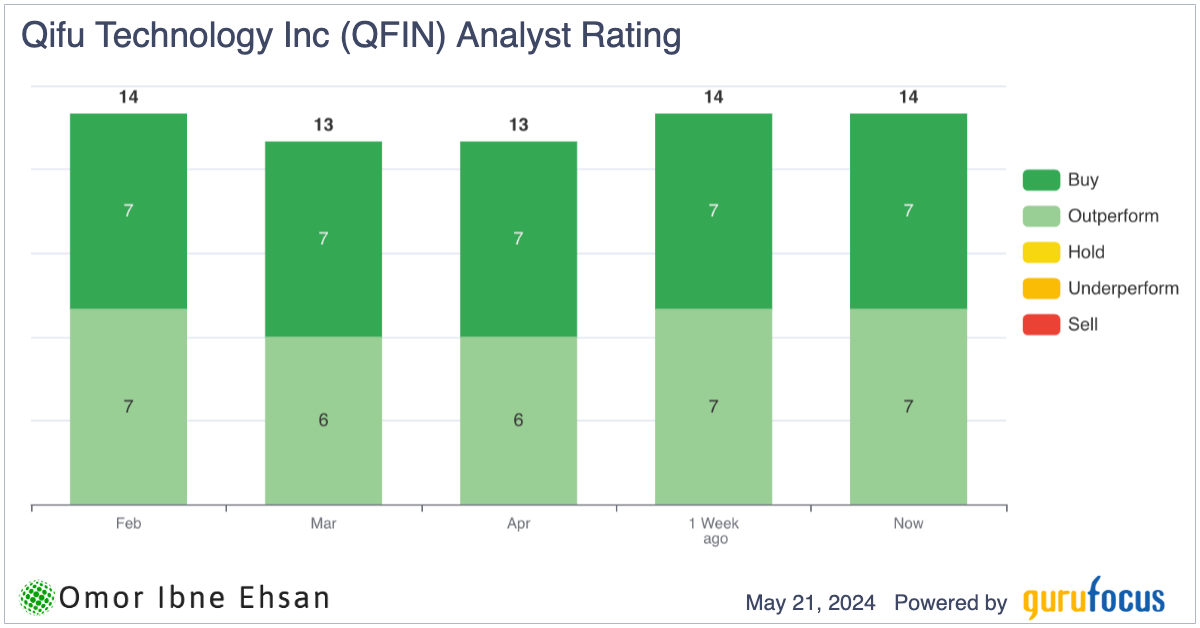

Qifu Technology (QFIN)

Qifu Technology (NASDAQ:QFIN) is a Chinese credit-tech company. It has a very good dividend yield at 5.3% and is up 36% year-to-date as the broader Chinese market recovers.

It had a very positive Q1, with revenue and earnings growing strongly despite challenges in the broader economy. Sales increased by over 15% compared to last year, bringing in over 4.2 billion yuan. At the same time, their net profit margin on each sale improved to around 3.5%, allowing their net income to jump over 23% to over 1.2 billion yuan after removing non-routine expenses.

Qifu “focuses on maintaining healthy risk levels and using data-driven insights to reduce losses.” The expected amount they may lose on new loans dropped about 15% from the previous quarter as fewer customers struggled to make timely payments and more payments were collected. They also did well in lowering their funding costs by over 70 basic points from the last period, in part by issuing more Asset-Backed Securities with lower interest rates.

I think QFIN could also make a full recovery if execution continues. Analysts are bullish here as well.

Click to Enlarge

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.