Cheap tech stocks with triple-digit upside? In 2024? It may sound like fantasy, but some very good deals are on the market. Of course, you won’t be able to find high-quality businesses trading at bargain-basement prices like in mid-2022, but there are plenty of cheap tech stocks with 150%-plus upside if you are willing to hold over the next few years.

You’ll have to take a bit more risk right now. The market rally has lasted longer than most people would have thought. This has caused most tech stocks to reach modestly overvalued levels or at least trade at fair prices. As such, we’ll naturally have to dig a little deeper, but I think the upside potential outweighs the risks here. Let’s dive in!

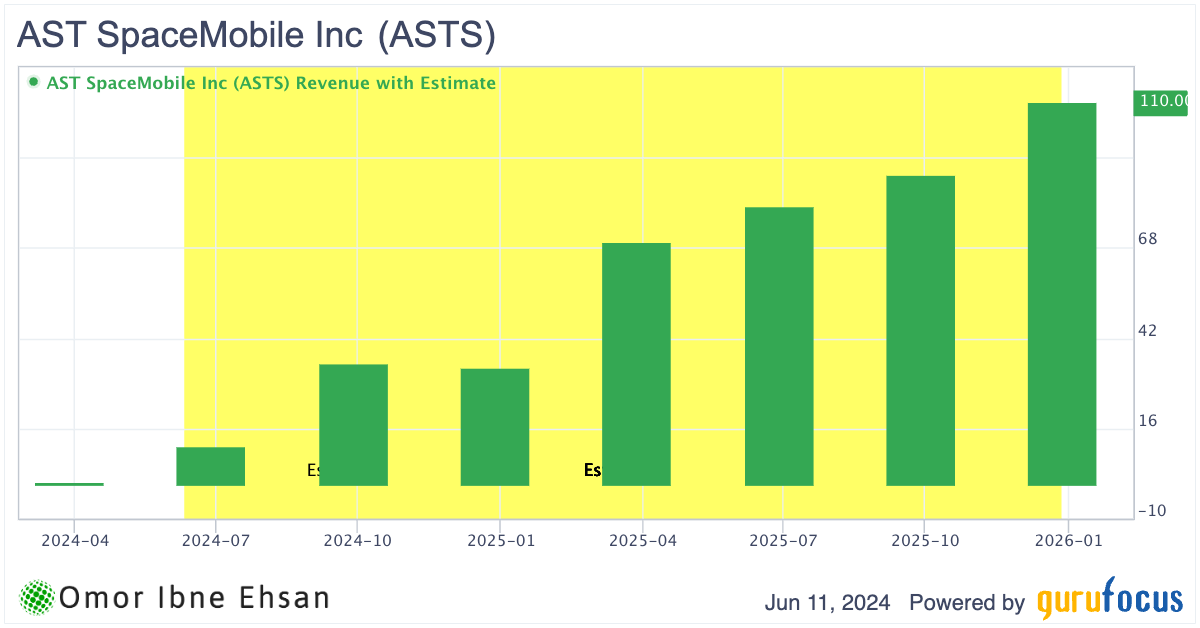

AST SpaceMobile (ASTS)

AST SpaceMobile (NASDAQ:ASTS) is building the first global cellular broadband network in space to operate directly with unmodified mobile devices. While the company currently generates minimal revenue of just $500K in Q1 and remains deep in losses, I believe the long-term outlook remains exceptionally bullish.

Management reiterated the July/August timeline for delivering the first five Block 1 satellites, enabling nationwide non-continuous cellular service across the U.S. The recent definitive commercial agreement with AT&T (NYSE:T) through 2030 validates the business model and should serve as a template for global expansion.

Click to Enlarge

With $210 million of cash on hand, ASTS has ample liquidity to reach profitability as revenue scales from an estimated $18.5 million this year to potentially $811 million by 2026.

While these projections are undoubtedly lofty, capturing even a fraction of the $34.5 billion revenue estimate by 2032 could deliver stellar returns.

BK Technologies (BKTI)

BK Technologies (NYSEMKT:BKTI) develops single and multiband radios for critical communications. I see major upside potential here as the company rides the same tailwinds, propelling Axon (NASDAQ:AXON) to new heights. As social unrest escalates, police and firefighting agencies are seeing budget increases, driving demand for BK’s cutting-edge radio products.

While its $46 million market cap may seem modest, don’t overlook the explosive growth. Analysts expect revenue to grow 8% this year and 25% in 2025. Even more enticing, EPS is projected to skyrocket 250% next year. That means shares are trading at a mere four times 2025 estimated earnings.

In Q1, BK’s gross margin expanded to 34.5% from 26.1% a year ago, with further improvement expected as they target historical 35%+ levels. The BKR5000 radio saw robust demand, fueled by a 5,620-unit order from the USDA Forest Service. Boulder County’s order for the BKR9000 model means it appeals to larger markets. I think this under-the-radar gem could deliver triple-digit gains.

Couchbase (BASE)

Couchbase (NASDAQ:BASE) provides a modern database for enterprise applications. The company delivered strong Q1 2025 results, with revenue of $51.3 million, growing 25% year-over-year and beating the high end of guidance by $2.4 million. I believe Couchbase is well-positioned to benefit from the explosive growth in data and AI adoption across large enterprises.

Despite these solid fundamentals, BASE stock has faced a steep 38% selloff from its March peak, primarily driven by a series of price target cuts by institutional investors like RBC Capital Markets. However, this appears to be more of a sector-wide valuation compression impacting software stocks broadly instead of any Couchbase-specific concerns.

The recent pullback presents an attractive entry point for long-term investors. GuruFocus’ DCF model sees a triple-digit upside if held for many years.

Click to Enlarge

Couchbase’s modern database platform is tailor-made for data-intensive, AI-powered applications rapidly becoming the norm. With key metrics like ARR growing 21% and Capella now representing 29% of the customer base, I believe Couchbase’s growth story remains firmly intact. The stock looks significantly undervalued at these levels. RBC cut price targets only by $4, from $35 to $31, and it cut price targets for Snowflake (NYSE:SNOW) and cited the same reason: “peer multiple compression.”

BM Technologies (BMTX)

BM Technologies (NYSEMKT:BMTX) provides banking services to colleges and universities across the country. This fintech player is poised to ride the digital banking megatrend to new heights in the coming years. In Q1, BMTX’s revenue surged 21% year over year to $16.2 million, while net income skyrocketed to $748,000 from a loss last year. The company’s strategic shift to a new partner bank and variable rate deposits is paying off.

BMTX’s unique customer acquisition model through long-term university contracts gives it a steady stream of young customers ripe for cross-selling. As it modernizes its tech stack, I expect BMTX to unlock significant new revenue streams and boost customer lifetime value.

BMTX’s involvement in the challenged banking sector and the recent rally may give some investors pause. However, with analysts projecting profitability in 2025, I believe the risk-reward is attractive for this small-cap with 150%+ upside potential. BMTX’s solid Q1 growth and improving financials suggest it is on the right track to capitalize on the digital banking boom.

Genius Sports (GENI)

Genius Sports (NYSE:GENI) provides sports data and streaming services to leagues, sportsbooks, and media companies. This U.K.-based firm is well-positioned to capitalize on the explosive global growth in sports betting and the insatiable demand for live game data.

In Q1, Genius delivered an impressive 23% revenue growth to $120 million, beating guidance by $3 million. Management raised full-year 2024 revenue guidance to $500 million. I expect Genius to sustain 15-20% annual sales growth for the foreseeable future.

The company’s strategic focus on soccer should be a major tailwind, as it’s the world’s most popular sport with a massive betting handle. I wouldn’t be surprised to see major contract wins ahead of the 2026 World Cup.

Click to Enlarge

Genius is targeting EBITDA margins of 16.4% this year, up 350 basis points, as its operating leverage improves. Analysts expect breakeven in 2026, but given the scalability of its data-driven model, profitability could come sooner.

LiveRamp (RAMP)

LiveRamp (NYSE:RAMP) provides data connectivity solutions for businesses. The company reported strong Q4 results, with revenue and operating income exceeding expectations. Subscription revenue growth accelerated, and annual recurring revenue grew the fastest in over a year. LiveRamp is well-positioned to capitalize on the growing need for secure first-party data collaboration and addressable digital advertising amid third-party signal loss. I believe these megatrends could propel the stock significantly higher in the long run.

However, it’s important to note that LiveRamp’s stock has been quite volatile, with steep ups and downs over the past few years. It’s currently down nearly 65% from its 2021 peak and almost 18% year-to-date. That said, I think the stock is entering oversold territory. While there are risks, I believe LiveRamp’s strong market position and growth potential could deliver hefty gains for patient investors willing to ride out the near-term volatility.

FlexShopper (FPAY)

FlexShopper (NASDAQ:FPAY) provides lease-to-own solutions for consumers to obtain durable goods. This small-cap stock, currently trading around $1, offers immense upside potential in the long run.

The company is riding powerful tailwinds from the rise of alternative financing options and increasing consumer demand for affordable access to essential products. As inflation erodes purchasing power, FlexShopper’s business model of providing lease-to-own solutions is becoming more popular. Loan revenues have increased significantly and could compound even more.

Click to Enlarge

In Q1, FlexShopper delivered strong growth, with revenue growing 10% year over year. Gross profit increased over 31%. Operating income reached $5 million from $4.2 million in the year-ago quarter.

While FPAY’s tiny $25 million market cap makes it the riskiest stock on my list, I believe the long-term potential is substantial. The stock has a history of explosive triple-digit gains from the $1 level.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.