Jobs data shows a cooling economy… unemployment ramps higher than expected… the “shadow chair” is coming – but who will it be?… different rate cut paths, but the same destination?

Today’s much-anticipated employment report finally arrived, and it delivered a tale of two months.

Following the 43-day federal government shutdown, which delayed data, the Bureau of Labor Statistics reported a sharp loss of 105,000 jobs in October, followed by a modest gain of 64,000 in November.

That November gain did beat expectations, but it hardly signals robust demand. Roughly 70% of all job creation came from the healthcare sector, meaning that growth was far from broad-based.

The most important figure this morning wasn’t payrolls at all – it was the unemployment rate, which climbed to 4.6% in November, its highest level in more than four years.

That matters because, just last week, the Fed’s updated dot plot showed policymakers expecting unemployment to peak at 4.5% this year before beginning to ease lower. So, we’re already above that projection.

Now, to be fair, the BLS – and Powell himself – warned that the government shutdown could distort the data, potentially pushing unemployment higher in the short term. So, this 4.6% reading should be taken with a grain of salt.

Still, the broader picture wasn’t encouraging. Here’s CNBC:

A more encompassing measure that includes discouraged workers and those holding part-time jobs for economic reasons swelled to 8.7%, its peak going back to August 2021.

So, what are we to make of this as investors?

Well, the labor isn’t collapsing, but it’s clearly cooling. That’s not great news for sustained consumer spending, which accounts for roughly 70% of the U.S. economy.

On the other hand, the rising unemployment rate could nudge policymakers to ease financial conditions. But this isn’t a foregone conclusion for a few reasons:

- The 64,000-job gain came in above expectations

- Today’s data likely wasn’t weak enough to disrupt Powell’s “wait-and-see” stance from last week

- There’s still the inflation part of the equation (we get the new CPI report this week).

Overall, the Fed isn’t reacting to one or two jobs reports. It’s watching a much broader mix of inflation and growth data.

Meanwhile, another drama is unfolding – one that could end up having far more influence over rate policy than any single jobs report… or even several months’ worth of them.

The Fed’s public message vs. its private reality

Officially, the Fed remains patient, data-dependent, and noncommittal.

As Powell put it last Wednesday:

We’re well-positioned to wait and see how the economy evolves from here.

Wall Street heard that and quickly pulled back expectations for near-term cuts. And this morning’s data hasn’t changed that.

As I write on Tuesday, the CME Group’s FedWatch Tool puts the likelihood of a cut in March as a toss-up. April is the first month when traders assign majority odds to the next quarter-point cut.

However, according to our hypergrowth expert, Luke Lango of Innovation Investor, traders expecting a sleepy, inactive Fed over the next few months have it wrong.

Luke has written that the next handful of months will bring the rise of a “shadow chair.” Someone without the gavel yet – but with growing influence:

FOMC members will know who’s coming. They’ll know how that person thinks about inflation, unemployment, and asset prices.

Just as importantly, Luke says these Fed members will understand the political backdrop:

Trump wants a strong economy and strong markets heading into the 2026 midterms, not some academic experiment in tight money.

Put it all together, and Luke expects a transition period where the Fed is publicly cautious, while privately preparing for slower growth – and increasingly factoring in the preferences of a chair-elect who may be more inclined to ease than current forecasts suggest.

Here’s what this means for rates:

The odds of additional cuts by spring are probably higher than what the market is currently pricing.

So, who is this shadow chair?

Does a new wrinkle complicate Luke’s forecast?

Until recently, Luke has been clear about his expectation: Kevin Hassett is the likely candidate to be the next Fed chair.

Hassett is a former Trump economic adviser with a long record of emphasizing growth risks, market stability, and the danger of overtightening.

He fits cleanly into Luke’s “shadow chair” framework — a chair-elect who would quietly give the Fed’s dovish wing cover to ease policy as the economy cools.

In that scenario, the logic is straightforward: a growth-friendly chair… more comfort cutting rates… easier financial conditions into 2026… stocks applaud.

Now, while Hassett remains a leading contender for the role, over the past several days, a new twist has emerged – one that doesn’t overturn Luke’s thesis, but does add nuance to how it may play out.

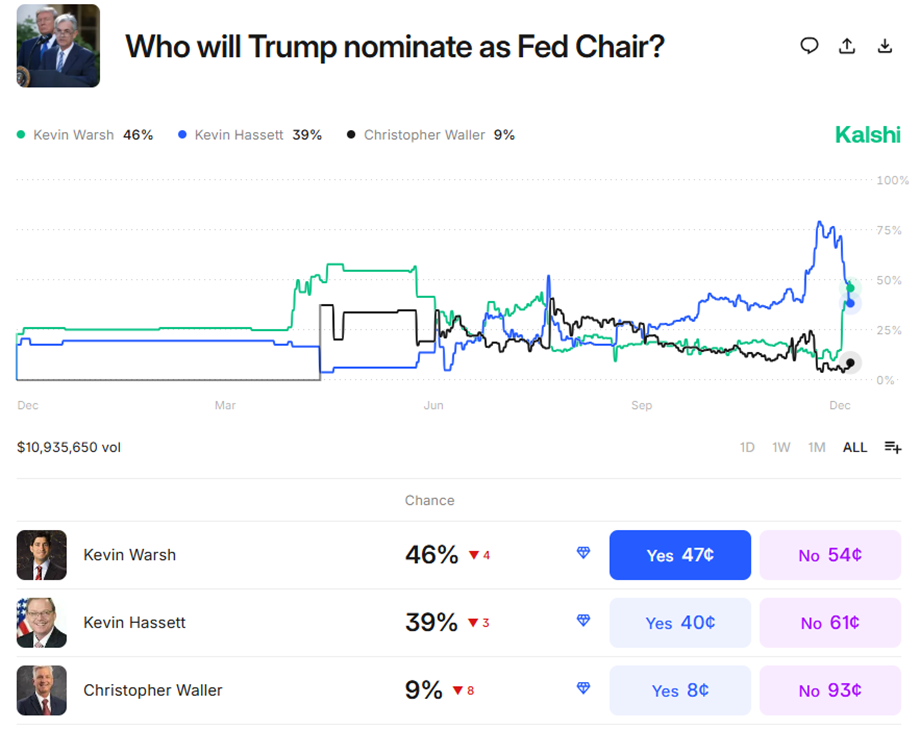

Enter Kevin Warsh

Former Fed Governor Kevin Warsh has now emerged as a serious – and possibly leading – contender.

Earlier this morning, the predictive markets platform Kalshi put Warsh in the top spot, assigning him roughly 46% odds of getting the nomination, compared with 39% for Hassett.

Source: Kalshi

Now, at first glance, this might seem confusing.

Warsh is widely viewed as more hawkish than Hassett – more focused on inflation credibility, more critical of QE, and more skeptical of the Fed’s role in inflating asset prices.

So why would President Trump – who wants meaningfully lower rates – lean in this direction?

Probably because Trump isn’t viewing this issue purely as “who will cut the most?” He’s also thinking about the politics of the decision, and asking himself, “Who can cut without triggering a backlash?”

And this is where Warsh brings something Hassett doesn’t…

What Warsh would give Trump

To the markets – especially bond markets – Warsh looks like someone who will not ease recklessly or for political reasons. He speaks the language of central bank independence.

This credibility matters.

A chair perceived as too dovish from day one risks pushing long-term yields higher, strengthening the dollar, and undermining the very easing that Trump wants.

Plus, practically speaking, even if Trump wants Hassett more, he might have an easier time getting Warsh through confirmation politics.

A former Fed governor with establishment bona fides is typically simpler to shepherd through the process than a sitting or recent White House insider – and you’ve probably noticed how much of the press coverage frames this as Warsh the “institutional” option versus Hassett the “Trump loyalist.”

So, here’s what Trump might be thinking…

Hassett makes me look like I’m setting up a puppet chair.

Warsh will sound tougher on inflation at first, but that doesn’t mean he won’t cut later with less resistance.

This morning, Hassett tried to push back on this, saying:

The Federal Reserve’s independence is really, really important, and the voices of the other people at the [Federal Open Market Committee], they’re important, too…

The idea that someone isn’t qualified for the job because they are a close friend who’s worked well with the president is something that I think the President rejects.

Shockingly, it appears this might have worked – at least according to Kalshi. As we’re going to press, Hassett is back in the lead…

Now, given how quickly these odds move, let’s continue with our focus on Warsh as the potential new Fed chair.

If he is more hawkish, why should we believe he will cut rates at all?

Why the rate-cutting narrative is still in play

The case for Warsh cutting later rests on how hawkish chairs have historically behaved, not on Warsh transforming into a dove or succumbing to pressure from Trump.

First, as just noted, Warsh’s credibility matters to the markets. It buys flexibility.

A chair who establishes inflation discipline early can ease later without spooking Wall Street. Bond investors tend to resist cuts from someone they don’t trust – but once trust is established, resistance fades when/if growth slows.

Meanwhile, Warsh isn’t blind. This morning’s data shows that the economy isn’t exactly firing on all cylinders. So, if/when the data deteriorates further, he’s likely to respond – which brings us to the next point…

Warsh is generally data-driven, not a hardline hawk.

While he’s been critical of QE and excess liquidity, he’s never argued that policy should ignore labor-market weakness. So, if unemployment continues to rise and growth slows, his stance would likely support rate cuts – just later and with clearer justification.

Finally, politics still applies.

No Fed chair – hawkish or not – wants to preside over a deep slowdown heading into an election cycle if the data clearly argues for relief.

So, the main difference between these two top contenders is that Hassett would likely pull cuts forward, while Warsh would likely delay them – then face less resistance when the time comes.

That’s the trade-off Trump is probably weighing.

None of this contradicts Luke’s core point. The Fed is still transitioning away from “crush inflation at all costs,” and a leadership change still weakens Powell’s grip.

So, whether it’s Hassett or Warsh, the idea that the Fed simply goes dormant for months – and delivers only a single rate cut in 2026 – is likely an oversimplification.

Bottom line…

Today’s unemployment report confirms what we knew – the labor market is cooling but not at a panic-inducing rate. On its own, that gives the Fed cover to stay patient and stick with its wait-and-see stance.

But job data isn’t the only thing that will determine where rates go next. Clearly, who leads the Fed matters too.

At first glance, the difference between Hassett and Warsh looks meaningful. But when you dig in, the distinction may be less about where rates are headed and more about how and when they get there.

We’ll give Luke the bottom line:

[Trump’s] “shadow chair” will begin shaping policy long before the official transition.

Rates are still headed meaningfully lower in 2026.

The path may wobble, but the destination hasn’t changed.

Stay constructive, stay opportunistic, and keep buying great AI names on weakness.

Have a good evening,

Jeff Remsburg