Markets flip to rate-hike odds for the first time this cycle… OpenAI kills Sora as AI monetization wobbles… private credit investors race for the exits… and why it’s all the same story

Last Friday, futures markets flashed a warning that would have seemed almost unthinkable six months ago…

A rate hike.

According to CME Group’s FedWatch tool, the probability of a rate increase by year-end crossed the 50% threshold for the first time last Friday. That’s a stunning reversal from the rate-cut narrative that has dominated market thinking for the better part of two years.

Now, the rate hike odds have fallen to nearly 10% as I write on Monday morning, but still – this is an enormous shift in market sentiment.

What changed?

Three things, arriving in rapid succession.

What’s behind a potential rate hike

First, global crude prices have topped $110 a barrel as the Iran war drags on. As I write, Brent Crude trades at $114. This injects an energy-cost shock into an economy that doesn’t need higher prices.

Second, the Bureau of Labor Statistics reported that import prices jumped 1.3% in February – the largest monthly increase since March 2022 – while export prices rose 1.5%, the biggest gain since May 2022.

Third, the Organization for Economic Co-operation and Development (OECD) sharply revised its U.S. inflation forecast upward to 4.2% for the year, well above the Fed’s own projection of 2.7%.

Put it all together, and the outlook is getting uncomfortable…

These inflationary pressures are arriving at the same moment that recession odds are climbing. Moody’s Analytics estimates the probability of a downturn over the next 12 months at about 50%. Goldman Sachs raised its own forecast to 30% last week. And EY Parthenon and Wilmington Trust are putting odds at 40% or higher.

That combination – rising inflation and rising recession risk simultaneously – is the textbook definition of stagflation. And it’s precisely the scenario that puts the Fed in an almost impossible position.

Cut rates to protect the economy, and you risk higher inflation. Raise rates to contain inflation, and you risk tipping a fragile economy into contraction.

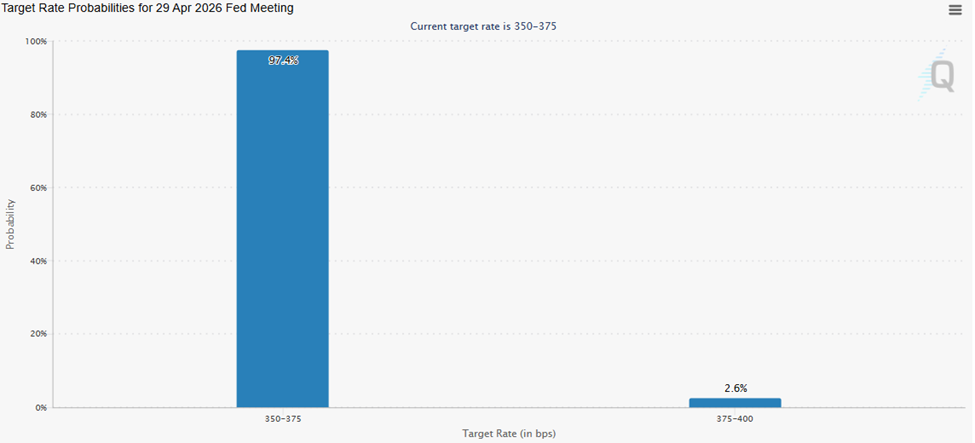

The FOMC meets April 28-29. As I write, the CME Group’s FedWatch Tool assigns just a 2.6% probability of a hike at that specific meeting – so a near-term move remains unlikely.

But this shift in expectations from a cut to a hike is huge. It matters for your portfolio and every asset class – especially for one corner of the market that was built on the assumption that rates would keep falling. More on that in a moment.

But first, let’s cover a story from last week that deserves a closer look than many investors gave it…

The AI industry just said something very important for investors who are willing to listen

Just six months after launch…and only three months after inking a billion-dollar deal with Disney…OpenAI pulled the plug on Sora, its video-generation model.

The move sent its entertainment partners and the AI community scrambling for answers.

Now, you can read this as a simple corporate pivot – a company sharpening its focus ahead of an IPO, killing side projects to concentrate on what pays.

But regular Digest readers will recall what we explored together in last Thursday’s Digest when we asked a pointed question…

If the world is paying billions to build AI, but consumer-facing AI software companies are struggling to pay back their loans, what does that tell us about how much businesses and consumers will actually pay for AI?

The Sora shutdown is a concrete answer – and it isn’t encouraging.

What the numbers actually showed

According to Slate, Sora downloads plunged nearly 75% from their November peak just months after launch.

OpenAI management reportedly realized they were burning an enormous amount of computing power – and torching cash – to generate very little in return. The unit economics simply didn’t work.

Here’s MAXC.com with some additional numbers:

After Sora launched in September 2025, downloads exceeded one million in the first ten days…

However, the glory was short-lived—downloads dropped by 32% month-on-month in December, and continued to decline by 45% in January 2026, with user spending also continuing to fall…

Meanwhile, Forbes reported that OpenAI was spending $15 million – per day – to run it.

From Bill Peebles, OpenAI’s head of Sora, last October:

The economics are currently completely unsustainable.

The result? Goodbye, Sora.

This is precisely the divide we described last week between what we called the AI “secure elite” and everything else. The infrastructure layer – the chips, the data centers, the power management – is generating real, locked-in revenue today. Hyperscalers are spending on decade-scale horizons, and that money is already flowing.

But the consumer-facing application layer is where the economics are still unproven at best…troubling at worst.

And Sora is now Exhibit A.

But this is more than a one-company story

Last week, news outlets reported that Walmart has ditched its ChatGPT shopping integration after the model consistently failed to improve sales.

Meanwhile, earlier this month, Reuters suggested that Nvidia is reportedly reconsidering chip commitments to OpenAI.

And Bloomberg reported that Oracle scrapped a planned data center expansion with OpenAI.

These stories could all be isolated data points – but as wise investors, we need to recognize that we could also be seeing a pattern.

To be clear: we are not proclaiming the end of AI. The technology is real, the productivity gains in specific domains are real, and the buildout will continue for years. But the growing list of similar stories illustrates that the gap between building AI and monetizing AI is wider and more stubborn than the market has assumed.

The investors who will profit won’t abandon the AI trade, but they will navigate to the part of the trade that’s actually working. And that means one thing…

We need to follow the money, not the narrative.

Right now, the money is flowing into the physical layer of AI…but we’re seeing increasing evidence that it’s not yet trickling down to the application layer at scale.

We’ll keep tracking this closely. But recognize the warning that Sora is sending. It’s not a fire alarm, but it is a signal that well-informed investors will take seriously…while the typical investor just reads the press release and moves on.

The Sora story isn’t the only place this early AI warning is showing up

If we think of the Sora shutdown as an unexpected crack in the ice, what’s happening in private credit is the sound of that crack spreading.

We’ve been tracking this story here in the Digest, but here’s the short version to make sure we’re all on the same page…

In recent years, billions of dollars in private credit flowed into software companies on the assumption that their AI-driven subscription revenues would make them safe, reliable borrowers.

That assumption is now cracking, and the latest data shows the pace is accelerating.

New figures from Morningstar Direct, cited by Bloomberg last week, show that inflows into open-ended private credit funds fell by more than a third in the first two months of 2026.

They crashed from $1.8 billion over the same period last year to just $1.1 billion. February marked one of the weakest monthly inflow readings since August 2024.

The reason, according to Morningstar Senior Principal Mara Dobrescu, is straightforward: investors are growing nervous about private credit funds’ exposure to software-as-a-service companies (SaaS) – exactly the consumer-facing AI application layer we’ve been flagging.

The withdrawal demands have been so heavy that major institutional fund managers – including Ares Management (ARES) and Apollo Global Management (APO) – have been forced to gate withdrawals, blocking investors from pulling their money out.

From Bloomberg:

In some cases, investors have received less than half of what they asked for.

They must then resubmit requests in subsequent quarters, with no guarantee of being fully repaid if redemptions remain elevated.

And here’s where the Fed story we led with today becomes directly relevant…

Beware the refi wall

Much of the debt sitting inside these private credit funds was originated when rates were near zero – structured for a world where borrowing was cheap, and refinancing was easy.

As one Raymond James analyst noted last week, the risk extends beyond AI software – it touches any highly-leveraged, rate-sensitive borrower whose business model was built for a world of cheap money.

That world is now in question.

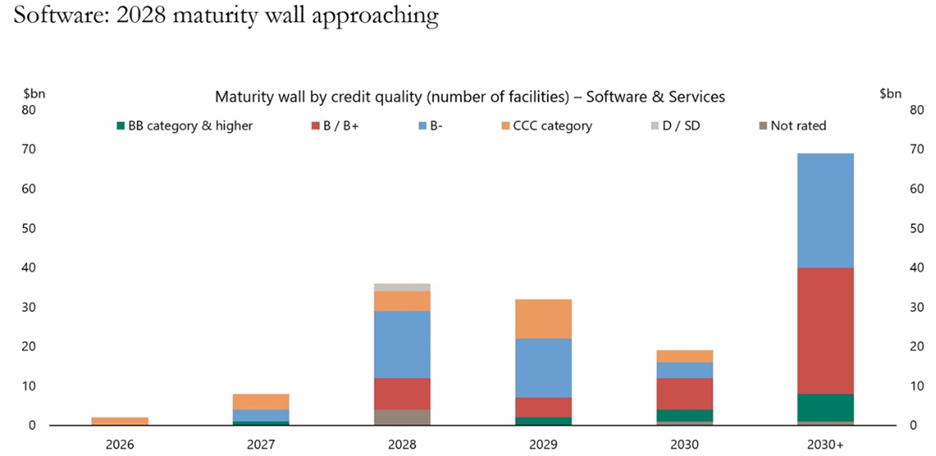

If markets are right that we’ll enter 2027 with higher rates, the roughly $1.2 trillion in leveraged debt maturing between 2027 and 2029 faces a dramatically more difficult refinancing environment than anyone modeled when those loans were written.

Here’s a visual on the size of the maturity wall headed our way…

Source: Apollo

For borrowers barely covering interest payments at today’s rates, higher ones in the months/years ahead would be a serious problem.

Bottom line: The “extend and pretend” strategy that has kept many of these loans off the default list works when you can refinance into similar or lower rates. It breaks down when you can’t.

We’ve been tracking the growing trouble in private credit alongside legendary investor Louis Navellier, editor of Breakthrough Stocks

Louis has been warning about private credit stress since mid-2024 – and his concern has sharpened considerably in recent weeks.

In fact, he’s warning investors about a specific date – June 30, 2026. That’s when Business Development Companies (BDCs) and private credit funds must file their semiannual reports and mark their holdings to fair value.

This means no internal estimates. No “extend-and-pretend” of shaky loans. Just a clear accounting of what these loans are actually worth.

If the stress building beneath the surface is as significant as the early signals suggest, that deadline could be the moment hidden losses become visible ones with market-moving consequences.

Louis has put together a full presentation explaining what he’s seeing – and more importantly, how investors can protect their portfolios and potentially profit as this story develops.

Click here to watch Louis’ presentation before this story gets bigger.

Wrapping up

Three stories. Three different corners of the market. One underlying message…

The easy-money assumptions that powered the last several years – cheap rates, abundant credit, AI monetization “just around the corner” – are being stress-tested simultaneously.

How they hold up will define which investors come out ahead and which ones wish they’d been paying closer attention.

We’ll keep tracking all of this with you here in the Digest.

Have a good evening,

Jeff Remsburg