The Fed is between a rock and a hard place … a tough place to begin hiking rates … why it’s not time to get too bearish … an important question to ask about your stocks

The Fed is in a tough position, with rampant inflation on one hand and the risk of kneecapping the economy on the other.

As to inflation, there’s no more tapdancing around it – it’s here, not going away in the immediate future, and hurting the bottom lines of everyday Americans.

Last week, we learned that inflation in November accelerated at its fastest pace since 1982. The consumer price index rose 0.8% for the month, good for a 6.8% pace on a year-over-year basis.

This morning brought news that wholesale prices rose 9.6% from last year. That topped the 9.2% estimate.

And let’s not forget how long inflation has been here. As you can see below, we’ve been dealing with it since May of 2020, more than a year and a half.

Plus, the broad inflation numbers mask how high inflation is in specific sectors and for various consumer products. Here’s CNBC with some of those details:

Energy prices have risen 33.3% since November 2020, including a 3.5% surge in November. Gasoline alone is up 58.1%.

Food prices have jumped 6.1% over the year, while used car and truck prices, a major contributor to the inflation burst, are up 31.4%, following a 2.5% increase last month…

Shelter costs, which comprise about one-third of the CPI, increased 3.8% on the year, the highest since 2007 as the housing crisis accelerated.

Now, remember, the Fed has a dual mandate – maximum employment and stable prices.

Obviously, prices are anything but stable.

***Historically, that would mean an easy call – not necessarily a call that everyone enjoys, but an easy call nonetheless

Begin hiking interest rates.

And, in fact, that’s on the agenda as the Fed holds its December policy meeting today and tomorrow.

It’s widely anticipated that the Fed will decide to speed up the end of its bond-buying program and signal that it expects to start hiking interest rates in 2022.

The question spooking Wall Street is how quickly we’ll see rates rise, and how many hikes we’ll have next year.

Too much too fast would likely roil stocks. But moving too slowly wouldn’t ease inflationary pressures, a bit like trying to extinguish a bonfire with only a glass of water.

It gets more complicated…

***We’re starting a rate-hiking cycle with the yield curve being the flattest in a generation

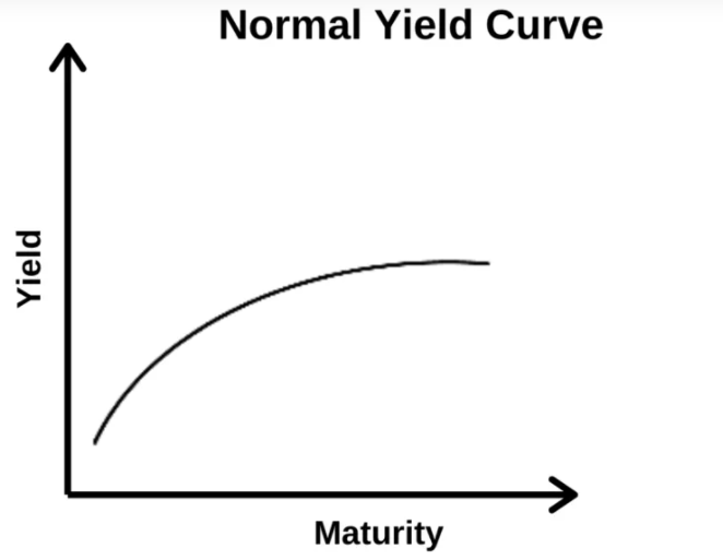

To make sure we’re all on the same page, let’s illustrate the yield curve using U.S. Treasury bonds.

A Treasury yield curve is a graphical representation of the yields of all currently available Treasuries – from short-term notes to long-term bonds.

The time until maturity is on the X-axis. The yield each Treasury generates is on the Y-axis.

In normal times, the longer you tie up your money in a bond, the higher the yield you would demand for it. After all, a two-year bond gives you far more flexibility compared to tying up your money for 10 years. So, you’d expect less yield from the two-year and more yield from the 10-year.

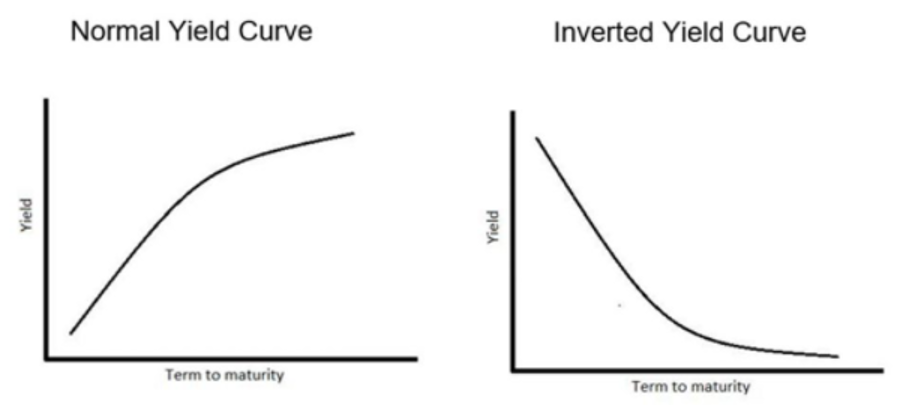

Given this, in healthy market conditions, we usually see a “lower-left” to “upper-right” yield curve. Here’s how that looks…

But when economic conditions become murky and investors aren’t sure what’s on the way, this can change.

Specifically, uncertain economic times tends to flatten the yield curve.

***The problem is that the Fed is looking to begin a new hiking cycle, yet a flat-ish yield curve constrains how much it can do

Here’s Bloomberg:

The Treasuries yield curve — or the spread between short-term and long-term interest rates — looks set to be the flattest at the beginning of a Fed tightening cycle in a generation if the central bank begins raising its benchmark overnight rate in mid-2022 as now forecast.

The two-year, 10-year spread is about 83 basis points, with futures indicating 55 basis points in June.

Both that flatness and the level of longer-term yields suggest investors see the central bank not being able to do too much before having to hit pause, or even reverse course if the economic recovery is in jeopardy.

So, why, exactly can’t Powell do too much given this flat-ish yield curve?

Well, remember, the Fed controls the Fed Funds Rate, which is the rate at which banks lend to one another. It’s a very short-term rate. The Fed doesn’t directly control rates that are further out along the yield curve.

If the Fed hikes up this short-term Fed Funds Rate in an effort squelch inflation – yet the yield curve is already flat – then we risk a yield curve inversion.

As the name implies, an inversion is when shorter-term bonds yield more than longer-dated bonds.

Now, here’s the punchline…

Historically, yield curve inversions precede recessions.

From Reuters:

Yield curve inversion is a classic signal of a looming recession.

The U.S. curve has inverted before each recession in the past 50 years. It offered a false signal just once in that time.

***But don’t get too bearish yet

For why, let’s turn to legendary investor, Louis Navellier.

Yesterday, Louis sent his Platinum Growth Club subscribers a Flash Alert podcast. Let’s jump in with Louis discussing the Fed meeting:

Obviously, a lot of people are on pins and needles about what the Fed is going to say this week.

I fully anticipate they will confirm they will be raising the Fed Funds Rate at least a quarter percent next year. And then, they will probably be reducing their (bond) tapering a bit…

The Fed is moving in baby steps. This will be all confirmed with the FOMC statement…

But inflation is good for stocks because companies make more money. Obviously, a lot of commodity-related companies can prosper from the inflation… If you have a lot of real estate or stocks, inflation is good for you.

Louis then lays out a handful of reasons why market conditions are actually bullish right now:

We’re on track for very, very strong GDP growth this quarter… the ISM (report) was record-high for services. In manufacturing, we’re seeing tremendous order backlogs… The shortages will get resolved in the new year… People were worried about Omnicon. Folks are catching it, but it’s not that bad… 10-year Treasury bond yields are plunging because of tremendous international buying pressure.

So, I feel good here, folks.

All that said, it doesn’t mean the entire stock market is a “buy.”

Louis is speaking to his Platinum Growth Club subscribers. So, they’re holding a select subset of fundamentally-strong stocks that have been identified by Louis’ rigorous stocks screening algorithms.

***As to the broad market, a healthy dose of pickiness is needed today

In other words, it’s time to get selective about the type of risk you’re willing to take.

Our macro specialist, Eric Fry, just published his latest issue of Investment Report. In it, he describes this perfectly:

To outperform the market over time, an investor must maintain the discipline of saying “no” to bad risks… and then keep on doing that until good risks come along.

It’s not easy.

It’s hard to say “no” to high-flying stocks when everyone else is saying “yes.” It’s like leaving a cocktail party while it’s still going strong.

But you must have the discipline to say “no” to bad risks and the patience to wait for better opportunities.

Bad risks are where the potential upside is much smaller than the potential downside. That’s why they’re often called “asymmetrical risks.”

Today, there are many, many bad risks in the broad market. And this suggests we need to evaluate the market through a different lens – capital preservation versus capital growth.

Back to Eric:

Disciplined investors understand the dangers of these risks. That’s why they begin their analysis by asking “What can go wrong?” rather than “What can go right?”

Disciplined investors understand that investing is optional and that they must be selective.

It’s okay to say “no” to bad risks. Unfortunately, many investors grow impatient. We justify buying richly valued stocks by comparing them to stocks that are even more richly valued. Or worse, we chase after “hot stocks” because their stories are so seductive.

But often, stocks like these offer a much larger dose of potential risk than potential reward. That’s a bad risk.

As you look at your portfolio, are you intimately aware of the risk/reward potential of your specific holdings?

Today, with the market sitting at all-time highs… on the cusp of an interest-rate-hiking cycle… with valuations at lofty levels… historic inflation… and plenty of geopolitical and/or social issues that could roil markets, you must know the potential upside of your specific stocks and compare that to the potential downside.

Given that ratio, are you taking on “good risk” if you hold that stock into 2022? Or is it bad risk?

Doing the work of answering that question now could save you a great deal of heartache later.

***Before we sign off, if you’re unsure of how to position yourself for next year, Louis, Eric, and Luke Lango sat down together last week to discuss this very issue

At their Early Warning Summit 2022, these expert analysts highlighted what’s coming in 2022 for the investment markets, and how to position your wealth accordingly.

They tackled the major issues facing investors today – inflation, Fed policy, the pandemic’s impact on growth, and far more.

Best of all, they gave away the tickers of four different stocks, poised to soar in 2022. One in particular is a stock that all three analysts believe could 2022’s top-performer.

If you missed the event, you can watch the replay by clicking here.

Hopefully, the Fed will be able to thread the needle with its policy changes. But if not, you’ll sleep better knowing your portfolio holds only “good risk” stocks.

Have a good evening,

Jeff Remsburg